|

市場調查報告書

商品編碼

2045709

地工止水膜市場機會、成長要素、產業趨勢分析及2026-2035年預測Geomembrane Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

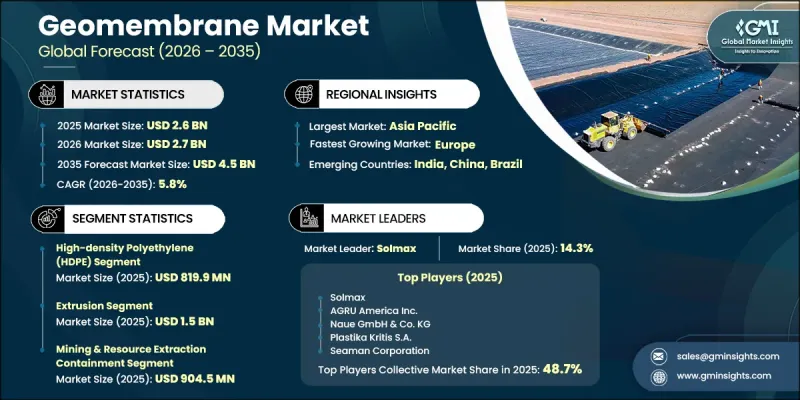

2025年全球地工止水膜市場價值為26億美元,預計2035年將以5.8%的複合年成長率成長至45億美元。

地工止水膜是一種低滲透性的合成襯墊,由多種樹脂聚合而成,並透過擠出成型或壓延加工成柔韌耐用的片材。其不透水的結構使其具有優異的密封和阻隔性能,使其成為需要嚴格環境保護和流體控制的應用中不可或缺的材料。這些材料能有效防止洩漏、滲漏和污染,廣泛應用於廢棄物管理、採礦和水利基礎設施等產業。此外,它們還具有優異的耐化學腐蝕性、抗紫外線輻射性和耐惡劣環境條件性,使其適用於地表和地下應用。對永續工程解決方案日益成長的需求進一步推動了地工膜在環保專案中的應用。聚合物化學和製造過程的持續技術進步提高了產品性能,實現了對厚度、柔軟性和機械強度的精確控制。擠出和壓延技術的進步使得生產具有更高拉伸強度、抗穿刺性和耐久性的地工止水膜成為可能,從而提升了其在礦山圍護和廢棄物管理系統等高要求應用中的性能。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 26億美元 |

| 預計金額 | 45億美元 |

| 複合年成長率 | 5.8% |

預計到2025年,高密度聚苯乙烯(HDPE)市場規模將達到8.199億美元。該市場持續成長,主要得益於其卓越的防水性能、耐化學腐蝕性能以及在掩埋和採礦作業等嚴苛環境下的適用性。 HDPE複合技術的不斷進步提升了產品的耐久性,同時,原生樹脂和再生樹脂的結合使用也有助於實現成本效益和永續性目標。這些特性進一步鞏固了HDPE作為地工止水膜市場材料類型的地位。

預計2025年,擠出成型地工膜市場規模將達15億美元。該製造程序發展勢頭強勁,因為它能夠生產厚度均勻、機械強度高且符合嚴格品質要求的地工止水膜。對包括多層共擠出技術在內的先進擠出系統的需求不斷成長,進一步提升了產品的性能。這些技術進步有助於生產適用於各種工業和環境應用的高品質地工止水膜。

預計北美地工止水膜市場規模將從2025年的7.414億美元成長到2035年的13億美元。這一區域成長的主要驅動力是廢棄物管理和採礦業對可靠圍護解決方案的需求不斷成長,以及日益嚴格的環境法規。此外,全部區域保護條例。這些因素共同推動了北美地工止水膜使用量的穩定成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 波特的分析

- PESTLE分析

- 價格趨勢

- 按地區

- 按成分

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 專利趨勢

- 貿易統計

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- LATAM

- 中東和非洲

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依原料分類,2022-2035年

- 高密度聚苯乙烯(HDPE)

- 線型低密度聚乙烯(LLDPE)

- 聚氯乙烯(PVC)

- 乙丙橡膠(EPDM)

- 其他

第6章 市場估計與預測:依技術分類,2022-2035年

- 擠壓

- 日曆

- 其他

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 廢棄物管理和掩埋圍堵系統

- 採礦和資源開採圍護

- 水利基礎設施和地方政府的應用

- 工業和化學品密封應用

- 其他

第8章 市場估算與預測:依最終用途產業分類,2022-2035年

- 環境服務及廢棄物管理業

- 採礦和自然資源產業

- 供水事業和水處理設施

- 地方政府基礎設施

- 工業製造和化學加工

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- UAE

- 其他中東和非洲國家

第10章:公司簡介

- AGRU America, Inc

- ATARFIL, SL

- Carlisle SynTec Systems

- Global Synthetics

- Istanbul Teknik

- Juta Ltd

- Naue GmbH & Co. KG

- Plastika Kritis SA

- Seaman Corporation

- Shanghai Yingfan Engineering Material Co., Ltd

- Solmax

- Sotrafa

The Global Geomembrane Market was valued at USD 2.6 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 4.5 billion by 2035.

