|

市場調查報告書

商品編碼

2038786

舷外機市場商機、成長要素、產業趨勢分析及2026-2035年預測。Outboard Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

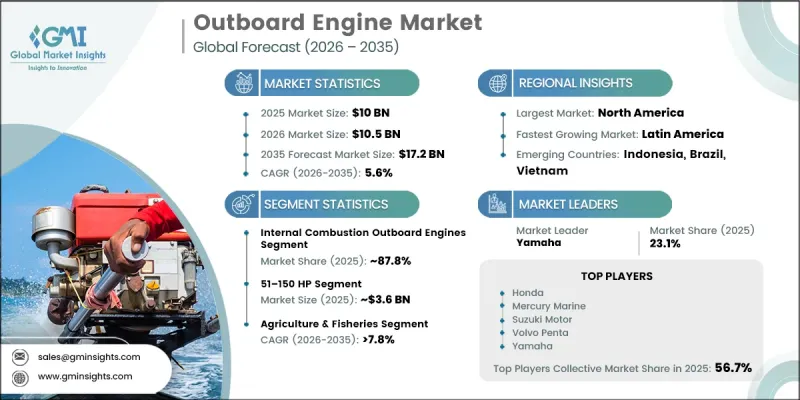

全球舷外機市場預計到 2025 年將價值 100 億美元,預計到 2035 年將以 5.6% 的複合年成長率成長至 172 億美元。

市場成長主要受海洋旅遊日益普及的推動,尤其是在沿海地區,休閒划船和釣魚活動持續發展。地方政府也增加對海洋旅遊基礎設施的投資,進一步刺激了對舷外機(也稱為舷外馬達)的需求。此外,商業捕魚和政府海上作業的穩定需求也支撐著市場的長期穩定。小型船舶因其機動性和成本效益而被廣泛使用,這持續推動舷外機在漁業領域的應用。海事部門和海岸警衛隊也依賴這些引擎,因為它們具有高速性能、適用於淺水作業以及易於維護和更換等優點。同時,該市場的產品開發也日益受到嚴格的排放氣體法規和燃油效率標準的影響。主要經濟體環保部門制定的法律規範正在加速向先進燃油噴射系統和四衝程引擎技術的過渡,取代老舊的二行程配置,並推動整個行業的現代化。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 100億美元 |

| 預測金額 | 172億美元 |

| 複合年成長率 | 5.6% |

預計2025年,內燃機市佔率將達到87.8%,市場規模將達88億美元。該細分市場之所以保持主導地位,是因為其強大的動力輸出、可靠的運作性能以及完善的燃料供應基礎設施,能夠支援廣泛的船舶應用。特別是四衝程內燃機系統,因其在休閒、商用船舶和政府船舶營運中持續穩定的動力輸出而備受青睞。與新興的電動引擎相比,它們在海上作業和遠洋航行中的卓越性能使其應用更為廣泛。

預計到2025年,51-150馬力細分市場的佔有率將達到36.4%,市場規模將達到36億美元。該馬力範圍因其燃油效率和動力性能的平衡而廣受歡迎。它能有效滿足休閒船艇和小規模商業用途的需求,並為各種類型的船舶提供適當的推進力。其在中型休閒船艇和多用途船艇中的多功能性,使其成為尋求經濟高效的船舶推進解決方案的個人用戶和小規模企業廣泛採用的選擇。

美國舷外機市場預計到2025年將達到35億美元,並在2026年至2035年間以4.4%的複合年成長率成長。由於美國擁有濃厚的航海文化和廣泛的內陸及沿海水道網路,因此仍是最大的國內市場。休閒航海的普及和大量的註冊船舶確保了舷外機需求的穩定。此外,遍布美國的湖泊、河流和沿海地區也為引擎銷售的持續成長做出了重要貢獻,尤其是在高功率和四行程引擎領域。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 休閒划船和水上運動活動的擴展

- 對節能環保引擎的需求日益成長。

- 商業和工業船舶運營的擴展

- 舷外機設計與性能的技術進步

- 產業潛在風險與挑戰

- 對海洋排放氣體的嚴格規定

- 電動舷外機的續航里程有限。

- 市場機遇

- 電氣化和混合整合

- 新興市場對可攜式舷外機的需求

- 生態旅遊和永續船舶使用的成長

- 促進因素

- 技術趨勢與創新生態系統

- 目前技術

- 先進燃油噴射系統

- 用於海水的耐腐蝕材料

- 數位引擎監控和智慧控制

- 新興技術

- 電動和混合動力舷外機推進系統

- 輕質複合材料

- 模組化可攜式電源裝置

- 聯網舷外機(物聯網整合)

