|

市場調查報告書

商品編碼

2045656

無菌瓶裝灌裝機市場機會、成長要素、產業趨勢分析及2026-2035年預測Aseptic Bottle Filling Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

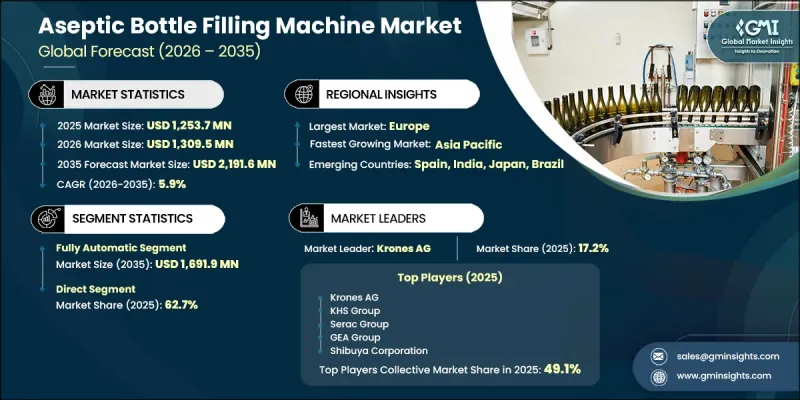

2025年全球無菌瓶裝灌裝機市值12.537億美元,預計2035年將以5.9%的複合年成長率成長至21.916億美元。

生物製藥、疫苗和無菌藥品需求的不斷成長,正加速醫療保健產業對先進無菌填充技術的應用。製造商正大幅增加對尖端灌裝系統和污染預防技術的投資,以確保在整個生產週期中安全無菌地處理產品。不斷發展的食品飲料產業也推動了市場成長,因為消費者越來越傾向於選擇不含防腐劑、保存期限長、品質優良的產品。無菌填充系統有助於製造商在滿足嚴格的衛生和包裝標準的同時,保持產品品質。監管機構正在收緊滅菌和隔離要求,敦促企業用先進合規的系統取代過時的設備。對營運效率、自動化、產品安全和法規遵循的日益重視,持續為全球無菌瓶裝灌裝機產業創造機會。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 12.537億美元 |

| 預計金額 | 21.916億美元 |

| 複合年成長率 | 5.9% |

預計到2025年,全自動灌裝設備市場規模將達到9.592億美元,2035年將達到16.919億美元。全自動無菌灌裝機憑藉著保持高無菌性和製程精度的能力,持續引領產業發展。這些系統顯著減少了填充過程中的人工直接接觸,最大限度地降低了污染風險,並提高了生產的可靠性。自動化技術還能確保整個生產週期內灌裝速度均勻、密封精準、產品處理穩定,進而帶來更高的操作一致性。這種一致性對於旨在符合嚴格的國際品質和安全標準的製造商至關重要。製藥和食品加工企業自動化程度的不斷提高,進一步推動了對全自動無菌填充設備的需求。

預計到2025年,直銷通路將佔62.7%的市佔率。由於無菌填充系統需要高度專業化的工程和技術整合,直接採購仍然是首選的銷售方式。客戶在投資先進的灌裝設備之前,通常需要全面的諮詢和客製化的系統配置。製造商通常直接與終端用戶合作,以確保機器規格符合營運要求、設施結構和生產能力。客製化的系統設計在大規模生產環境中也至關重要,因為設備必須適應特定的加工特性和包裝要求。無菌灌裝機械的技術複雜性限制了第三方經銷商的作用,因為買家通常更傾向於直接與原始設備製造商 (OEM) 合作,以獲得更好的技術指導和長期的支援服務。

預計到2025年,美國無菌瓶裝灌裝機市佔率將達81.6%。這一強勁的市場成長主要得益於包裝營養品、乳製品飲料和即飲產品消費量的成長,這些產品均需要無菌包裝解決方案。食品和飲料製造商越來越重視無菌生產環境,以符合監管機構制定的嚴格食品安全和驗證標準。此外,自動化技術和工業4.0解決方案的快速普及也推動了對先進無菌填充設備的投資,從而提高了可追溯性、營運效率和合規性。美國和加拿大生產設施中老舊包裝基礎設施的現代化改造也促進了全部區域市場的持續擴張。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 對無菌和無污染包裝的需求日益成長

