|

市場調查報告書

商品編碼

2045664

菸草過濾嘴市場機會、成長要素、產業趨勢分析及2026-2035年預測。Cigarette Filter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

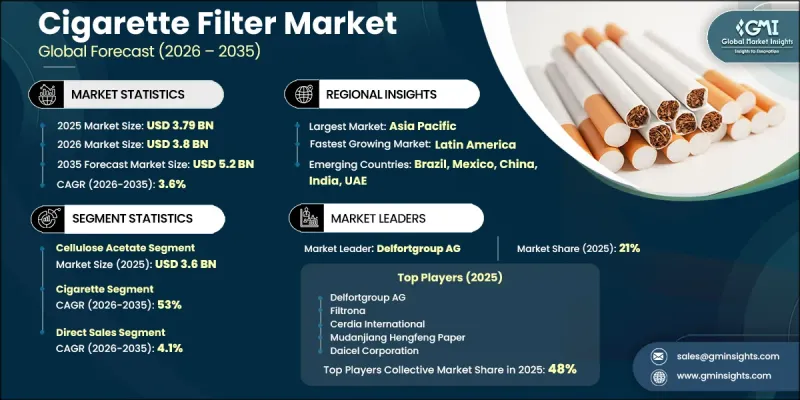

2025年全球菸草過濾嘴市場價值為37.9億美元,預計到2035年將以3.6%的複合年成長率成長至52億美元。

隨著消費者對吸菸相關健康風險的認知不斷提高,以及對旨在減少有害物質接觸的產品的需求日益成長,全球菸草過濾嘴產業持續加速發展。過濾嘴廣泛用於捲菸中,以減少焦油、尼古丁和其他有毒化合物的攝入,是整個菸草行業的重要組成部分。一些新興國家吸煙率的上升,以及過濾材料和製造技術的不斷進步,都推動了該行業的擴張。世界各國政府實施的監管政策也影響市場發展,要求製造商遵守旨在降低吸菸相關健康風險的更嚴格標準。這種監管壓力促使企業投資先進的過濾解決方案和新一代材料。永續發展趨勢也正在改變菸草過濾嘴產業,對環保替代品的需求不斷成長,推動了可生物分解和環保過濾嘴產品的開發。製造商越來越注重永續創新,以滿足不斷變化的消費者偏好和環保期望。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 37.9億美元 |

| 預測市場規模 | 52億美元 |

| 複合年成長率 | 3.6% |

預計到2025年,醋酸纖維素市場規模將達到36億美元,並在2035年之前以3.7%的複合年成長率成長。由於其卓越的過濾性能、價格優勢以及在菸草製造領域的廣泛應用,市場對醋酸纖維素濾嘴的需求持續成長。大眾對吸菸危害的認知不斷提高,也推動了濾嘴技術的進步,為醋酸纖維素基產品創造了有利的成長機會。此外,人們對比傳統塑膠菸草濾嘴更環保的材料的興趣日益濃厚,也促進了該細分市場的發展。隨著產品不斷創新和可生物分解濾嘴解決方案的改進,預計未來幾年醋酸纖維素濾嘴的市場前景將進一步增強。

預計到2025年,菸草市場佔有率將達到61%,並在2026年至2035年間以53%的複合年成長率成長。菸草過濾嘴產業的擴張主要受消費者日益關注減少接觸有害吸菸物質的驅動。隨著製造商致力於降低菸草產品中的焦油和尼古丁含量,過濾嘴的使用也變得越來越普遍。先進過濾材料(包括活性碳和永續替代材料)的技術進步不斷為整個行業創造新的成長機會。此外,旨在減輕吸菸對健康影響的政府法規也在促進創新菸草過濾嘴技術的應用,並支持市場的長期發展。