- 目前技術

- 成長潛力分析

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按球員類型分類的定價策略(高階/超值/成本加成)

- 監理情勢

- 北美洲

- 美國環保署引擎排放氣體標準

- 加拿大海事安全局,運輸部

- 歐洲

- 歐盟 - 歐盟委員會 -休閒船舶指令 (RCD)

- 德國 - 聯邦海事和水文局 (BSH)

- 亞太地區

- 中國 - 中國船級社(CCS)

- 澳洲 - 澳洲海事安全局 (AMSA)

- 拉丁美洲

- 巴西 - 巴西海軍港口和海岸管理局 (DPC)

- 墨西哥 - 環境與自然資源部 (SEMARNAT)

- 中東和非洲

- 阿拉伯聯合大公國 - 阿拉伯聯合大公國能源和基礎設施部

- 沙烏地阿拉伯 - 沙烏地阿拉伯港務局

- 北美洲

- 波特五力分析

- PESTEL 分析

- 專利分析(基於初步研究)

- 交易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易走廊及關稅的影響

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的已安裝產能

- 設備運轉率和擴建計劃

- 成本細分分析

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按收入、地區和創新能力分類的層級定位矩陣。

第5章 市場估算與預測:驅動系統/能源類型,2022-2035年

- 內燃機

- 二行程

- 四衝程

- 電力推進

- 天然氣(液化石油氣/壓縮天然氣)

第6章 市場估計與預測:依馬力分類,2022-2035年

- 不到50馬力

- 51-150馬力

- 150馬力或以上

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 政府

- 軍隊

- 海岸警衛隊

- 巡邏

- 救援

- 公共服務船舶

- 緊急/災難救援船

- 休閒和個人用途

- 水上活動(滑水、尾波滑水、運動艇)

- 休閒釣

- 用於健身和戶外活動的船隻

- 觀光和租賃船隻船隊

- 休閒、運動和旅遊

- 個人遊艇(用於遊艇/附屬艇)

- 工業的

- 貨物運輸

- 客運

- 海上作業/支援船

- 作業船

- 農業/漁業

- 內陸漁船

- 水產養殖支援船

- 灌溉和農村船舶

第8章 市場估算與預測:以點火法分類,2022-2035年

- 電的

- 手動的

第9章 市場估價與預測:依通路分類,2022-2035年

- 海洋航行

- 政府

- 軍隊

- 海岸警衛隊

- 巡邏

- 救援

- 公共服務船舶

- 緊急/災難救援船

- 休閒和個人用途

- 水上活動(滑水、尾波滑水、運動艇)

- 休閒釣

- 用於健身和戶外活動的船隻

- 觀光和租賃船隻船隊

- 休閒、運動和旅遊

- 個人遊艇(用於遊艇/附屬艇)

- 工業的

- 貨物運輸

- 客運

- 海上作業/支援船

- 作業船

- 農業/漁業

- 內陸漁船

- 水產養殖支援船

- 灌溉和農村船舶

- 政府

- 內陸

- 政府

- 軍隊

- 海岸警衛隊

- 巡邏

- 救援

- 公共服務船舶

- 緊急/災難救援船

- 休閒和個人用途

- 水上活動(滑水、尾波滑水、運動艇)

- 休閒釣

- 用於健身和戶外活動的船隻

- 觀光和租賃船隻船隊

- 休閒、運動和旅遊

- 個人遊艇(用於遊艇/附屬艇)

- 工業的

- 貨物運輸

- 客運

- 海上作業/支援船

- 作業船

- 農業/漁業

- 內陸漁船

- 水產養殖支援船

- 灌溉和農村船舶

- 政府

第10章 市場估價與預測:依銷售管道分類,2022-2035年

- OEM

- 售後市場

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 匈牙利

- 希臘

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 世界公司

- Yamaha Motor

- Mercury Marine

- Honda Motor

- Suzuki Motor

- Tohatsu

- Volvo Penta

- Torqeedo

- Parsun Power Machine

- Hidea Power Machinery

- Selva

- 當地公司

- Hangkai

- Changchai Company

- Cox Powertrain

- ePropulsion

- Aquawatt

- Briggs & Stratton

- 新興企業

- Caudwell Marine

- Zhejiang Anqidi Power Machinery

- Jinhua Himarine Machinery

- Boatee

The Global Outboard Engine Market was valued at USD 10 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 17.2 billion by 2035.