- 增加可在室溫下儲存且不含防腐劑的產品的消耗量

- 加強對衛生、可追溯性和過程驗證的監管要求。

- 產業潛在風險與挑戰

- 高昂的初始投資成本

- 嚴格的監管要求和合規標準

- 機會

- 擴大乳製品替代品、機能飲料和營養保健品市場

- 實施自動化、數位化監控和工業4.0解決方案

- 促進因素

- 成長潛力分析

- 監理框架

- 關鍵市場趨勢與顛覆性因素

- 技術與創新展望

- 價格分析

- 對過去價格趨勢的分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 未來市場趨勢

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 波特的分析

- PESTLE分析

- 生產能力和生產情況

- 按地區和主要製造商分類的無菌瓶填充能力

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依技術分類,2022-2035年

- 旋轉式無菌填充系統

- 線性無菌填充系統

- 其他

第6章 市場估計與預測:依營運模式分類,2022-2035年

- 全自動

- 半自動

第7章 市場估計與預測:依產能分類,2022-2035年

- 每小時最多可處理 10,000 瓶

- 每小時 10,000 至 25,000 個單位

- 每小時 25,000 至 50,000 瓶

- 每小時超過5萬瓶

第8章 市場估算與預測:依整合類型分類,2022-2035年

- 獨立式灌裝系統

- 整合單體系統

第9章 市場估算與預測:依滅菌技術分類,2022-2035年

- 化學滅菌

- 基於能量的滅菌

- 複雜/多方法系統

第10章 市場估價與預測:依應用領域分類,2022-2035年

- 塑膠瓶

- 寶特瓶灌裝

- 填充高密度聚乙烯瓶

- 灌裝PP瓶

- 玻璃瓶

- 其他(金屬瓶、多層瓶、特殊瓶子)

第11章 市場估計與預測:依最終用途產業分類,2022-2035年

- 製藥

- 化妝品產業

- 食品/飲料

- 生物技術

- 其他(化學品等)

第12章 市場估計與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第13章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第14章:公司簡介

- 世界公司

- GEA Group

- KHS Group

- Krones AG

- Serac Group

- Shibuya Corporation

- Syntegon

- Tetra Pak

- 當地公司

- Aseptic Systems Co., Ltd.

- Dara Pharma

- Groninger Holding GmbH & Co. KG

- Plumat

- Romaco Group

- SMI Group

- Watson-Marlow/Flexicon

- 新興企業

- Cozzoli Machine Company

- NJM Packaging

- Newamstar Packaging Machinery

- Tech-Long Packaging Machinery

- Trepko

- Weiler Engineering, Inc.

- Zhangjiagang King Machine

The Global Aseptic Bottle Filling Machine Market was valued at USD 1,253.7 million in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 2,191.6 million by 2035.

Rising demand for biologics, vaccines, and sterile pharmaceutical products continues to accelerate the adoption of advanced aseptic filling technologies across the healthcare sector. Manufacturers are significantly increasing investments in modern filling systems and contamination control technologies to ensure safe and sterile product handling throughout the production cycle. The evolving food and beverage sector is also contributing to market growth as consumers increasingly prefer preservative-free products with extended shelf life and high product integrity. Aseptic filling systems help manufacturers maintain product quality while meeting strict hygiene and packaging standards. Regulatory authorities have strengthened sterilization and containment requirements, encouraging companies to replace outdated machinery with advanced, compliant systems. Growing emphasis on operational efficiency, automation, product safety, and regulatory adherence continues to create favorable opportunities for the aseptic bottle filling machine industry worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1,253.7 Million |

| Forecast Value | $2,191.6 Million |

| CAGR | 5.9% |

The fully automatic segment generated USD 959.2 million in 2025 and is expected to reach USD 1,691.9 million by 2035. Fully automated aseptic bottle filling machines continue to dominate the industry due to their ability to maintain high levels of sterility and process precision. These systems significantly reduce direct human interaction during the filling process, minimizing contamination risks and improving production reliability. Automated technologies also deliver greater operational consistency by ensuring uniform filling speed, accurate sealing, and stable product handling throughout production cycles. Such consistency is essential for manufacturers aiming to comply with strict international quality and safety standards. Increasing adoption of automation across pharmaceutical and food processing facilities is further strengthening demand for fully automatic aseptic filling equipment.

The direct sales segment accounted for 62.7% share in 2025. Direct purchasing channels remain the preferred sales approach because aseptic filling systems involve highly specialized engineering and technical integration requirements. Customers typically require extensive consultation and customized system configuration before investing in advanced filling equipment. Manufacturers often work directly with end users to ensure machinery specifications align with operational requirements, facility structures, and production capacities. Customized system design also plays an important role in large-scale production environments where equipment must accommodate specific processing characteristics and packaging requirements. The technical complexity associated with aseptic machinery limits the role of third-party distributors, as buyers generally prefer direct engagement with original equipment manufacturers for better technical guidance and long-term support services.

