|

市場調查報告書

商品編碼

2045694

顯微鏡市場商機、成長要素、產業趨勢分析及2026-2035年預測。Microscopy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

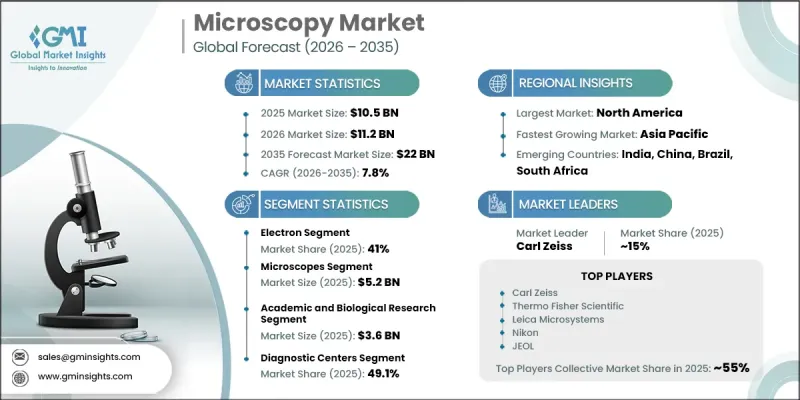

2025 年全球顯微鏡市場價值為 105 億美元,預計到 2035 年將以 7.8% 的複合年成長率成長至 220 億美元。

在技術快速發展以及奈米技術、再生醫學、生物技術和先進材料研究日益融合的推動下,這個市場持續擴張。成像系統的不斷創新拓展了顯微鏡在生命科學和工業領域的應用,鞏固了其作為關鍵分析工具的地位。對細胞結構、分子間相互作用和奈米級材料高精度可視化的需求不斷成長,進一步加速了顯微鏡的普及應用。高解析度成像技術的進步使研究人員能夠更深入地了解生物過程和材料行為,從而推動醫學和科學研究各個領域的突破性進展。隨著數位成像、自動化和人工智慧的融合,顯微鏡系統的分析精度和運作效率也不斷提高。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 105億美元 |

| 預計金額 | 220億美元 |

| 複合年成長率 | 7.8% |

顯微鏡技術是一種用於觀察和分析肉眼不可見物體的科學成像技術。它能夠對細胞、微生物、組織和奈米級結構進行精細觀察。這項技術在科學發現中發揮著至關重要的作用,並廣泛應用於生物醫學研究、工業檢測和材料科學領域。近年來,受激發射衰減顯微鏡(STED)、構造化照明顯微鏡(SIM)和單分子定位顯微鏡(SMLM)等前緣成像技術不斷出現。這些先進技術突破了傳統解析度的限制,使研究人員能夠以驚人的清晰度研究動態生物活性和分子水平結構。顯微鏡技術透過即時觀察細胞內過程和結構相互作用,持續推動藥物遞送系統、組織工程、奈米材料和生物材料等領域的創新發展。

由於電子顯微鏡能夠產生極高解析度的影像並捕捉奈米級結構細節,預計到2025年,其市佔率將達到41%。此領域廣泛應用於奈米技術研究、半導體檢測和先進材料分析。電子顯微鏡系統對於研究生物樣品和人工材料的精細結構特性至關重要,因為它們能夠實現原子級和亞奈米級的可視化。半導體製造、缺陷檢測和品質保證流程中對精密分析的需求不斷成長,持續推動電子顯微鏡的廣泛應用。先進電子裝置、奈米結構材料和微機電系統(MEMS)的快速發展進一步增強了對電子顯微鏡解決方案的需求。

預計到2025年,顯微鏡領域市場規模將達52億美元。由於顯微鏡系統是所有應用的核心硬體,因此該領域在顯微鏡市場中仍然佔據核心地位。光學設計、影像解析度、自動化和數位整合的持續改進是推動成長的主要動力。從傳統儀器轉向螢光顯微鏡、共聚焦顯微鏡顯微鏡、電子顯微鏡和光片顯微鏡等先進系統的轉變,提升了這些系統的價值,並推動了市場需求的成長。研究應用的日益複雜化以及對專業成像解決方案日益成長的需求,進一步促進了先進顯微鏡技術的應用。

截至2025年,北美在顯微鏡領域佔據最大的市場佔有率。該地區受益於許多頂尖研究型大學、政府資助實驗室和學術機構,這些機構廣泛使用先進的顯微鏡系統。這些設施支持神經科學、腫瘤學、遺傳學、細胞生物學、奈米技術和材料科學等廣泛的研究活動。這些機構內共用顯微鏡中心的普遍建立,擴大了超高解析度、共聚焦和光片等先進成像平台的使用範圍。這些共用設施的高利用率持續推動儀器升級和對下一代成像技術的持續投資。