Market growth is supported by the rising popularity of marine tourism, particularly across coastal regions, where recreational boating and fishing activities continue to expand. Governments across various regions are also investing in marine-based tourism infrastructure, further strengthening demand for outboard engines, also known as outboard motors. In addition, steady demand from commercial fishing and government maritime operations is sustaining long-term market stability. Small watercraft remain widely used due to their mobility and cost efficiency, which continues to support outboard engine adoption across fishing applications. Maritime authorities and coastal security agencies also rely on these engines due to their high-speed capability, shallow water operation advantage, and ease of maintenance and replacement. At the same time, product development in this market is increasingly influenced by strict emissions regulations and fuel efficiency standards. Regulatory frameworks established by environmental authorities in major economies are accelerating the transition toward advanced fuel injection systems and four-stroke engine technologies, replacing older two-stroke configurations and driving modernization across the industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10 Billion |

| Forecast Value | $17.2 Billion |

| CAGR | 5.6% |

The internal combustion engine segment accounted for 87.8% share in 2025, generating USD 8.8 billion. This segment remains dominant due to its strong power output, operational reliability, and established fueling infrastructure that supports a wide range of marine applications. Four-stroke internal combustion systems are particularly preferred for their ability to deliver consistent horsepower across recreational, commercial, and government marine operations. Their strong performance in offshore conditions and long-distance marine travel continues to make them more widely adopted compared to emerging electric alternatives.

The 51-150 HP segment held 36.4% share in 2025, valued at USD 3.6 billion. This horsepower range is widely preferred due to its balanced combination of fuel efficiency and operational power. It effectively supports both recreational boating and small-scale commercial use, offering suitable propulsion for a variety of vessel types. Its versatility across mid-sized recreational boats and utility watercraft makes it a widely adopted category among both individual users and small business operators seeking cost-effective marine propulsion solutions.

U.S. Outboard Engine Market reached USD 3.5 billion in 2025 and is projected to grow at a CAGR of 4.4% from 2026 to 2035. The country continues to represent the largest national market due to its strong boating culture and extensive network of inland and coastal waterways. High levels of recreational boating activity and a large registered boat population support consistent demand for outboard engines. In addition, lakes, rivers, and coastal zones across the country contribute significantly to sustained engine sales, particularly in higher horsepower and four-stroke engine categories.

Key companies operating in the Outboard Engine Market include Yamaha, Honda, Brunswick, Suzuki Motor, Volvo Penta, Yanmar, Torqeedo, Tohatsu, Oxe Marine, and Parsun Power Machine. Companies in the Outboard Engine Market are focusing on developing fuel-efficient and low-emission propulsion systems to comply with tightening environmental regulations. Significant investments in engine electrification and hybrid propulsion technologies are being made to align with future sustainability goals. Manufacturers are also enhancing product durability and corrosion resistance to improve performance in harsh marine environments. Expansion of service networks and aftermarket support is being prioritized to strengthen customer retention and long-term brand loyalty. Strategic collaborations with boat manufacturers are enabling better product integration and increased market penetration. In addition, companies are focusing on lightweight engine designs and advanced fuel injection systems to improve performance efficiency. Digital monitoring solutions and smart engine diagnostics are also being introduced to enhance user experience and predictive maintenance capabilities across marine applications.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Propulsion

- 2.2.3 Horsepower

- 2.2.4 Application

- 2.2.5 Ignition

- 2.2.6 Waterways

- 2.2.7 Sales channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing recreational boating and water sports activities

- 3.2.1.2 Increasing demand for fuel-efficient and eco-friendly engines

- 3.2.1.3 Expansion of commercial and industrial marine operations

- 3.2.1.4 Technological advancements in outboard engine design and performance

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Stringent marine emission regulations

- 3.2.2.2 Limited range for electric outboards

- 3.2.3 Market opportunities

- 3.2.3.1 Electrification & hybrid integration

- 3.2.3.2 Demand for portable outboards in emerging markets

- 3.2.3.3 Growth in eco-tourism & sustainable boating

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Advanced fuel injection systems

