|

市場調查報告書

商品編碼

2045730

單相可變並聯電抗器市場機會、成長要素、產業趨勢分析及2026-2035年預測。Single Phase Variable Shunt Reactor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

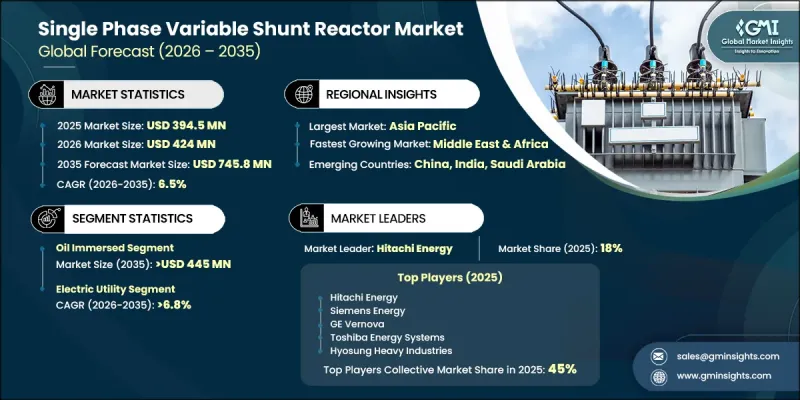

2025年全球單相可變並聯電抗器市值為3.945億美元,預計2035年將以6.5%的複合年成長率成長至7.458億美元。

市場擴張的驅動力來自輸電基礎設施的持續發展以及現代電網對精確電壓調節日益成長的需求。隨著再生能源來源網比例的不斷提高,對高效電壓調節器解決方案的需求也隨之成長,以應對發電波動。人們對提高能源效率和電能品質的日益關注也加速了先進電抗器技術的應用。此外,智慧電網系統的演進、分散式發電的擴張以及老舊輸電基礎設施的現代化改造也顯著促進了市場成長。世界各國政府都在積極投資能源基礎建設,進一步推動了先進並聯電抗器系統的應用。電力公司越來越注重符合最新法規結構和不斷發展的輸電網要求的緊湊型高性能解決方案,從而推動了全球市場的長期需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 3.945億美元 |

| 預計金額 | 7.458億美元 |

| 複合年成長率 | 6.5% |

預計2035年,油浸式電抗器市場規模將達4.45億美元。由於其卓越的熱性能、運行穩定性和可靠的電壓調節器能力,該領域呈現強勁的成長勢頭。油浸式並聯電抗器廣泛應用於高負載應用,在這些應用中,高效散熱和長運作至關重要。可再生能源併網專案和智慧電網建設投資的不斷增加,進一步推動了這些系統的部署。提高電網穩定性並最大限度減少能源損耗的能力,也持續推動其在公用事業規模應用中的廣泛應用。

預計到2025年,電力產業將佔據66.1%的市場佔有率,並在2035年之前以6.8%的複合年成長率成長。由於再生能源來源的日益併網,電力公司仍是主要的終端用戶,但這也導致電力流動出現較大波動。因此,需要先進的電壓調節系統來應對這種波動,並維持電網的穩定性和運作效率。對永續能源基礎設施投資的增加,以及政府為促進向清潔能源轉型而採取的支持措施,進一步推動了市場需求。風能和太陽能發電系統的擴展也增加了對電網內高效無功功率補償解決方案的需求。

2025年,美國單相可變並聯電抗器市場規模為4,360萬美元,預計2035年將達到7,200萬美元。推動美國市場成長的主要因素是輸電基礎設施的持續現代化改造以及對高效能電壓調節系統日益成長的需求。再生能源來源併入國家電網進一步加劇了對先進無功功率管理解決方案的需求。電網現代化和智慧電網部署方面投資的增加也促進了市場發展。美國電力公司正擴大部署先進的並聯電抗器系統,以提高電網可靠性、提升電能質量,並協助實現長期能源轉型目標。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章:行業洞察