目錄

第1章:調查方法

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響產業的因素

- 促進因素

- 顯微鏡技術的應用領域不斷拓展

- 顯微鏡技術的進步

- 人們對奈米技術和再生醫學的興趣日益濃厚。

- 有利於顯微鏡技術研究開發的資金籌措環境

- 產業潛在風險與挑戰

- 熟練專業人員短缺

- 開放原始碼顯微鏡軟體的可用性

- 市場機遇

- 整合基於雲端的資料管理解決方案

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 科技趨勢

- 最新技術

- 全像顯微鏡技術的進步

- 量子顯微鏡和下一代成像技術

- 新興技術

- 微型高解析度顯微鏡

- 影像分析的SaaS(軟體即服務)模式

- 最新技術

- 未來市場趨勢

- 2025年價格分析

- 專利分析

- 人工智慧和生成式人工智慧對市場的影響

- 波特的分析

- PESTLE分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 光

- 直立

- 倒置

- 立體顯微鏡

- 相位差

- 螢光

- 共聚焦掃描

- 近距離掃描

- 其他光學顯微鏡技術

- 電子的

- 掃描式電子顯微鏡

- 穿透式電子顯微鏡

- 掃描探針

第6章 市場估計與預測:依組件分類,2022-2035年

- 顯微鏡

- 配件

- 軟體

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 藥物發現和藥物開發

- 臨床診斷

- 藥品和生物製藥的生產

- 學術和生物學調查

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 診斷中心

- 學術研究機構

- 其他最終用戶

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第10章:公司簡介

- Bruker Corporation

- Carl Zeiss AG

- Leica Microsystems

- Nikon Corporation

- Thermo Fisher Scientific Inc.

- JEOL Ltd.

- Hitachi High-Tech Corporation

- Evident Corporation(Olympus)

- Keyence Corporation

- Oxford Instruments

- Horiba Ltd.

- Lasertec Corporation

- Motic

- Meiji Techno

- Vision Engineering Ltd.

The Global Microscopy Market was valued at USD 10.5 billion in 2025 and is estimated to grow at a CAGR of 7.8% to reach USD 22 billion by 2035.

The market is experiencing expansion driven by rapid technological advancements and increasing integration across nanotechnology, regenerative medicine, biotechnology, and advanced materials research. Continuous innovation in imaging systems is broadening the use of microscopy in both life sciences and industrial applications, strengthening its position as a critical analytical tool. The growing demand for highly precise visualization of cellular structures, molecular interactions, and nanoscale materials is further accelerating adoption. Advancements in high-resolution imaging technologies are enabling researchers to achieve deeper insights into biological processes and material behaviors, which is supporting breakthroughs across healthcare and scientific research domains. The increasing convergence of digital imaging, automation, and artificial intelligence is further enhancing analytical accuracy and operational efficiency in microscopy systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.5 Billion |

| Forecast Value | $22 Billion |

| CAGR | 7.8% |

Microscopy is defined as a scientific imaging technique used to observe and analyze objects that are not visible to the naked eye. It allows detailed examination of cells, microorganisms, tissues, and nanoscale structures. The technology plays a vital role in scientific discovery and is widely used across biomedical research, industrial inspection, and materials science applications. Recent advancements have introduced cutting-edge imaging modalities such as stimulated emission depletion microscopy (STED), structured illumination microscopy (SIM), and single-molecule localization microscopy (SMLM). These advanced techniques enable visualization beyond traditional resolution limits, allowing researchers to study dynamic biological activities and molecular-level structures with exceptional clarity. Microscopy continues to support innovation in drug delivery systems, tissue engineering, nanomaterials, and biomaterials development by enabling real-time observation of sub-cellular processes and structural interactions.

The electron segment held a 41% share in 2025, driven by its ability to deliver extremely high-resolution imaging and capture nanoscale structural details. This segment is widely used in nanotechnology research, semiconductor inspection, and advanced materials analysis. Electron-based imaging systems allow visualization at atomic and sub-nanometer scales, making them essential for studying fine structural characteristics in biological samples and engineered materials. The increasing demand for precise analysis in semiconductor fabrication, defect detection, and quality assurance processes continues to support strong adoption. The growth of advanced electronic devices, nanostructured materials, and microelectromechanical systems is further reinforcing demand for electron microscopy solutions.

The microscopes segment accounted for USD 5.2 billion in 2025. This segment remains central to the microscopy market as microscope systems form the core hardware across all applications. Growth is supported by continuous improvements in optical design, imaging resolution, automation, and digital integration. The transition from conventional instruments to advanced systems such as fluorescence, confocal, electron, and light-sheet microscopes is increasing system value and driving higher demand. The expanding complexity of research applications and the need for specialized imaging solutions are further strengthening the adoption of advanced microscope technologies.

North America Microscopy Market held the largest share in 2025. The region benefits from a strong presence of leading research universities, government-funded laboratories, and academic medical institutions that extensively use advanced microscopy systems. These facilities support a wide range of research activities across neuroscience, oncology, genetics, cell biology, nanotechnology, and materials science. The widespread establishment of shared microscopy centers within academic institutions has increased access to advanced imaging platforms such as super-resolution, confocal, and light-sheet systems. High utilization rates of these shared facilities continue to drive recurring investments in equipment upgrades and next-generation imaging technologies.