預計到2025年,美國菸草過濾嘴市佔率將達到77%,市場規模將達3.154億美元。美國市場趨勢受消費者偏好變化、區域吸煙趨勢和不斷完善的法律規範的影響。雖然吸菸人口相對較高的地區持續支撐著產業需求,但由於其他地區更嚴格的禁煙令以及公眾對吸菸相關健康風險的認知不斷提高,市場成長正在放緩。消費者對可生物分解菸草過濾嘴的偏好日益成長,也影響美國多個地區的購買行為,促使製造商拓展產品線,推出環保型過濾嘴產品。預計產品創新和對永續材料的投資將繼續成為推動美國菸草過濾嘴產業成長的關鍵因素。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 未來市場趨勢

- 供應鏈分析

- 原物料採購狀況

- 製造流程

- 配電網結構

- 供應鏈脆弱性與風險緩解

- 技術與創新展望

- 生物分解過濾材料技術

- 微穿孔和通風技術

- 多層濾波器設計創新

- 奈米纖維膜的整合

- 風味膠囊技術

- 價格分析

- 對過去價格趨勢的分析

- 定價策略:按業務類型分類

- 監理框架

- 歐盟一次性塑膠指令(SUPD)的影響

- 菸草製品指令(2014/40/EU)

- 區域過濾材料法規

- 生產者延伸責任制(EPR)

- 管理過濾廢棄物的義務

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧正在改變傳統的經營模式。

- 按客戶群分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 人工智慧驅動的智慧家庭生態系統的整合

- 波特五力分析

- PESTLE分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依過濾資料分類,2022-2035年

- 醋酸纖維素

- 紙

- PLA

- 其他

第6章 市場估計與預測:依菸草類型分類,2022-2035年

- 菸草

- 普通/特大號

- 超薄

- 標準/常規

- 短/迷你

- 加熱菸草製品(HNB煙棒)

第7章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第9章:公司簡介

- 全球主要公司

- Cerdia International

- Daicel Corporation

- Delfortgroup AG

- Filtrona

- Julius Glatz

- Mativ Holdings

- Miquel y Costas & Miquel

- 當地公司

- Anji Hengda Paper

- Bright Eagle Industry

- Dae Dong Paper

- Hunan Xiangfeng Special Paper

- Isparta Filtre

- LTR Industries

- Nantong Nengda Special Paper

- 新興企業和專業公司

- BMJ Paper

- Cerdia Brazil Facility

- Filtrona Indonesia

- Glatz Feinpapier

- Kao Collins

- Papierfabrik Wattens

- Republic Technologies International

The Global Cigarette Filter Market was valued at USD 3.79 billion in 2025 and is estimated to grow at a CAGR of 3.6% to reach USD 5.2 billion by 2035.

Growth across the global cigarette filters industry continues to accelerate as consumers become increasingly aware of the health concerns linked to smoking and seek products designed to reduce exposure to harmful substances. Filters are widely incorporated into cigarettes to lower the intake of tar, nicotine, and other toxic compounds, making them an essential component across the tobacco sector. Rising smoking rates in several developing economies, along with continuous advancements in filtration materials and production technologies, are supporting industry expansion. Regulatory policies introduced by governments worldwide are also influencing market development, as manufacturers are required to comply with stricter standards aimed at reducing smoking-related health risks. This regulatory pressure is encouraging companies to invest in advanced filtration solutions and next-generation materials. Sustainability trends are further transforming the cigarette filter industry, with growing demand for eco-conscious alternatives encouraging the development of biodegradable and environmentally safer filter products. Manufacturers are increasingly focusing on sustainable innovations to align with evolving consumer preferences and environmental expectations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.79 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 3.6% |

In 2025, the cellulose acetate segment accounted for USD 3.6 billion and is anticipated to grow at a CAGR of 3.7% through 2035. Demand for cellulose acetate filters continues to increase because of their strong filtration performance, affordability, and widespread adoption within cigarette manufacturing. Increased public awareness regarding the harmful effects of smoking has also encouraged the development of enhanced filter technologies, creating favorable growth opportunities for cellulose acetate-based products. The segment is additionally benefiting from rising interest in materials considered more environmentally acceptable than traditional plastic-based cigarette filters. Ongoing product innovations and improvements in biodegradable filter solutions are expected to further strengthen the market outlook for cellulose acetate filters during the coming years.

