|

市場調查報告書

商品編碼

2045696

2026 年至 2035 年商用熱水鍋爐市場的商業機會、成長要素、產業趨勢分析與預測。Commercial Hot Water Boiler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

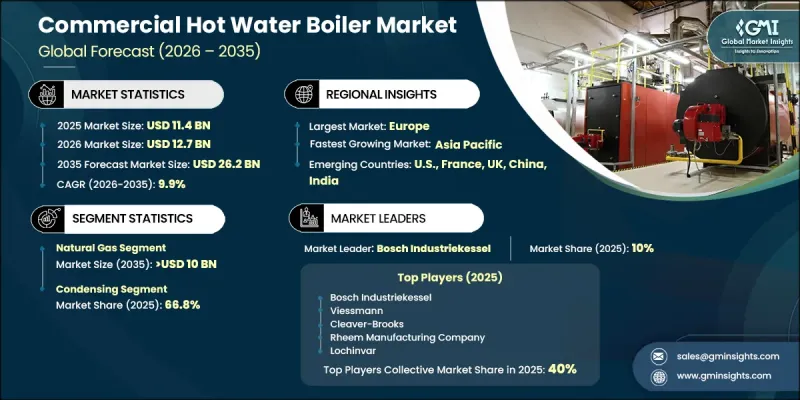

2025年全球商用熱水鍋爐市場價值為114億美元,預計到2035年將以9.9%的複合年成長率成長至262億美元。

商用熱水鍋爐產業正經歷強勁成長,這主要得益於公共和私營部門投資的增加,尤其是在醫療保健領域和大規模基礎設施建設方面。政府支出的增加在擴大商業設施暖氣系統的應用方面發揮了重要作用。同時,嚴格的排放政策正在推動更有效率、更清潔的鍋爐技術的應用。商業基礎設施對可靠暖氣解決方案的需求也促進了現有系統的更新和現代化。旅遊業的擴張和酒店基礎設施的持續發展進一步增強了市場需求。氣候變化,尤其是在寒冷地區,增加了對穩定室內暖氣解決方案的需求。此外,消費者購買力的提高和對節能建築系統的轉向也對市場滲透率產生了積極影響。鍋爐效率和燃料最佳化的技術進步進一步提升了系統性能,使現代熱水鍋爐在各種商業應用中更具吸引力。總體而言,隨著能源效率、環保法規的遵守和運作可靠性成為終端用戶的首要考慮因素,市場正在穩步發展。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 114億美元 |

| 預測金額 | 262億美元 |

| 複合年成長率 | 9.9% |

預計到2035年,天然氣驅動型鍋爐市場規模將達100億美元。該市場成長勢頭強勁,主要得益於透過提高效率和利用廢氣餘熱,可顯著降低整體燃料消耗。企業越來越重視降低生命週期成本而非初始投資,從而推動了對先進、節能型鍋爐系統的需求成長。天然氣基礎設施的完善和有利的政策環境也進一步增強了該市場的成長前景。

到2025年,冷凝式商用熱水鍋爐市佔率將達到66.8%。這項技術因其卓越的能源效率、更低的排放氣體和更低的運行成本而持續獲得市場認可。人們對永續性和碳排放目標的日益關注正在加速對冷凝式系統的需求。這些鍋爐透過回收廢氣中的熱量來提高效率,從而提高整體能源利用率,並幫助商用用戶實現長期成本節約。

預計2025年,美國商用熱水鍋爐市場規模將達15億美元。推動美國市場成長的主要因素包括嚴寒的冬季氣候、不斷成長的基礎設施投資以及商業設施對高效供暖系統日益成長的需求。現有建築的持續維修以及日益嚴格的環保法規,正在推動先進鍋爐技術的應用。此外,建設活動的增加和政府對節能系統的扶持獎勵也進一步促進了市場發展。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 原物料供應及採購分析