- 工業生態系分析

- 監理情勢

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- PESTLE分析

- 分流執行器的成本結構分析

- 貿易數據分析

- 進出口額趨勢

- 主要貿易路線及關稅的影響

- 生產能力和運轉率

- 各地區的生產能力

- 運轉率和擴張計劃

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 基於細分市場的生成式人工智慧的應用案例和部署藍圖

- 預測性維護和故障檢測

- 利用數位雙胞胎進行模擬與檢測

- 風險、限制和監管考量

- 新機會和趨勢

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 競爭定位矩陣

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場規模及預測:依隔熱材料分類,2022-2035年

- 充油

- 空洞

第6章 市場規模與預測:依最終用途分類,2022-2035年

- 電力業務

- 可再生能源

第7章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第8章:公司簡介

- CG Power & Industrial Solutions

- Coil Innovation

- Fuji Electric

- GE Vernova

- GBE

- GETRA

- HICO America

- Hilkar

- Hitachi Energy

- Hyosung Heavy Industries

- Nissin Electric

- Pennsylvania Transformer

- Phoenix Electric

- Prolec Energy

- SGB SMIT

- Shrihans Electricals

- Siemens Energy

- TMC Transformers Manufacturing Company

- Toshiba Energy Systems & Solutions

- Trench Group

- WEG

The Global Single Phase Variable Shunt Reactor Market was valued at USD 394.5 million in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 745.8 million by 2035.

The market expansion is driven by continuous advancements in power transmission infrastructure and the increasing need for precise voltage regulation in modern electrical networks. The rising integration of renewable energy sources is further intensifying demand for efficient voltage control solutions to manage variability in power generation. Growing emphasis on energy efficiency and improved power quality is also accelerating the adoption of advanced reactor technologies. In addition, the evolution of smart grid systems, the expansion of distributed energy generation, and the modernization of aging grid infrastructure are significantly supporting market growth. Governments across multiple regions are actively investing in energy infrastructure development, which is further strengthening the deployment of advanced shunt reactor systems. Utilities are increasingly focusing on compact, high-performance solutions that comply with updated regulatory frameworks and evolving grid requirements, thereby boosting long-term market demand globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $394.5 Million |

| Forecast Value | $745.8 Million |

| CAGR | 6.5% |

The oil-immersed reactor segment is projected to reach USD 445 million by 2035. This segment is gaining strong traction due to its superior thermal performance, operational stability, and reliable voltage control capabilities in transmission networks. Oil-immersed shunt reactors are widely preferred in high-demand applications where efficient heat dissipation and long operational life are critical. Increasing investments in renewable integration projects and smart grid development are further strengthening the adoption of these systems. Their ability to enhance grid stability while minimizing energy losses continues to support their widespread deployment across utility-scale applications.

The electric utility sector accounted for 66.1% share in 2025 and is expected to grow at a CAGR of 6.8% through 2035. Utilities remain the primary end users due to the increasing integration of renewable energy sources that introduce higher variability in power flow. This variability requires advanced voltage regulation systems to maintain grid stability and operational efficiency. Rising investments in sustainable energy infrastructure, combined with supportive government policies promoting clean energy transition, are further driving demand. The growing deployment of wind and solar energy systems is also increasing the need for efficient reactive power compensation solutions within utility networks.

U.S. Single Phase Variable Shunt Reactor Market was valued at USD 43.6 million in 2025 and is projected to reach USD 72 million by 2035. Growth in the country is driven by the ongoing modernization of power transmission infrastructure and increasing demand for efficient voltage regulation systems. The integration of renewable energy sources into the national grid is further strengthening the need for advanced reactive power management solutions. Expanding investments in grid modernization and smart grid deployment initiatives are also contributing to market development. Utilities in the country are increasingly adopting advanced shunt reactor systems to improve grid reliability, enhance power quality, and support long-term energy transition goals.

Major companies operating in the Global Single Phase Variable Shunt Reactor Market include Siemens Energy, Hitachi Energy, GE Vernova, Fuji Electric, Toshiba Energy Systems & Solutions, Hyosung Heavy Industries, CG Power & Industrial Solutions, Nissin Electric, Trench Group, WEG, Prolec Energy, SGB SMIT, Pennsylvania Transformer, Phoenix Electric, TMC Transformers Manufacturing Company, Coil Innovation, GBE, GETRA, HICO America, Hilkar, and Shrihans Electricals. Companies operating in the single phase variable shunt reactor market are adopting multiple strategic initiatives to strengthen their market presence and improve competitiveness. Leading manufacturers are focusing on developing compact, energy-efficient, and high-performance reactor designs that align with modern grid requirements. Significant investments in research and development are being directed toward improving thermal efficiency, voltage stability, and operational reliability of shunt reactors. Companies are also expanding production capabilities and enhancing global supply chain networks to meet rising demand from utility-scale projects. Strategic collaborations with power utilities and grid operators are helping accelerate technology deployment and customization of solutions. In addition, firms are integrating digital monitoring and smart control systems into reactor designs to improve performance diagnostics and lifecycle management.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.8.3.1 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Insulation trends

