|

市場調查報告書

商品編碼

2045746

工業機械市場機會、成長要素、產業趨勢分析及2026-2035年預測。Industrial Machinery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

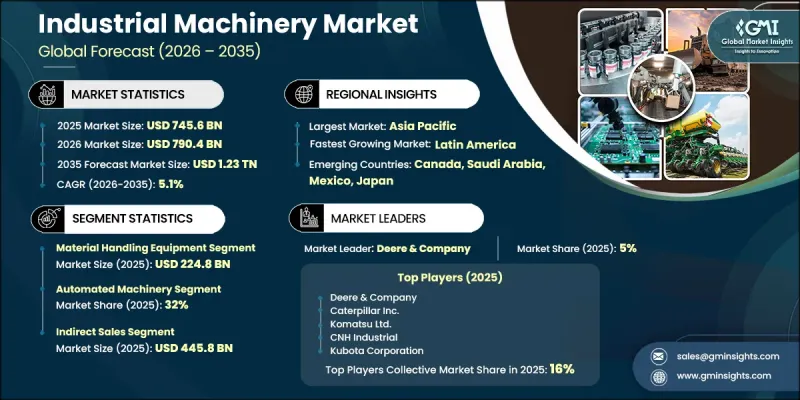

2025年全球工業機械市場價值為7,456億美元,預計2035年將以5.1%的複合年成長率成長至1.23兆美元。

市場成長的驅動力在於整個製造和生產環境加速向自動化轉型。各行業正擴大採用先進機械設備,以提高操作精度、加快生產速度並降低整體製造成本。隨著大規模生產行業的企業力求最大限度地減少對人工的依賴並降低生產錯誤,對自動化系統的需求也不斷成長。汽車、電子、製藥和食品加工等行業正擴大採用機器人、數控系統和物料輸送方案來實現生產線的現代化。人事費用的上升和技術純熟勞工的長期短缺進一步加速了終端用戶從傳統設備向高度自動化機械的轉型。工業4.0技術的應用也正在改變市場,使智慧互聯的機器能夠實現即時性能監控、預測性維護和能源最佳化。這些功能對於減少停機時間和提高成本效益的重要性日益凸顯。因此,如今的採購決策不僅受機器性能的影響,還受到數位整合、長期運作效率以及與現有工業系統的兼容性等因素的影響。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 7456億美元 |

| 預計金額 | 1.23兆美元 |

| 複合年成長率 | 5.1% |

預計2025年,物料輸送設備市場規模將達2,248億美元,佔據市場主導地位。此類別涵蓋用於生產工廠、倉庫、物流中心、建築工地及其他場所的物料運輸、儲存、保護和管理的系統。堆高機、起重機、輸送機、起吊裝置、自動化倉庫系統和工業升降機等設備在簡化工作流程、提高職場安全性和加快整體工業活動中的物料搬運速度方面發揮著至關重要的作用。

到2025年,自動化機械領域將佔據32%的市場佔有率,成為一項重要的技術類別。自動化系統旨在利用機器人、感測器和軟體控制系統等先進技術,在最大限度減少人工干預的情況下執行多項工業任務。它們能夠提高生產精度、保持穩定的產品品質並提升營運效率,從而推動了人工系統的廣泛替代,尤其是在需要高速和高精度的環境中。典型應用包括機器人組裝單元、CNC工具工具機、自動化生產線以及用於包裝、加工和物料輸送作業的智慧系統。

預計2025年,美國工業機械市場規模將達到9,19億美元,市佔率高達77.9%。這一成長主要得益於對自動化技術、節能機械和先進製造系統的大力投資,旨在提高生產效率並實現營運現代化。汽車、航太、建築、食品加工和電子產業的強勁需求持續推動著設備的普及。此外,製造業回流計畫和聯邦基礎設施發展項目也進一步提升了全美對重型機械、智慧生產系統和先進物料輸送設備的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 工業自動化和工業4.0

- 基礎設施和建築支出

- 關注能源轉型和永續性

- 產業潛在風險與挑戰

- 供應鏈中斷

- 監理和合規負擔

- 機會

- 智慧互聯機械

- 以永續發展主導的創新

- 促進因素

- 成長潛力分析

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 監理框架

- 安全標準和合規性(ISO、OSHA、CE)

