|

市場調查報告書

商品編碼

2045693

機器人空氣清淨機市場機會、成長要素、產業趨勢分析及2026-2035年預測Robotic Air Purifier Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

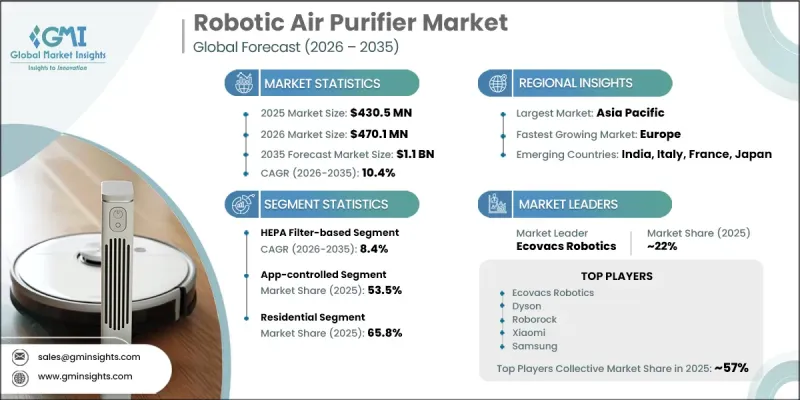

預計到 2025 年,全球機器人空氣清淨機市場價值將達到 4.305 億美元,年複合成長率為 10.4%,到 2035 年將達到 11 億美元。

在商業環境中,人們對空氣品質的關注度日益提高。家庭、辦公室、醫療機構和公共場所等場所對保持室內空氣清潔的需求不斷成長,這些場所都將室內空氣清潔視為首要任務。人們對呼吸系統健康以及室內污染危害的認知不斷提高,進一步推動了市場擴張。此外,連網家庭技術和智慧自動化系統的快速普及,加速了機器人空氣清淨機融入更廣泛的智慧家庭生態系統。消費者越來越傾向於選擇具備遠端監控、自動化功能以及與數位平台無縫連接的智慧空氣清淨器,這支撐了機器人空氣清淨機市場的整體持續成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 4.305億美元 |

| 預測市場規模 | 11億美元 |

| 複合年成長率 | 10.4% |

採用高效能空氣微粒過濾器(HEPA過濾器)的空氣淨化機器人市場預計在2025年達到1.719億美元,並在2026年至2035年間以8.4%的複合年成長率成長。由於其高效的過濾性能和對影響室內空氣品質的細顆粒污染物的捕捉能力,該細分市場在空氣淨化機器人市場中持續佔據主導地位。 HEPA過濾技術因其可靠的淨化性能,在空氣品質和呼吸健康備受關注的環境中被廣泛採用。消費者對更健康室內空間的日益關注以及對空氣污染物的日益重視,正在推動配備HEPA過濾器的空氣淨化機器人在住宅和商用中的持續成長。

預計到2025年,App控制型空氣清淨機市佔率將達到53.5%,並在2035年之前維持6.5%的複合年成長率。消費者越來越青睞可透過應用程式遠端控制和監控的智慧家庭設備。 App控制型機器人空氣清淨機使用戶能夠直接追蹤空氣品質狀況、自訂淨化設定、設定運作時間表,並透過連接的行動裝置接收即時通知。隨著物聯網生態系統的擴展和智慧家庭技術的普及,對自動化空氣淨化解決方案的需求持續成長,鞏固了App控制系統在市場上的主導地位。

預計到2025年,中國機器人空氣清淨機市場規模將達到5,980萬美元,並在2026年至2035年間以10.7%的複合年成長率成長。全部區域的市場成長主要受都市化加快、污染加劇以及消費者對智慧家庭技術日益成長的需求所驅動。中國市場持續引領區域需求,機器人空氣清淨系統已廣泛應用於住宅、教育機構和商業建築。該地區的消費者越來越傾向於選擇具備先進自動化功能、智慧監控系統和行動連線連線功能的產品。亞太地區的製造商正致力於提供技術先進、體積小巧且經濟實惠的產品,以滿足消費者對便利性、自動化和室內空氣品質控制等方面的不斷變化的偏好。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 人們越來越關注室內空氣污染及其對健康的影響

- 智慧家庭和連網型設備的廣泛應用

- 感測器、導航和過濾系統方面的技術進步

- 潛在風險和挑戰

- 與傳統空氣清淨機相比,它的成本更高。

- 市場認知度低,市場滲透尚處於初期階段。

- 機會

- 人工智慧與先進空氣品質監測系統的整合

- 在污染程度不斷上升的新興市場拓展業務。

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 監理情勢

- 標準和合規要求

- 區域監理框架

- 認證標準

- 波特的分析

- PESTLE分析

- 價格分析

- 2021-2024年歷史價格趨勢分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 按產品類型和功能進行價格細分