- 2.4 End use trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.7 Cost structure analysis of shunt reactors

- 3.8 Trade data analysis (Driven by Primary Research)

- 3.8.1 Import/export value trends (Driven by Primary Research)

- 3.8.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.9 Production capacity & utilization (Driven by Primary Research)

- 3.9.1 Production capacity by region (Driven by Primary Research)

- 3.9.2 Utilization rates and expansion pipeline (Driven by Primary Research)

- 3.10 Impact of AI & generative AI on the market [SOLUTION CORE]

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.2.1 Predictive maintenance & fault detection

- 3.10.2.2 Digital twin simulation & testing

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Emerging opportunities & trends

- 3.12 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key Developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Insulation, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Oil immersed

- 5.3 Air core

Chapter 6 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Electric utility

- 6.3 Renewable energy

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 CG Power & Industrial Solutions

- 8.2 Coil Innovation

- 8.3 Fuji Electric

- 8.4 GE Vernova

- 8.5 GBE

- 8.6 GETRA

- 8.7 HICO America

- 8.8 Hilkar

- 8.9 Hitachi Energy

- 8.10 Hyosung Heavy Industries

- 8.11 Nissin Electric

- 8.12 Pennsylvania Transformer

- 8.13 Phoenix Electric

- 8.14 Prolec Energy

- 8.15 SGB SMIT

- 8.16 Shrihans Electricals

- 8.17 Siemens Energy

- 8.18 TMC Transformers Manufacturing Company

- 8.19 Toshiba Energy Systems & Solutions

- 8.20 Trench Group

- 8.21 WEG

電力資產管理市場:全球市場預測,2026-2032年

電力資產管理市場:全球市場預測,2026-2032年 智慧寬頻傳輸市場預測至2034年-按組件、部署模式、技術、應用、最終用戶和地區分類的全球分析

智慧寬頻傳輸市場預測至2034年-按組件、部署模式、技術、應用、最終用戶和地區分類的全球分析 固定式配電組件市場-全球產業規模、佔有率、趨勢、機會與預測:按組件類型、安裝類型、電壓、最終用戶產業、地區和競爭格局分類,2021-2031年

固定式配電組件市場-全球產業規模、佔有率、趨勢、機會與預測:按組件類型、安裝類型、電壓、最終用戶產業、地區和競爭格局分類,2021-2031年 全球配電斷路器市場規模、佔有率、趨勢和成長分析報告(2026-2034)高壓輸電設備市場:依設備類型、電壓等級、技術、安裝方式、導線類型、鐵塔類型及最終用戶分類-2026年至2032年全球預測

全球配電斷路器市場規模、佔有率、趨勢和成長分析報告(2026-2034)高壓輸電設備市場:依設備類型、電壓等級、技術、安裝方式、導線類型、鐵塔類型及最終用戶分類-2026年至2032年全球預測 2026年資料中心低壓(LV)或中壓(MV)配電全球市場報告2026-2034年全球空氣絕緣配電元件市場規模、佔有率、趨勢和成長分析報告全球資料中心高壓配電市場:預測(至 2034 年)-按組件、電壓等級、功率等級、部署方式、最終用戶和地區分類的分析2026年全球智慧配電終端市場報告低壓高速比較器市場按類型、最終用戶、供電電壓和應用分類,全球預測,2026-2032年

2026年資料中心低壓(LV)或中壓(MV)配電全球市場報告2026-2034年全球空氣絕緣配電元件市場規模、佔有率、趨勢和成長分析報告全球資料中心高壓配電市場:預測(至 2034 年)-按組件、電壓等級、功率等級、部署方式、最終用戶和地區分類的分析2026年全球智慧配電終端市場報告低壓高速比較器市場按類型、最終用戶、供電電壓和應用分類,全球預測,2026-2032年