- 環境法規(排放氣體、噪音)

- 進出口限制和關稅

- 《勞動與職場安全法》

- 法規的區域差異

- 未來監管變化(2026-2035 年)

- 價格分析

- 對過去價格趨勢的分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 區域價格波動

- 原物料成本對價格的影響

- 貿易數據分析(8479)

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 主要出口國

- 主要進口國

- 區域貿易平衡分析

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 預測性維護與人工智慧的融合

- 自主機器的開發

- 生產能力和生產情況

- 設備產能:按地區和主要生產商分類

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 農業機械

- 聯結機

- 收割機和聯合收割機

- 種植/播種設備

- 灌溉系統

- 其他農業機械

- 建築和土木機械

- 液壓挖土機

- 推土機

- 裝載機

- 起重機

- 自動卸貨卡車

- 平土機和刮刀

- 其他施工機械

- 物料輸送設備

- 堆高機

- 輸送帶

- 起吊裝置和吊車

- 自動化倉庫系統(AS/RS)

- 堆垛機

- 加工機械

- 食品加工設備

- 塑膠加工機械

- 金屬加工/成型機械

- 木工機械

- 化學處理設備

- 包裝器材

- 灌裝機

- 碼高機

- 貼標機

- 包裝機

- 其他包裝設備

- 工業機器人和自動化單元

- 關節機器人

- SCARA機器人

- 協作機器人(cobots)

- 直角坐標系/龍門式機器人

- 自動化製造單元

- 其他

第6章 市場估計與預測:依營運區分,2022-2035年

- 自動化機械

- 半自動機器

- 手動機械

- 機器人

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 建築和採礦

- 農業

- 食品/飲料加工

- 汽車製造

- 製藥

- 化學處理

- 包裝過程

- 半導體製造

- 金屬加工

- 其他

第8章 市場估算與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第10章:公司簡介

- 世界公司

- Caterpillar Inc.

- Deere &Company

- Komatsu Ltd.

- CNH Industrial NV

- Volvo Construction Equipment

- Liebherr Group

- Atlas Copco AB

- 當地公司

- JCB

- Hitachi Construction Machinery

- Kubota Corporation

- Sandvik AB

- Ingersoll Rand Inc

- Manitowoc Company

- Honeywell International

- 新興企業

- ASML Holding NV

- Metso

- AGCO Corporation

- Terex Corporation

- Alfa Laval AB

- GEA Group AG

- Illinois Tool Works Inc

The Global Industrial Machinery Market was valued at USD 745.6 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 1.23 trillion by 2035.

Market growth is influenced by the accelerating shift toward automation across manufacturing and production environments. Industries are increasingly deploying advanced machinery to improve operational precision, enhance production speed, and reduce overall manufacturing costs. Demand for automated systems is rising as companies aim to minimize dependence on manual labor and reduce production errors across high-volume industrial operations. Sectors such as automotive, electronics, pharmaceuticals, and food processing are increasingly integrating robotics, CNC systems, and automated material handling solutions to modernize their production lines. Rising labor costs and persistent shortages of skilled workers are further encouraging end users to transition from conventional equipment to advanced automated machinery. The adoption of Industry 4.0 technologies is also reshaping the market, enabling smart, connected machines capable of real-time performance monitoring, predictive maintenance, and energy optimization. These capabilities are increasingly viewed as essential for reducing downtime and improving cost efficiency. As a result, purchasing decisions are now driven not only by machine capacity but also by digital integration, long-term operational efficiency, and compatibility with existing industrial systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $745.6 Billion |

| Forecast Value | $1.23 Trillion |

| CAGR | 5.1% |

The material handling equipment segment generated USD 224.8 billion in 2025, securing a leading position in the market. This category includes systems designed for transporting, storing, protecting, and managing materials across production plants, warehouses, logistics centers, and construction environments. Equipment such as forklifts, cranes, conveyors, pallet jacks, hoists, automated storage and retrieval systems, and industrial lift trucks plays a critical role in improving workflow efficiency, workplace safety, and material movement speed across industrial operations.