- 生產能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 監理情勢

- 成長潛力分析

- 波特的分析

- PESTLE分析

- 商用熱水鍋爐成本結構分析

- 新機會和趨勢

- 數位化和物聯網整合

- 投資分析及未來展望

- 價格趨勢分析

- 按地區

- 額定功率

- 貿易數據分析

- 進出口額趨勢

- 主要貿易路線及關稅的影響

- 生產能力和生產情況

- 各地區及主要生產商的產能

- 運轉率和擴張計劃

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧最佳化生產

- 預測性維護和故障檢測

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 按公司規模進行基準測試

- 排名分類標準與選擇標準

- 按銷售額、地區和創新能力分類的層級定位矩陣。

第5章 市場規模及預測:依燃料類型分類,2022-2035年

- 天然氣

- 油

- 煤炭

- 電的

- 其他

第6章 市場規模與預測:依產能分類,2022-2035年

- 0.3~2.5 MMBtu/hr

- >2.5~10 MMBtu/hr

- >10~25 MMBtu/hr

- >25~50 MMBtu/hr

- >50 MMBtu/hr

第7章 市場規模及預測:依技術分類,2022-2035年

- 簡寫型

- 非冷凝型

第8章 市場規模及預測:依應用領域分類,2022-2035年

- 辦公室

- 醫療設施

- 教育機構

- 住宿設施

- 零售店

- 其他

第9章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 法國

- 英國

- 波蘭

- 義大利

- 西班牙

- 奧地利

- 德國

- 瑞典

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 菲律賓

- 日本

- 韓國

- 澳洲

- 印尼

- 中東和非洲

- 沙烏地阿拉伯

- 伊朗

- UAE

- 奈及利亞

- 南非

- 拉丁美洲

- 阿根廷

- 智利

- 巴西

第10章:公司簡介

- Bradford White Corporation

- Bosch Industriekessel

- Cleaver-Brooks

- Energy Kinetics

- Ferroli

- Fulton

- Heatex Boilers

- Hurst Boiler &Welding

- Lennox International

- Lochinvar

- Maxima Boilers

- Mestek

- Parker Boiler

- Precision Boilers

- Remeha

- Rheem Manufacturing Company

- SAZ Boilers

- Thermal Solutions

- Viessmann

- WM Technologies

The Global Commercial Hot Water Boiler Market was valued at USD 11.4 billion in 2025 and is estimated to grow at a CAGR of 9.9% to reach USD 26.2 billion by 2035.

The commercial hot water boiler industry is witnessing strong growth supported by increasing public and private sector investments, particularly in healthcare and large-scale infrastructure development. Rising government expenditure is playing a key role in improving heating system installations across commercial facilities. At the same time, stringent emission reduction policies are encouraging the adoption of more efficient and cleaner boiler technologies. The demand for reliable heating solutions across commercial infrastructure is also driving the replacement and modernization of existing systems. Expanding tourism activity, along with continuous development in hospitality infrastructure, is further strengthening market demand. Changing climate conditions, especially in colder regions, are increasing the need for consistent indoor heating solutions. Additionally, rising consumer spending power and the shift toward energy-efficient building systems are positively influencing market adoption. Technological advancements in boiler efficiency and fuel optimization are further enhancing system performance, making modern hot water boilers more attractive across diverse commercial applications. Overall, the market is evolving steadily as energy efficiency, environmental compliance, and operational reliability become central priorities for end users.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.4 Billion |

| Forecast Value | $26.2 Billion |

| CAGR | 9.9% |

The natural gas-powered segment is expected to reach USD 10 billion by 2035. This segment is gaining traction due to its improved efficiency and ability to utilize waste heat from exhaust systems, which significantly reduces overall fuel consumption. Businesses are increasingly prioritizing lifecycle cost savings over initial investment, leading to higher demand for advanced and energy-optimized boiler systems. Expanding gas infrastructure availability and supportive policy frameworks are further strengthening growth prospects within this segment.

The condensing commercial hot water boiler segment held a 66.8% share in 2025. This technology continues to gain adoption due to its superior energy efficiency, reduced emissions, and lower operating costs. Increasing focus on sustainability and carbon reduction targets is accelerating demand for condensing systems. These boilers improve efficiency by recovering heat from flue gases, which enhances overall energy utilization and supports long-term cost savings for commercial users.

U.S. Commercial Hot Water Boiler Market was valued at USD 1.5 billion in 2025. Market growth in the country is driven by harsh winter conditions, rising infrastructure investments, and increasing demand for efficient heating systems across commercial facilities. Continuous modernization of existing buildings, combined with stricter environmental regulations, is supporting the adoption of advanced boiler technologies. Expansion of construction activity and supportive policy incentives for energy-efficient systems are further contributing to market development.

Key companies operating in the Global Commercial Hot Water Boiler Market include Viessmann, Bosch Industriekessel, Cleaver-Brooks, Lennox International, Fulton, Rheem Manufacturing Company, Lochinvar, Remeha, Parker Boiler, Thermal Solutions, Energy Kinetics, Hurst Boiler & Welding, Ferroli, Mestek, SAZ Boilers, Maxima Boilers, Precision Boilers, Heatex Boilers, WM Technologies, and Balkrishna Boilers. Companies in the Commercial Hot Water Boiler Market are adopting several strategic initiatives to strengthen their competitive position and expand market reach. Manufacturers are investing in advanced research and development to improve boiler efficiency, reduce emissions, and enhance operational performance. Product innovation is a key focus, with companies developing energy-efficient and low-emission systems aligned with environmental regulations. Strategic partnerships with construction firms, facility managers, and energy service providers are helping expand distribution networks. Firms are also focusing on digitalization and smart monitoring technologies to improve system control and predictive maintenance capabilities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Fuel trends

- 2.1.3 Capacity trends

- 2.1.4 Technology trends

- 2.1.5 Application trends

- 2.1.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of commercial hot water boilers