Geomembranes are low-permeability synthetic liners produced through the polymerization of various resins into flexible, durable sheets using extrusion and calendering processes. Their impermeable structure delivers strong containment and barrier performance, making them essential for applications that require reliable environmental protection and fluid containment. These materials are widely used across industries such as waste management, mining, and water infrastructure due to their effectiveness in preventing leakage, seepage, and contamination. They also offer strong resistance to chemicals, ultraviolet exposure, and harsh environmental conditions, making them suitable for both surface and subsurface applications. Growing demand for sustainable engineering solutions has further strengthened their adoption in environmentally sensitive projects. Continuous technological improvements in polymer chemistry and manufacturing processes have enhanced product performance, allowing precise control over thickness, flexibility, and mechanical strength. Advancements in extrusion and calendering technologies have enabled the production of geomembranes with superior tensile strength, puncture resistance, and durability, improving their performance in demanding applications such as mining containment and waste management systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.6 Billion |

| Forecast Value | $4.5 Billion |

| CAGR | 5.8% |

The high-density polyethylene (HDPE) segment accounted for USD 819.9 million in 2025. This segment continues to expand due to its strong impermeability, chemical resistance, and suitability for demanding containment applications in landfills and mining operations. Ongoing advancements in HDPE formulation have improved product durability, while the use of both virgin and recycled resins is supporting cost efficiency and sustainability goals. These characteristics continue to reinforce HDPE as the most widely used material type in the geomembrane market.

The extrusion segment reached USD 1.5 billion in 2025. This manufacturing process is gaining strong traction due to its ability to produce geomembranes with uniform thickness and high mechanical strength that comply with strict quality requirements. Increasing demand for advanced extrusion systems, including multi-layer co-extrusion technologies, is further enhancing product performance characteristics. These technological advancements are supporting the production of high-quality geomembranes suitable for a wide range of industrial and environmental applications.

North America Geomembrane Market is expected to grow from USD 741.4 million in 2025 to USD 1.3 billion by 2035. Growth in the region is primarily driven by rising demand from the waste management and mining sectors for reliable containment solutions, alongside increasingly stringent environmental protection regulations. Market expansion is further supported by the adoption of advanced polymer technologies, improved installation expertise, and stronger quality assurance frameworks across the region. These factors are collectively contributing to the steady growth of geomembrane usage in North America.

Key companies operating in the Global Geomembrane Market include Solmax, AGRU America, Naue GmbH & Co. KG, Seaman Corporation, ATARFIL, S.L, Carlisle SynTec Systems, Plastika Kritis S.A., Global Synthetics, Sotrafa, Juta Ltd, Istanbul Teknik, and Shanghai Yingfan Engineering Material Co., Ltd. Companies in the geomembrane market are focusing on multiple strategic initiatives to strengthen their market position and enhance competitiveness. Leading manufacturers are investing heavily in research and development to improve polymer formulations, enhance durability, and increase resistance to environmental stress. Product innovation is centered on developing high-performance geomembranes with improved tensile strength, flexibility, and puncture resistance. Many players are also integrating recycled materials into production processes to support sustainability goals and reduce environmental impact. Expansion of manufacturing capacity and strengthening of global distribution networks are helping companies improve supply efficiency and reach emerging markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Raw Material

- 2.2.2 Technology

- 2.2.3 Application

- 2.2.4 End use industry

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By raw material

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Raw Material, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 High-Density Polyethylene (HDPE)

- 5.3 Linear Low-Density Polyethylene (LLDPE)

- 5.4 Polyvinyl Chloride (PVC)

- 5.5 Ethylene Propylene Diene Monomer (EPDM)

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Extrusion

- 6.3 Calendering

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Waste Management & Landfill Containment Systems

- 7.3 Mining & Resource Extraction Containment

- 7.4 Water Infrastructure & Municipal Applications

- 7.5 Industrial & Chemical Containment Applications

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Environmental Services & Waste Management Industry

- 8.3 Mining & Natural Resources Industry

- 8.4 Water Utilities & Treatment Facilities

- 8.5 Municipal & Government Infrastructure

- 8.6 Industrial Manufacturing & Chemical Processing

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 AGRU America, Inc

- 10.2 ATARFIL, S.L

- 10.3 Carlisle SynTec Systems

- 10.4 Global Synthetics

- 10.5 Istanbul Teknik

- 10.6 Juta Ltd

- 10.7 Naue GmbH & Co. KG

- 10.8 Plastika Kritis S.A.

- 10.9 Seaman Corporation

- 10.10 Shanghai Yingfan Engineering Material Co., Ltd

- 10.11 Solmax

- 10.12 Sotrafa

PE地工止水膜市場報告:趨勢、預測及競爭分析(至2035年)

PE地工止水膜市場報告:趨勢、預測及競爭分析(至2035年) 池塘襯墊市場-2026-2032年全球市場預測地工止水膜市場-2026-2032年全球市場預測

池塘襯墊市場-2026-2032年全球市場預測地工止水膜市場-2026-2032年全球市場預測 地工止水膜市場規模、佔有率和成長分析:按材料、應用、最終用途和地區分類-2026-2033年產業預測

地工止水膜市場規模、佔有率和成長分析:按材料、應用、最終用途和地區分類-2026-2033年產業預測 地工止水膜市場規模、佔有率和成長分析:按材料、應用、最終用途、厚度和地區分類-2026-2033年產業預測

地工止水膜市場規模、佔有率和成長分析:按材料、應用、最終用途、厚度和地區分類-2026-2033年產業預測 地工止水膜市場報告:按原料、製造流程、應用和地區分類(2026-2034 年)

地工止水膜市場報告:按原料、製造流程、應用和地區分類(2026-2034 年) 地工止水膜市場:依材料、應用、厚度和地區分類

地工止水膜市場:依材料、應用、厚度和地區分類 2026年全球池塘襯墊市場報告浮動蓋板市場:2026-2032年全球市場預測(按材料、安裝方式、厚度、應用和最終用戶分類)

2026年全球池塘襯墊市場報告浮動蓋板市場:2026-2032年全球市場預測(按材料、安裝方式、厚度、應用和最終用戶分類) 全球地工止水膜市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球地工止水膜市場規模、佔有率、趨勢和成長分析報告(2026-2034)