Key companies operating in the Global Microscopy Industry include Nikon, Carl Zeiss, Leica Microsystems, Thermo Fisher Scientific, JEOL, Hitachi High-Tech, Oxford Instruments, Bruker, Keyence, Evident, Horiba, Lasertec, Meiji Techno, Motic, and Vision Engineering. Companies in the microscopy market are focusing on advancing imaging performance by developing next-generation high-resolution and multi-modal systems that enhance research accuracy and application scope. They are investing heavily in research and development to improve automation, digital imaging, and AI-enabled analysis capabilities. Strategic collaborations with universities, research institutes, and healthcare organizations are strengthening product adoption and expanding application reach. Manufacturers are also emphasizing software integration and cloud-based data management to improve workflow efficiency and data accessibility. Expansion into emerging research markets and customization of microscopy solutions for specific scientific applications are helping companies strengthen their global footprint.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.1.1 Key market trends

- 2.1.2 Product trends

- 2.1.3 Component trends

- 2.1.4 Application trends

- 2.1.5 End use trends

- 2.1.6 Regional trends

- 2.2 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing application areas of microscopy

- 3.2.1.2 Technological advancement in microscopes

- 3.2.1.3 Rising focus on nanotechnology and regenerative medicine

- 3.2.1.4 Favourable funding scenario for R&D in microscopy

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Dearth of skilled professionals

- 3.2.2.2 Availability of open-source microscopy software

- 3.2.3 Market opportunity

- 3.2.3.1 Integration of cloud-based data management solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological landscape (Driven by Primary Research)

- 3.5.1 Current technologies

- 3.5.1.1 Holographic microscopy advances

- 3.5.1.2 Quantum microscopy and next-generation imaging

- 3.5.2 Emerging technologies

- 3.5.2.1 Miniaturized high-resolution microscopy

- 3.5.2.2 Software-as-a-service (SaaS) models for imaging analysis

- 3.5.1 Current technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Pricing analysis, 2025 (Driven by Primary Research)

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Impact of AI and Generative AI on the market (Driven by Primary Research)

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Optical

- 5.2.1 Upright

- 5.2.2 Inverted

- 5.2.3 Stereomicroscopes

- 5.2.4 Phase contrast

- 5.2.5 Fluorescence

- 5.2.6 Confocal scanning

- 5.2.7 Near field scanning

- 5.2.8 Other optical microscopes

- 5.3 Electron

- 5.3.1 Scanning electron

- 5.3.2 Transmission

- 5.4 Scanning probe

Chapter 6 Market Estimates and Forecast, By Component, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Microscopes

- 6.3 Accessories

- 6.4 Software

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Drug discovery and development

- 7.3 Clinical diagnostics

- 7.4 Pharmaceutical and biopharmaceutical manufacturing

- 7.5 Academic and biological research

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Diagnostic centers

- 8.3 Academic and research institutes

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bruker Corporation

- 10.2 Carl Zeiss AG

- 10.3 Leica Microsystems

- 10.4 Nikon Corporation

- 10.5 Thermo Fisher Scientific Inc.

- 10.6 JEOL Ltd.

- 10.7 Hitachi High-Tech Corporation

- 10.8 Evident Corporation (Olympus)

- 10.9 Keyence Corporation

- 10.10 Oxford Instruments

- 10.11 Horiba Ltd.

- 10.12 Lasertec Corporation

- 10.13 Motic

- 10.14 Meiji Techno

- 10.15 Vision Engineering Ltd.

神經顯微鏡設備市場:全球市場預測,2026-2032年顯微鏡市場-2026-2032年全球市場預測顯微鏡技術市場-2026-2032年全球市場預測

神經顯微鏡設備市場:全球市場預測,2026-2032年顯微鏡市場-2026-2032年全球市場預測顯微鏡技術市場-2026-2032年全球市場預測 全球先進顯微鏡市場(2026-2037 年)

全球先進顯微鏡市場(2026-2037 年) 表面科學市場(2025-2030 年):市場概覽

表面科學市場(2025-2030 年):市場概覽 共聚焦掃描顯微鏡市場規模、佔有率和趨勢分析報告:按產品類型、應用、地區和細分市場預測(2026-2033 年)

共聚焦掃描顯微鏡市場規模、佔有率和趨勢分析報告:按產品類型、應用、地區和細分市場預測(2026-2033 年) 生命科學顯微鏡市場:按產品類型、最終用戶和地區分類

生命科學顯微鏡市場:按產品類型、最終用戶和地區分類 立體變焦顯微鏡市場預測—按類型、應用和地區分類的全球分析—2034年視覺檢測顯微鏡市場預測至2034年—按類型、放大倍率、照明光源、應用、最終用戶和地區分類的全球分析螢光顯微鏡市場規模、佔有率和趨勢分析報告:按類型、應用、地區和細分市場預測(2026-2033 年)

立體變焦顯微鏡市場預測—按類型、應用和地區分類的全球分析—2034年視覺檢測顯微鏡市場預測至2034年—按類型、放大倍率、照明光源、應用、最終用戶和地區分類的全球分析螢光顯微鏡市場規模、佔有率和趨勢分析報告:按類型、應用、地區和細分市場預測(2026-2033 年)