- 3.3.1.2 Corrosion-resistant materials for saltwater use

- 3.3.1.3 Digital engine monitoring & smart controls

- 3.3.2 Emerging technologies

- 3.3.2.1 Electric & hybrid outboard propulsion

- 3.3.2.2 Lightweight composite materials

- 3.3.2.3 Modular & portable power units

- 3.3.2.4 Connected outboards (IoT Integration)

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 US - EPA engine emission standards

- 3.6.1.2 Canada - Transport Canada Marine Safety

- 3.6.2 Europe

- 3.6.2.1 EU - European Commission - Recreational Craft Directive (RCD)

- 3.6.2.2 Germany - Federal Maritime and Hydrographic Agency (BSH)

- 3.6.3 Asia Pacific

- 3.6.3.1 China - China Classification Society (CCS)

- 3.6.3.2 Australia - Australian Maritime Safety Authority (AMSA)

- 3.6.4 Latin America

- 3.6.4.1 Brazil - Brazilian Navy Directorate of Ports and Coasts (DPC)

- 3.6.4.2 Mexico - Secretariat of Environment and Natural Resources (SEMARNAT)

- 3.6.5 Middle East & Africa

- 3.6.5.1 UAE - UAE Ministry of Energy and Infrastructure

- 3.6.5.2 Saudi Arabia - Saudi Ports Authority

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Trade Data Analysis (Driven by Paid Database)

- 3.10.1 Import/Export Volume & Value Trends

- 3.10.2 Key Trade Corridors & Tariff Impact

- 3.11 Capacity & Production Landscape (Driven by Primary Research)

- 3.11.1 Installed Capacity by Region & Key Producer

- 3.11.2 Capacity Utilization Rates & Expansion Pipelines

- 3.12 Cost breakdown analysis

- 3.13 Impact of AI & Generative AI on the Market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Propulsion/Energy Type, 2022- 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Internal combustion

- 5.2.1 2-stroke

- 5.2.2 4-stroke

- 5.3 Electric propulsion

- 5.4 Natural gas (LPG/CNG)

Chapter 6 Market Estimates & Forecast, By Horsepower, 2022- 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Up to 50 HP

- 6.3 51-150 HP

- 6.4 Above 150 HP

Chapter 7 Market Estimates & Forecast, By Application, 2022- 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Government

- 7.2.1 Military

- 7.2.2 Coast guard

- 7.2.3 Patrol

- 7.2.4 Rescue

- 7.2.5 Public service vessels

- 7.2.6 Emergency & disaster relief vessels

- 7.3 Recreational & personal use

- 7.3.1 Water sports (skiing, wakeboarding, sport boating)

- 7.3.2 Recreational fishing

- 7.3.3 Fitness & outdoor activity boating

- 7.3.4 Tourism & rental fleets

- 7.3.4.1 Leisure & sport tourism

- 7.3.5 Private pleasure craft (yachting/tender use)

- 7.4 Industrial

- 7.4.1 Goods transport

- 7.4.2 Passenger transport

- 7.4.3 Offshore operations & support vessels

- 7.4.4 Workboats

- 7.5 Agriculture & fisheries

- 7.5.1 Inland fishery boats

- 7.5.2 Aquaculture support vessels

- 7.5.3 Irrigation & rural utility boats

Chapter 8 Market Estimates & Forecast, By Ignition, 2022- 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Electric

- 8.3 Manual

Chapter 9 Market Estimates & Forecast, By Waterways, 2022- 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Seagoing

- 9.2.1 Government

- 9.2.1.1 Military

- 9.2.1.2 Coast guard

- 9.2.1.3 Patrol

- 9.2.1.4 Rescue

- 9.2.1.5 Public service vessels

- 9.2.1.6 Emergency & disaster relief vessels

- 9.2.2 Recreational & personal use

- 9.2.2.1 Water sports (skiing, wakeboarding, sport boating)

- 9.2.2.2 Recreational fishing

- 9.2.2.3 Fitness & outdoor activity boating

- 9.2.2.4 Tourism & rental fleets

- 9.2.2.4.1 Leisure & sport tourism

- 9.2.2.5 Private pleasure craft (yachting/tender use)