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization & IoT integration

- 3.10 Investment analysis & future prospects

- 3.11 Price trend analysis (USD/Unit) (Driven by Primary Research)

- 3.11.1 By region (Driven by Primary Research)

- 3.11.2 By power rating (Driven by Primary Research)

- 3.12 Trade data analysis (Driven by Primary Research)

- 3.12.1 Import/export value trends (Driven by Primary Research)

- 3.12.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Capacity by region & key producer (Driven by Primary Research)

- 3.13.2 Capacity utilization rates & expansion pipelines (Driven by Primary Research)

- 3.14 Impact of AI & Generative AI on the market (Driven by Primary Research)

- 3.14.1 AI-Driven production optimization (Driven by Primary Research)

- 3.14.2 Predictive maintenance & fault detection (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

- 4.5 Company tier benchmarking

- 4.5.1 Tier classification criteria & qualifying thresholds

- 4.5.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million, MMBTU/hr & Units)

- 5.1 Key trends

- 5.2 Natural gas

- 5.3 Oil

- 5.4 Coal

- 5.5 Electric

- 5.6 Others

Chapter 6 Market Size and Forecast, By Capacity, 2022 - 2035 (USD Million, MMBTU/hr & Units)

- 6.1 Key trends

- 6.2 ≤ 0.3 - 2.5 MMBtu/hr

- 6.3 > 2.5 - 10 MMBtu/hr

- 6.4 > 10 - 25 MMBtu/hr

- 6.5 > 25 - 50 MMBtu/hr

- 6.6 > 50 MMBtu/hr

Chapter 7 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million, MMBTU/hr & Units)

- 7.1 Key trends

- 7.2 Condensing

- 7.3 Non-condensing

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Million, MMBTU/hr & Units)

- 8.1 Key trends

- 8.2 Offices

- 8.3 Healthcare facilities

- 8.4 Educational institutions

- 8.5 Lodgings

- 8.6 Retail stores

- 8.7 Others

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million, MMBTU/hr & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 France

- 9.3.2 UK

- 9.3.3 Poland

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Austria

- 9.3.7 Germany

- 9.3.8 Sweden

- 9.3.9 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Philippines

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.4.6 Australia

- 9.4.7 Indonesia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 Iran

- 9.5.3 UAE

- 9.5.4 Nigeria

- 9.5.5 South Africa

- 9.6 Latin America

- 9.6.1 Argentina

- 9.6.2 Chile

- 9.6.3 Brazil

Chapter 10 Company Profiles

- 10.1 Bradford White Corporation

- 10.2 Bosch Industriekessel

- 10.3 Cleaver-Brooks

- 10.4 Energy Kinetics

- 10.5 Ferroli

- 10.6 Fulton

- 10.7 Heatex Boilers

- 10.8 Hurst Boiler & Welding

- 10.9 Lennox International

- 10.10 Lochinvar

- 10.11 Maxima Boilers

- 10.12 Mestek

- 10.13 Parker Boiler

- 10.14 Precision Boilers

- 10.15 Remeha

- 10.16 Rheem Manufacturing Company

- 10.17 SAZ Boilers

- 10.18 Thermal Solutions

- 10.19 Viessmann

- 10.20 WM Technologies

北美商用鍋爐和熱水器市場:2026 年

北美商用鍋爐和熱水器市場:2026 年 全球工業熱水鍋爐市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球工業熱水鍋爐市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 工業用熱水鍋爐市場機會、成長促進因素、產業趨勢分析及2026-2035年預測

工業用熱水鍋爐市場機會、成長促進因素、產業趨勢分析及2026-2035年預測 商用鍋爐市場-全球產業規模、佔有率、趨勢、機會和預測:按燃料、技術、最終用戶、地區和競爭格局分類,2021-2031年

商用鍋爐市場-全球產業規模、佔有率、趨勢、機會和預測:按燃料、技術、最終用戶、地區和競爭格局分類,2021-2031年 商用鍋爐市場:依燃料類型、技術、容量、終端用戶產業及地區分類

商用鍋爐市場:依燃料類型、技術、容量、終端用戶產業及地區分類 商用鍋爐市場規模、佔有率、趨勢和預測:按燃料類型、技術、容量、最終用戶和地區分類,2026-2034年

商用鍋爐市場規模、佔有率、趨勢和預測:按燃料類型、技術、容量、最終用戶和地區分類,2026-2034年 商用鍋爐市場:2026-2032年全球市場預測(依燃料類型、技術、壓力類型、安裝類型、應用、最終用戶和銷售管道)商用鍋爐市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的考察以及未來預測(2026-2034年)全球商用鍋爐市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

商用鍋爐市場:2026-2032年全球市場預測(依燃料類型、技術、壓力類型、安裝類型、應用、最終用戶和銷售管道)商用鍋爐市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的考察以及未來預測(2026-2034年)全球商用鍋爐市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球商用鍋爐市場報告

2026年全球商用鍋爐市場報告