The automated machinery segment accounted for a 32% share in 2025, making it the dominant technology category. Automated systems are designed to execute multiple industrial tasks with minimal human involvement, using advanced technologies such as robotics, sensors, and software-based control systems. Their ability to enhance production accuracy, maintain consistent output quality, and improve operational efficiency has led to widespread replacement of manual systems, particularly in high-speed and precision-driven environments. Common applications include robotic assembly units, CNC machines, automated production lines, and intelligent systems used in packaging, processing, and material handling operations.

U.S. Industrial Machinery Market accounted for a 77.9% share in 2025, reaching USD 91.9 billion. Growth in the country is driven by strong investments in automation technologies, energy-efficient machinery, and advanced manufacturing systems aimed at improving productivity and operational modernization. High demand from automotive, aerospace, construction, food processing, and electronics industries continues to support equipment adoption. Additionally, manufacturing reshoring initiatives and federal infrastructure development programs are further reinforcing demand for heavy machinery, smart production systems, and advanced material handling equipment across the country.

Key players operating in the Global Industrial Machinery Industry include Caterpillar Inc., Deere & Company, Komatsu Ltd., CNH Industrial NV, Volvo Construction Equipment, Liebherr Group, Atlas Copco AB, JCB, Hitachi Construction Machinery, Kubota Corporation, Sandvik AB, Ingersoll Rand Inc., Manitowoc Company, Honeywell International, ASML Holding NV, Metso, AGCO Corporation, Terex Corporation, Alfa Laval AB, GEA Group AG, and Illinois Tool Works Inc. Companies in the industrial machinery market are focusing on expanding automation and smart manufacturing capabilities by integrating advanced digital technologies into equipment design. They are investing heavily in research and development to improve machine efficiency, durability, and precision. Strategic partnerships with industrial end users are helping manufacturers tailor solutions to specific production requirements. Firms are also strengthening global distribution and service networks to enhance customer support and reduce downtime. A growing emphasis is placed on predictive maintenance solutions and IoT-enabled machinery to improve lifecycle performance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Operation

- 2.2.4 Application

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Industrial automation & industry 4.0

- 3.2.1.2 Infrastructure & construction spending

- 3.2.1.3 Energy transition & sustainability focus

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Supply chain disruptions

- 3.2.2.2 Regulatory & compliance burden

- 3.2.3 Opportunities

- 3.2.3.1 Smart & connected machinery

- 3.2.3.2 Sustainability-driven innovation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Regulatory framework

- 3.5.1 Safety standards & compliance (ISO, OSHA, CE)

- 3.5.2 Environmental regulations (emissions, noise)

- 3.5.3 Import/export regulations & tariffs

- 3.5.4 Labor & workplace safety laws

- 3.5.5 Regional regulatory variations

- 3.5.6 Upcoming regulatory changes (2026-2035)

- 3.6 Pricing analysis

- 3.6.1 Historical price trend analysis

- 3.6.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.6.3 Regional price variations

- 3.6.4 Impact of raw material costs on pricing

- 3.7 Trade data analysis (driven by paid data base) (8479)

- 3.7.1 Import/export volume & value trends

- 3.7.2 Key trade corridors & tariff impact

- 3.7.3 Top exporting countries

- 3.7.4 Top importing countries

- 3.7.5 Trade balance analysis by region

- 3.8 Impact of AI & generative AI on the market

- 3.8.1 AI-driven disruption of existing business models

- 3.8.2 GenAI use cases & adoption roadmap by segment

- 3.8.3 Risks, limitations & regulatory considerations

- 3.8.4 Predictive maintenance & AI integration

- 3.8.5 Autonomous machinery development

- 3.9 Capacity & production landscape (driven by primary research)

- 3.9.1 Installed capacity by region & key producer

- 3.9.2 Capacity utilization rates & expansion pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Agricultural machinery

- 5.2.1 Tractors

- 5.2.2 Harvesters & combines

- 5.2.3 Planting & seeding equipment

- 5.2.4 Irrigation systems

- 5.2.5 Other agricultural machinery

- 5.3 Construction & earth-moving equipment

- 5.3.1 Excavators

- 5.3.2 Bulldozers

- 5.3.3 Loaders

- 5.3.4 Cranes

- 5.3.5 Dump trucks

- 5.3.6 Graders & scrapers

- 5.3.7 Other construction equipment

- 5.4 Material handling equipment

- 5.4.1 Forklifts

- 5.4.2 Conveyors

- 5.4.3 Hoists & cranes

- 5.4.4 Automated storage & retrieval systems (as/rs)