- 區域價格波動與價格平價分析

- 原物料成本對價格的影響

- 促銷策略和季節性折扣模式

- 貿易數據分析

- 2021-2024年進出口數量及價值趨勢

- 主要貿易路線及關稅的影響

- 區域貿易平衡

- HS編碼分類與關稅結構

- 貿易協定和製裁的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 預測性空氣品質管理

- 自動駕駛和車內地圖的最佳化

- 個人化空氣淨化方案

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 人工智慧語音助理和自然語言控制

- 濾波器最佳化的衍生設計

- 人工智慧驅動的客戶支援和故障排除

- 風險、限制和監管考量

- 資料隱私問題與網路安全威脅

- 演算法偏差和效能可靠性

- 監管合規(人工智慧法律、消費者安全)

- 利用人工智慧改造現有經營模式

- 目前分銷基礎設施和通路滲透情況

- 按地區和格式分類的頻道覆蓋率(線上與線下滲透率)

- 缺乏最後一公里基礎設施和不斷變化的管道

- 電子商務成熟度與D2C模式

- 專業零售與大眾市場通路的發展趨勢

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- HEPA濾網底座

- 活性碳

- 基於UV-C光

- 離子發生器類型

- 其他

第6章 市場估計與預測:依技術分類,2022-2035年

- 應用程式 Z 類型

- 語音控制

- 智慧整合

第7章 市場規模估算與預測(2022-2035年)

- 袖珍的

- 中等的

- 大的

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 住宅

- 商業的

第9章 市場估價與預測:依通路分類,2022-2035年

- 離線

- 線上

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- UAE

- 南非

第11章:公司簡介

- 360(Qihoo 360)

- Dreame Technology

- Dyson

- Ecovacs Robotics

- Eufy

- iLife

- LG

- Narwal

- Philips

- Roborock

- Samsung

- Sharp

- TCL

- Wyze

- Xiaomi

The Global Robotic Air Purifier Market was valued at USD 430.5 million in 2025 and is estimated to grow at a CAGR of 10.4% to reach USD 1.1 billion by 2035.

Increasing awareness regarding indoor air quality and its impact on human health continues to drive strong demand for robotic air purifiers worldwide. Rising levels of indoor pollutants, including airborne particles, allergens, smoke residue, and volatile compounds, are creating growing concerns across residential and commercial environments. As consumers place greater emphasis on healthier indoor living conditions, robotic air purifiers are gaining popularity for their ability to automatically monitor and purify indoor air while improving convenience and operational efficiency. Demand is increasing across homes, commercial offices, healthcare environments, and institutional facilities where maintaining clean indoor air has become a priority. Growing awareness regarding respiratory health and the harmful effect of indoor pollution is further supporting market expansion. In addition, rapid adoption of connected home technologies and smart automation systems is accelerating the integration of robotic air purifiers into broader smart home ecosystems. Consumers increasingly prefer intelligent air purification devices that offer remote monitoring, automated functionality, and seamless connectivity with digital platforms, supporting continued growth across the robotic air purifier market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $430.5 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 10.4% |

The HEPA filter-based segment generated USD 171.9 million in 2025 and is anticipated to grow at a CAGR of 8.4% from 2026 to 2035. This segment continues to dominate the robotic air purifier market because of its strong filtration efficiency and ability to capture fine airborne contaminants that affect indoor air quality. HEPA filtration technology is widely preferred for environments where air cleanliness and respiratory health are major concerns due to its reliable purification performance. Growing consumer focus on healthier indoor spaces and rising concerns related to airborne pollutants continue to strengthen adoption of HEPA filter-based robotic air purifiers across both residential and commercial applications.

The app-controlled segment accounted for a 53.5% share in 2025 and is expected to register a CAGR of 6.5% through 2035. Consumers are increasingly favoring smart connected appliances that can be remotely operated and monitored through digital applications. App-controlled robotic air purifiers enable users to track air quality conditions, customize purification settings, schedule operations, and receive real-time notifications directly through connected mobile devices. The growing expansion of IoT-enabled ecosystems and increasing adoption of smart home technologies continue to strengthen demand for automation-driven air purification solutions, reinforcing the leading position of app-controlled systems within the market.