United States Aseptic Bottle Filling Machine Market accounted for 81.6% share in 2025. Strong market growth across the country is primarily supported by rising consumption of packaged nutritional products, dairy-based beverages, and ready-to-consume products requiring sterile packaging solutions. Food and beverage manufacturers are increasingly prioritizing contamination-free production environments to comply with strict food safety and validation standards established by regulatory authorities. Additionally, the rapid integration of automation technologies and Industry 4.0 solutions is encouraging investments in advanced aseptic filling equipment capable of improving traceability, operational efficiency, and regulatory compliance. Replacement of aging packaging infrastructure across production facilities in the United States and Canada is also contributing to continued market expansion throughout the region.

Major companies operating in the Global Aseptic Bottle Filling Machine Market include Aseptic Systems Co., Ltd., Cozzoli Machine Company, Dara Pharma, GEA Group, Groninger Holding GmbH & Co. KG, KHS Group, Krones AG, Newamstar Packaging Machinery, NJM Packaging, Plumat, Romaco Group, Serac Group, Shibuya Corporation, SMI Group, Syntegon, Tech-Long Packaging Machinery, Tetra Pak, Trepko, Watson-Marlow / Flexicon, Weiler Engineering, Inc., and Zhangjiagang King Machine. Companies operating in the aseptic bottle filling machine industry are adopting several strategic initiatives to strengthen their market presence and improve competitive positioning. Leading manufacturers are investing heavily in automation technologies, robotic integration, and smart monitoring systems to enhance production efficiency and reduce contamination risks. Product innovation remains a major focus area, with companies developing advanced filling systems capable of supporting higher throughput and improved sterilization performance. Strategic partnerships, mergers, and regional expansion initiatives are also helping market participants increase customer reach and strengthen distribution capabilities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.9 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 By Technology

- 2.2.3 By Mode Of Operation

- 2.2.4 By Output Capacity

- 2.2.5 By Integration Type

- 2.2.6 By Sterilization Technology

- 2.2.7 By Application

- 2.2.8 By End Use Industry

- 2.2.9 By Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surging demand for increasing demand for sterile contamination free packaging

- 3.2.1.2 Rising consumption of shelf-stable and preservative-free products

- 3.2.1.3 Stricter regulatory requirements for hygiene, traceability, and process validation

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Stringent regulatory requirements and compliance standards

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of dairy alternatives, functional beverages, and nutraceuticals

- 3.2.3.2 Adoption of automation, digital monitoring, and industry 4.0 solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory framework

- 3.5 Major market trends and disruptions

- 3.6 Technology/innovation landscape

- 3.7 Pricing Analysis (driven by primary research)

- 3.7.1 Historical price trend analysis (driven by primary research)

- 3.7.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.8 Future market trends

- 3.9 Trade data analysis (driven by paid database) (HS code- 8422.30)

- 3.9.1 Import/export volume & value trends (driven by primary research)

- 3.9.2 Key trade corridors & tariff impact (driven by primary research)

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 Gen-AI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Aseptic Bottle Filling Capacity by Region & Key Producer (Driven by Primary Research)

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035 (USD Million, Thousand Units)

- 5.1 Key trends

- 5.2 Rotary aseptic filling systems

- 5.3 Linear aseptic filling systems

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By Mode of Operation, 2022 - 2035 (USD Million, Thousand Units)

- 6.1 Key trends

- 6.2 Fully automatic

- 6.3 Semi-automatic

Chapter 7 Market Estimates & Forecast, By Output Capacity, 2022 - 2035 (USD Million, Thousand Units)

- 7.1 Key trends

- 7.2 Up to 10,000 Bottles/Hr

- 7.3 10,000 to 25,000 Bottles/Hr

- 7.4 25,000 to 50,000 Bottles/Hr

- 7.5 Above 50,000 Bottles/Hr

Chapter 8 Market Estimates & Forecast, By Integration Type, 2022 - 2035 (USD Million, Thousand Units)

- 8.1 Key trends

- 8.2 Standalone filling systems

- 8.3 Integrated monobloc systems

Chapter 9 Market Estimates & Forecast, By Sterilization Technology, 2022 - 2035 (USD Million, Thousand Units)

- 9.1 Key trends

- 9.2 Chemical sterilization

- 9.3 Energy-based sterilization

- 9.4 Combination/multi-method systems

Chapter 10 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Million, Thousand Units)

- 10.1 Key trends

- 10.2 Plastic bottle

- 10.2.1 PET bottle filling

- 10.2.2 HDPE bottle filling

- 10.2.3 PP bottle filling

- 10.3 Glass bottle

- 10.4 Others (metallic, multilayer & specialty bottle)

Chapter 11 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 (USD Million, Thousand Units)

- 11.1 Key trends

- 11.2 Pharmaceutical

- 11.3 Cosmetic industries

- 11.4 Food and beverages

- 11.5 Biotechnology

- 11.6 Others (chemical etc.)