- 5.4.5 Palletizers

- 5.5 Processing machinery

- 5.5.1 Food processing equipment

- 5.5.2 Plastics processing machinery

- 5.5.3 Metalworking & metal forming machines

- 5.5.4 Woodworking machinery

- 5.5.5 Chemical processing equipment

- 5.6 Packaging machinery

- 5.6.1 Filling machines

- 5.6.2 Palletizing machines

- 5.6.3 Labelling machines

- 5.6.4 Wrapping machines

- 5.6.5 Other packaging equipment

- 5.7 Industrial robots & automation cells

- 5.7.1 Articulated robots

- 5.7.2 Scara robots

- 5.7.3 Collaborative robots (cobots)

- 5.7.4 Cartesian/gantry robots

- 5.7.5 Automated manufacturing cells

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Operation, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Automated machinery

- 6.3 Semi-automated machinery

- 6.4 Manual machinery

- 6.5 Robotic machinery

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Construction & mining

- 7.3 Agriculture

- 7.4 Food & beverage processing

- 7.5 Automotive manufacturing

- 7.6 Pharmaceuticals

- 7.7 Chemical processing

- 7.8 Packaging operations

- 7.9 Semiconductor manufacturing

- 7.10 Metal fabrication

- 7.11 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Caterpillar Inc.

- 10.1.2 Deere & Company

- 10.1.3 Komatsu Ltd.

- 10.1.4 CNH Industrial NV

- 10.1.5 Volvo Construction Equipment

- 10.1.6 Liebherr Group

- 10.1.7 Atlas Copco AB

- 10.2 Regional players

- 10.2.1 JCB

- 10.2.2 Hitachi Construction Machinery

- 10.2.3 Kubota Corporation

- 10.2.4 Sandvik AB

- 10.2.5 Ingersoll Rand Inc

- 10.2.6 Manitowoc Company

- 10.2.7 Honeywell International

- 10.3 Emerging players

- 10.3.1 ASML Holding NV

- 10.3.2 Metso

- 10.3.3 AGCO Corporation

- 10.3.4 Terex Corporation

- 10.3.5 Alfa Laval AB

- 10.3.6 GEA Group AG

- 10.3.7 Illinois Tool Works Inc

工業機械人工智慧市場:按組件、應用、技術、機器類型、國家和地區分類-產業分析、市場規模、市場佔有率和預測(2026-2033 年)

工業機械人工智慧市場:按組件、應用、技術、機器類型、國家和地區分類-產業分析、市場規模、市場佔有率和預測(2026-2033 年) 工業機械接觸器市場機會、成長要素、產業趨勢分析及2026-2035年預測

工業機械接觸器市場機會、成長要素、產業趨勢分析及2026-2035年預測 工業機械市場:2026-2032年全球市場預測(依產品類型、操作方式、動力來源、控制架構、應用與銷售管道)

工業機械市場:2026-2032年全球市場預測(依產品類型、操作方式、動力來源、控制架構、應用與銷售管道) 2026年全球人工智慧(AI)預測性維護市場報告2026年工業機械人工智慧(AI)全球市場報告2026年全球商業和服務業機械市場報告2026年全球工業機械市場報告全球客製化加工服務市場(按製程類型、材料類型、生產規模和最終用途產業分類)預測(2026-2032年)客製化鑄鐵加工服務市場(按最終用戶、製程類型、產品類型、材料等級和服務模式分類),全球預測(2026-2032年)鑄鐵機械加工服務市場(按加工服務類型、最終用途行業、工具機類型和材料等級分類),全球預測,2026-2032年

2026年全球人工智慧(AI)預測性維護市場報告2026年工業機械人工智慧(AI)全球市場報告2026年全球商業和服務業機械市場報告2026年全球工業機械市場報告全球客製化加工服務市場(按製程類型、材料類型、生產規模和最終用途產業分類)預測(2026-2032年)客製化鑄鐵加工服務市場(按最終用戶、製程類型、產品類型、材料等級和服務模式分類),全球預測(2026-2032年)鑄鐵機械加工服務市場(按加工服務類型、最終用途行業、工具機類型和材料等級分類),全球預測,2026-2032年