China Robotic Air Purifier Market reached USD 59.8 million in 2025 and is projected to grow at a CAGR of 10.7% between 2026 and 2035. Market growth across the Asia Pacific region is being supported by increasing urbanization, rising pollution levels, and growing consumer interest in smart home technologies. China continues to lead regional demand due to widespread adoption of robotic air purification systems across residential properties, educational facilities, and commercial buildings. Consumers throughout the region increasingly prefer products equipped with advanced automation capabilities, intelligent monitoring systems, and mobile connectivity features. Manufacturers across Asia Pacific are focusing on delivering technologically advanced, compact, and cost-efficient products that align with evolving consumer preferences for convenience, automation, and enhanced indoor air quality management.

Major companies operating in the Global Robotic Air Purifier Market include 360 (Qihoo 360), Dreame Technology, Dyson, Ecovacs Robotics, Eufy, iLife, LG, Narwal, Philips, Roborock, Samsung, Sharp, TCL, Wyze, and Xiaomi. Companies operating in the robotic air purifier market are implementing various strategic initiatives to strengthen market share and improve competitive positioning. Leading manufacturers are heavily investing in research and development to introduce advanced filtration technologies, AI-powered automation, and intelligent air quality monitoring systems. Product innovation focused on app connectivity, voice-control compatibility, and seamless smart home integration is helping companies enhance user experience and attract technology-focused consumers. Businesses are also expanding product portfolios with compact, energy-efficient, and multifunctional devices tailored for residential and commercial applications. Strategic partnerships with smart home platform providers and expansion through online retail channels are further supporting global market penetration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Technology

- 2.2.4 Size

- 2.2.5 End Use

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising concerns over indoor air pollution and health impacts

- 3.2.1.2 Growing adoption of smart home and connected devices

- 3.2.1.3 Technological advancements in sensors, navigation, and filtration systems

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High cost compared to conventional air purifiers

- 3.2.2.2 Limited awareness and early-stage market penetration

- 3.2.3 Opportunities

- 3.2.3.1 Integration of AI and advanced air quality monitoring systems

- 3.2.3.2 Expansion in emerging markets with rising pollution levels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (2021-2024) (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.9.3 Price segmentation by product type & features

- 3.9.4 Regional price variations & parity analysis

- 3.9.5 Impact of raw material costs on pricing

- 3.9.6 Promotional strategies & seasonal discounting patterns

- 3.10 Trade data analysis (driven by paid database)

- 3.10.1 Import/export volume & value trends (2021-2024) (driven by paid database)

- 3.10.2 Key trade corridors & tariff impact (driven by paid database)

- 3.10.3 Trade balance by region

- 3.10.4 HS code classification & customs duty structure

- 3.10.5 Impact of trade agreements & sanctions

- 3.11 Impact of AI and generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.1.1 Predictive air quality management

- 3.11.1.2 Autonomous navigation & room mapping optimization

- 3.11.1.3 Personalized air purification routines

- 3.11.2 GenAI use cases and adoption roadmap by segment

- 3.11.2.1 AI-powered voice assistants & natural language control

- 3.11.2.2 Generative design for filter optimization

- 3.11.2.3 AI-enhanced customer support & troubleshooting

- 3.11.3 Risks, limitations & regulatory considerations

- 3.11.3.1 Data privacy concerns & cybersecurity threats

- 3.11.3.2 Algorithm bias & performance reliability

- 3.11.3.3 Regulatory compliance (AI Act, consumer safety)

- 3.11.1 AI-driven disruption of existing business models

- 3.12 Distribution infrastructure and channel penetration landscape (driven by primary research)

- 3.12.1 Channel coverage by region & format (online vs. offline penetration) (driven by primary research)

- 3.12.2 Last-mile infrastructure gaps & emerging channel shifts (driven by primary research)

- 3.12.3 E-commerce maturity & direct-to-consumer models

- 3.12.4 Specialty retail vs. mass market channel dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 HEPA Filter-Based

- 5.3 Activated Carbon

- 5.4 UV-C Light-Based

- 5.5 Ionizer-Based

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 App-Controlled

- 6.3 Voice-Controlled

- 6.4 Smart Integration

Chapter 7 Market Estimates & Forecast, By Size, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Compact

- 7.3 Medium

- 7.4 Large

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Offline

- 9.3 Online

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 360 (Qihoo 360)

- 11.2 Dreame Technology

- 11.3 Dyson

- 11.4 Ecovacs Robotics

- 11.5 Eufy

- 11.6 iLife

- 11.7 LG

- 11.8 Narwal

- 11.9 Philips

- 11.10 Roborock

- 11.11 Samsung

- 11.12 Sharp

- 11.13 TCL

- 11.14 Wyze

- 11.15 Xiaomi