Chapter 12 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Million, Thousand Units)

- 12.1 Key trends

- 12.2 Direct sales

- 12.3 Indirect sales

Chapter 13 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Million, Thousand Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Spain

- 13.3.5 Italy

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 Japan

- 13.4.3 India

- 13.4.4 Australia

- 13.4.5 South Korea

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.6 MEA

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Global Companies

- 14.1.1 GEA Group

- 14.1.2 KHS Group

- 14.1.3 Krones AG

- 14.1.4 Serac Group

- 14.1.5 Shibuya Corporation

- 14.1.6 Syntegon

- 14.1.7 Tetra Pak

- 14.2 Regional Companies

- 14.2.1 Aseptic Systems Co., Ltd.

- 14.2.2 Dara Pharma

- 14.2.3 Groninger Holding GmbH & Co. KG

- 14.2.4 Plumat

- 14.2.5 Romaco Group

- 14.2.6 SMI Group

- 14.2.7 Watson-Marlow / Flexicon

- 14.3 Emerging Companies

- 14.3.1 Cozzoli Machine Company

- 14.3.2 NJM Packaging

- 14.3.3 Newamstar Packaging Machinery

- 14.3.4 Tech-Long Packaging Machinery

- 14.3.5 Trepko

- 14.3.6 Weiler Engineering, Inc.

- 14.3.7 Zhangjiagang King Machine

雙腔注射器填充機市場:依自動化類型、材料類型和最終用戶分類-2026-2032年全球市場預測

雙腔注射器填充機市場:依自動化類型、材料類型和最終用戶分類-2026-2032年全球市場預測 無菌灌裝機市場規模、佔有率和趨勢分析報告:按包裝、運作方法、最終用途、地區和細分市場預測(2026-2033 年)藥品滅菌液體灌裝機市場:依機器類型、技術、包裝形式、填充量、應用、最終用戶分類,全球預測(2026-2032年)食品薄膜封裝包裝機市場按類型、薄膜材料、包裝方法、應用和最終用途產業分類-全球預測,2026-2032年

無菌灌裝機市場規模、佔有率和趨勢分析報告:按包裝、運作方法、最終用途、地區和細分市場預測(2026-2033 年)藥品滅菌液體灌裝機市場:依機器類型、技術、包裝形式、填充量、應用、最終用戶分類,全球預測(2026-2032年)食品薄膜封裝包裝機市場按類型、薄膜材料、包裝方法、應用和最終用途產業分類-全球預測,2026-2032年 無菌灌裝機市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、操作模式、產業、地區和競爭格局分類,2021-2031年全球薄膜封口機市場(依機器類型、最終用戶、包裝材料、封口類型和自動化程度分類)-2026-2032年預測自動蛋糕裱花機市場按類型、動力來源、容量、應用、最終用戶和分銷管道分類-2026-2032年全球預測

無菌灌裝機市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、操作模式、產業、地區和競爭格局分類,2021-2031年全球薄膜封口機市場(依機器類型、最終用戶、包裝材料、封口類型和自動化程度分類)-2026-2032年預測自動蛋糕裱花機市場按類型、動力來源、容量、應用、最終用戶和分銷管道分類-2026-2032年全球預測 替代化糞池系統市場,按系統類型、最終用戶、國家和地區分類 - 全球產業分析、市場規模、市場佔有率及2025-2032年預測醫藥用無菌灌裝袋市場-全球產業規模、佔有率、趨勢、機會及預測,依袋型、技術、最終用戶、地區及競爭格局分類,2020-2030年預測

替代化糞池系統市場,按系統類型、最終用戶、國家和地區分類 - 全球產業分析、市場規模、市場佔有率及2025-2032年預測醫藥用無菌灌裝袋市場-全球產業規模、佔有率、趨勢、機會及預測,依袋型、技術、最終用戶、地區及競爭格局分類,2020-2030年預測 無菌填充和密封系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

無菌填充和密封系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測