- 9.2.3 Industrial

- 9.2.3.1 Goods transport

- 9.2.3.2 Passenger transport

- 9.2.3.3 Offshore operations & support vessels

- 9.2.3.4 Workboats

- 9.2.4 Agriculture & fisheries

- 9.2.4.1 Inland fishery boats

- 9.2.4.2 Aquaculture support vessels

- 9.2.4.3 Irrigation & rural utility boats

- 9.2.1 Government

- 9.3 Inland

- 9.3.1 Government

- 9.3.1.1 Military

- 9.3.1.2 Coast guard

- 9.3.1.3 Patrol

- 9.3.1.4 Rescue

- 9.3.1.5 Public service vessels

- 9.3.1.6 Emergency & disaster relief vessels

- 9.3.2 Recreational & personal use

- 9.3.2.1 Water sports (skiing, wakeboarding, sport boating)

- 9.3.2.2 Recreational fishing

- 9.3.2.3 Fitness & outdoor activity boating

- 9.3.2.4 Tourism & rental fleets

- 9.3.2.4.1 Leisure & sport tourism

- 9.3.2.5 Private pleasure craft (yachting/tender use)

- 9.3.3 Industrial

- 9.3.3.1 Goods transport

- 9.3.3.2 Passenger transport

- 9.3.3.3 Offshore operations & support vessels

- 9.3.3.4 Workboats

- 9.3.4 Agriculture & fisheries

- 9.3.4.1 Inland fishery boats

- 9.3.4.2 Aquaculture support vessels

- 9.3.4.3 Irrigation & rural utility boats

- 9.3.1 Government

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2022- 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.3.8 Hungary

- 11.3.9 Greece

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global players

- 12.1.1 Yamaha Motor

- 12.1.2 Mercury Marine

- 12.1.3 Honda Motor

- 12.1.4 Suzuki Motor

- 12.1.5 Tohatsu

- 12.1.6 Volvo Penta

- 12.1.7 Torqeedo

- 12.1.8 Parsun Power Machine

- 12.1.9 Hidea Power Machinery

- 12.1.10 Selva

- 12.2 Regional players

- 12.2.1 Hangkai

- 12.2.2 Changchai Company

- 12.2.3 Cox Powertrain

- 12.2.4 ePropulsion

- 12.2.5 Aquawatt

- 12.2.6 Briggs & Stratton

- 12.3 Emerging players

- 12.3.1 Caudwell Marine

- 12.3.2 Zhejiang Anqidi Power Machinery

- 12.3.3 Jinhua Himarine Machinery

- 12.3.4 Boatee

電動舷外機市場規模、佔有率和成長分析:按產品類型、功率輸出、電池類型、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測

電動舷外機市場規模、佔有率和成長分析:按產品類型、功率輸出、電池類型、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測 2026年全球舷外機市場報告

2026年全球舷外機市場報告 全球二行程汽油舷外機市場(按馬力範圍、最終用途、潤滑系統、通路和傾斜機構分類)預測(2026-2032年)2026年全球船用舷外機市場報告

全球二行程汽油舷外機市場(按馬力範圍、最終用途、潤滑系統、通路和傾斜機構分類)預測(2026-2032年)2026年全球船用舷外機市場報告 2026-2030年全球船用外置引擎市場

2026-2030年全球船用外置引擎市場 船用外置引擎市場規模、佔有率及成長分析(按引擎類型、燃料類型、應用及地區分類)-2026-2033年產業預測

船用外置引擎市場規模、佔有率及成長分析(按引擎類型、燃料類型、應用及地區分類)-2026-2033年產業預測 舷外機:全球市佔率排名、總銷售量和需求預測(2025-2031年)

舷外機:全球市佔率排名、總銷售量和需求預測(2025-2031年) 舷外機市場-全球產業規模、佔有率、趨勢、機會和預測,按引擎類型、燃料類型、應用、地區和競爭細分,2020-2030 年預測

舷外機市場-全球產業規模、佔有率、趨勢、機會和預測,按引擎類型、燃料類型、應用、地區和競爭細分,2020-2030 年預測 電動舷外機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測電動舷外馬達市場按功率、船型、技術、應用和最終用戶分類 - 2025-2030 年全球預測

電動舷外機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測電動舷外馬達市場按功率、船型、技術、應用和最終用戶分類 - 2025-2030 年全球預測