The cigarette segment held a 61% share in 2025 and is forecast to grow at a CAGR of 53% between 2026 and 2035. Expansion within the cigarette filter industry is being driven by stronger consumer focus on reducing exposure to harmful smoking substances. Filters have become increasingly common as manufacturers work toward lowering tar and nicotine levels in tobacco products. Technological progress involving advanced filtration materials, including activated carbon and sustainable alternatives, continues to create new growth opportunities across the industry. In addition, government regulations aimed at reducing the health impact associated with smoking are encouraging wider adoption of innovative cigarette filter technologies and supporting long-term market development.

U.S. Cigarette Filter Market accounted for 77% share in 2025 and generated USD 315.4 million. Market performance across the United States is shaped by changing consumer preferences, regional smoking patterns, and evolving regulatory frameworks. Certain regions continue to support industry demand due to relatively higher smoking populations, while other areas experience slower growth because of stricter anti-smoking regulations and stronger public awareness regarding smoking-related health risks. The growing preference for biodegradable cigarette filters is also influencing purchasing behavior in several parts of the country, encouraging manufacturers to expand their portfolios with environmentally responsible filtration products. Increasing investments in product innovation and sustainable materials are expected to remain key factors supporting the expansion of the U.S. cigarette filter industry.

Key participants operating in the Global Cigarette Filters Market include Cerdia International, Daicel Corporation, Delfortgroup AG, Filtrona, Julius Glatz, Mativ Holdings, and Miquel y Costas & Miquel. Other notable companies active in the industry include Anji Hengda Paper, Bright Eagle Industry, Dae Dong Paper, Hunan Xiangfeng Special Paper, Isparta Filtre, LTR Industries, and Nantong Nengda Special Paper. Emerging and niche-focused manufacturers participating in the market include BMJ Paper, Cerdia Brazil Facility, Filtrona Indonesia, Glatz Feinpapier, Kao Collins, Papierfabrik Wattens, and Republic Technologies International. Companies operating in the cigarette filter market are implementing several strategic initiatives to strengthen their competitive position and expand their market presence. Leading manufacturers are investing heavily in research and development activities to introduce advanced filtration technologies that improve performance while meeting evolving regulatory standards. Many companies are focusing on biodegradable and sustainable filter materials to address rising environmental concerns and attract eco-conscious consumers. Strategic partnerships, mergers, and regional expansion activities are also helping businesses increase production capabilities and enhance distribution networks.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Filter material

- 2.2.3 Cigarette type

- 2.2.4 Distribution channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Supply chain analysis

- 3.5.1 Raw material sourcing landscape

- 3.5.2 Manufacturing process flow

- 3.5.3 Distribution network structure

- 3.5.4 Supply chain vulnerabilities & risk mitigation

- 3.6 Technology and innovation landscape

- 3.6.1 Biodegradable filter material technologies

- 3.6.2 Micro perforation & ventilation technologies

- 3.6.3 Multi-layered filter design innovations

- 3.6.4 Nanofiber membrane integration

- 3.6.5 Flavor capsule technologies

- 3.7 Pricing analysis (Driven by Primary Research)

- 3.7.1 Historical price trend analysis

- 3.7.2 Pricing strategy by player type

- 3.8 Regulatory framework

- 3.8.1 EU Single-Use Plastics Directive (SUPD) Impact

- 3.8.2 Tobacco Products Directive (2014/40/EU)

- 3.8.3 Regional Filter Material Regulations

- 3.8.4 Extended Producer Responsibility (EPR) Schemes

- 3.8.5 Filter Waste Management Mandates

- 3.9 Trade data analysis (Driven by Paid Database Research) (HS Code-560122)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Impact of AI & generative ai on the market

- 3.10.1 AI-driven disruption of traditional business models

- 3.10.2 GenAI use cases & adoption roadmap by customer segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.10.4 AI-enabled smart home ecosystem integration

- 3.11 Porter's five forces analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Filter Material, 2022 - 2035 ($Billion, Billion Units)

- 5.1 Key trends

- 5.2 Cellulose acetate

- 5.3 Paper

- 5.4 PLA

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Cigarette Type, 2022 - 2035 ($Billion, Billion Units)

- 6.1 Key trends

- 6.2 Cigarette

- 6.2.1 Conventional/king size

- 6.2.2 Super slim

- 6.2.3 Standard/regular

- 6.2.4 Short/mini

- 6.3 Heat-Not-Burn Product (HNB Stick)

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Billion Units)

- 7.1 Key trends

- 7.2 Direct sales

- 7.3 Indirect sales

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Billion Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Cerdia International

- 9.1.2 Daicel Corporation

- 9.1.3 Delfortgroup AG

- 9.1.4 Filtrona

- 9.1.5 Julius Glatz

- 9.1.6 Mativ Holdings

- 9.1.7 Miquel y Costas & Miquel

- 9.2 Regional Players

- 9.2.1 Anji Hengda Paper

- 9.2.2 Bright Eagle Industry

- 9.2.3 Dae Dong Paper

- 9.2.4 Hunan Xiangfeng Special Paper

- 9.2.5 Isparta Filtre

- 9.2.6 LTR Industries

- 9.2.7 Nantong Nengda Special Paper

- 9.3 Emerging/Niche Specialists

- 9.3.1 BMJ Paper

- 9.3.2 Cerdia Brazil Facility

- 9.3.3 Filtrona Indonesia

- 9.3.4 Glatz Feinpapier

- 9.3.5 Kao Collins

- 9.3.6 Papierfabrik Wattens

- 9.3.7 Republic Technologies International

菸草市場:產品類型、口味特徵、成分、年齡層、通路、性別-2026-2032年全球市場預測

菸草市場:產品類型、口味特徵、成分、年齡層、通路、性別-2026-2032年全球市場預測 菸草市場報告:按類型、分銷管道和地區分類(2026-2034 年)薄荷醇菸草市場報告:按膠囊類型、最終用戶、規模、分銷管道和地區分類(2026-2034 年)菸草紙市場:2026-2032年全球市場預測(依原料、產品類型、包裝、應用及銷售管道分類)紙煙紙和煙嘴紙市場:依產品類型、厚度、材料類型、通路、最終用戶分類,全球預測(2026-2032年)

菸草市場報告:按類型、分銷管道和地區分類(2026-2034 年)薄荷醇菸草市場報告:按膠囊類型、最終用戶、規模、分銷管道和地區分類(2026-2034 年)菸草紙市場:2026-2032年全球市場預測(依原料、產品類型、包裝、應用及銷售管道分類)紙煙紙和煙嘴紙市場:依產品類型、厚度、材料類型、通路、最終用戶分類,全球預測(2026-2032年) 2026-2034年全球薄荷醇菸草市場規模、佔有率、趨勢和成長分析報告日本菸草市場規模、佔有率、趨勢和預測:按類型、通路和地區分類,2026-2034年

2026-2034年全球薄荷醇菸草市場規模、佔有率、趨勢和成長分析報告日本菸草市場規模、佔有率、趨勢和預測:按類型、通路和地區分類,2026-2034年 菸草市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、銷售管道、地區及競爭格局分類,2021-2031年)

菸草市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、銷售管道、地區及競爭格局分類,2021-2031年) 2026-2030年全球菸草市場煙草包裝市場按產品類型、包裝類型、口味和分銷管道分類,全球預測(2026-2032年)

2026-2030年全球菸草市場煙草包裝市場按產品類型、包裝類型、口味和分銷管道分類,全球預測(2026-2032年)