|

市場調查報告書

商品編碼

2038784

無塵室技術市場機會、成長要素、產業趨勢分析及2026-2035年預測Cleanroom Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

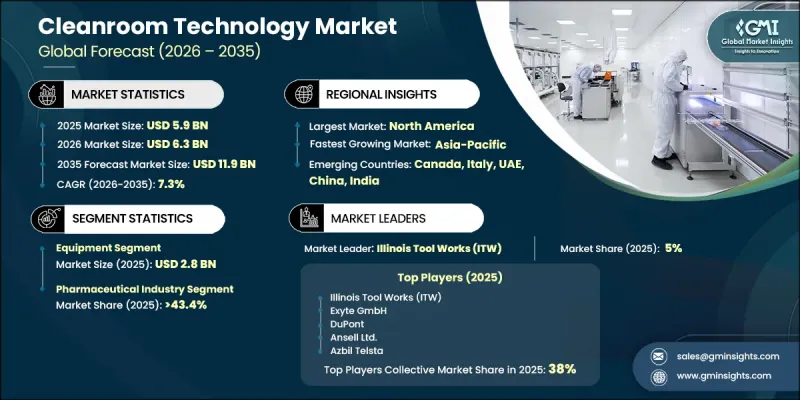

2025年全球無塵室技術市場價值為59億美元,預計2035年將以7.3%的複合年成長率成長至119億美元。

市場成長主要受製藥、生物技術和先進醫療保健製造領域日益嚴格的監管要求和品質合規標準的推動。企業被迫投資高性能無塵室系統,以確保無污染的生產環境並維持監管核准。產品召回、污染風險和生產中斷帶來的成本上升也推動了受控環境的擴展。無塵室技術在複雜治療方法、精密醫療設備和先進生技藥品的生產中變得至關重要,因為產品的完整性和無菌性是關鍵。藥物研發的加速,尤其是在細胞和基因治療領域,進一步增加了對超潔淨生產環境的依賴。這些系統能夠嚴格控制空氣中的顆粒物、溫度穩定性和濕度水平,從而確保產品品質的穩定性。隨著醫療保健產品日益複雜,對高度可控的生產條件的需求不斷成長,無塵室基礎設施在全球生命科學產業的重要性日益凸顯。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 59億美元 |

| 預計金額 | 119億美元 |

| 複合年成長率 | 7.3% |

預計到2025年,設備領域的市場規模將達到28億美元。此領域涵蓋空調機組、過濾解決方案、層流系統、傳輸室和監控設備等關鍵系統。這些技術對於維持醫療和生命科學領域高精度製造流程所需的受控環境至關重要。

預計到2025年,製藥業將佔43.4%的市場。這一主導地位歸功於無塵室設施在無菌藥品和對污染敏感製劑生產的廣泛應用。潔淨室環境在無菌生產過程中至關重要,在整個生產過程中保持無菌狀態是確保產品安全和符合法規要求的必要條件。

美國潔淨室技術市場佔76%的佔有率,預計2025年市場規模將達到15億美元。這一強勁的市場趨勢得益於高度發展的製藥和生物技術行業,以及嚴格的法律規範確保了高標準的生產製造。對生物製造能力,特別是先進治療領域的持續投資,也推動了美國各地對現代化無塵室設施的需求。

目錄

第1章:調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策及對資料完整性的承諾

- 資訊來源一致性協議

- GMI人工智慧政策及對資料完整性的承諾

- 調查軌跡和置信度評分

- 調查和路線的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 每種方法中基準年的計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 關於調查透明度的補充信息

- 資訊來源歸因框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 製藥和生物技術領域的擴張

- 嚴格的監管要求

- 個性化醫療的發展

- 產業潛在風險與挑戰

- 巨額資本投資

- 複雜的維護要求

- 機會

- 模組化潔淨室解決方案

- 智慧監控系統

- 促進因素

- 成長潛力分析

- 監理情勢

- ISO 14644 標準(世界分類)

- cGMP要求(FDA/EMA)

- 21 CFR 第 117 部分(食品加工無塵室)

- 救贖方案

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析(基於初步研究)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 按無塵室類型分類的建造成本基準

- 科技趨勢

- 差距分析

- 波特五力分析

- PESTEL 分析

- 貿易數據分析(基於付費數據來源)

- 進出口數量和價值趨勢(基於初步調查)

- 主要貿易路線及關稅的影響(基於初步調查)

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 細分市場生成式人工智慧用例和實施藍圖

- 風險、限制和監管考量

- 生態系鎖定效應:三星Galaxy生態系與蘋果生態系的分析

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要製造商分類的無塵室裝置容量(基於初步調查)

- 運轉率和擴張計劃(基於初步調查)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 消耗品

- 手套

- 工作服

- 擦拭巾

- 真空系統

- 其他消耗品

- 裝置

- 暖通空調系統

- 潔淨室空氣過濾器

- 層流櫃

- 空氣擴散器和空氣浴塵室

- 透過

- 其他設備

- 結構

- 傳統無塵室

- 模組化潔淨室

- 硬牆

- 軟壁

- 混合

第6章 市場估計與預測:依氣流類型分類,2022-2035年

- 單向氣流(層流)

- 非單向氣流(湍流)

第7章 市場估算與預測:依 ISO 分類,2022-2035 年

- ISO 1-4級(超潔淨)

- ISO 5-6級(無菌處理)

- ISO 7-8級(一般製造業)

- ISO 9級(易於組裝)

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 製藥業

- 生技產業

- 醫療設備業

- 醫院和診所

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 波蘭

- 瑞典

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 印尼

- 菲律賓

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 智利

- 秘魯

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 伊朗

- 以色列

第10章:公司簡介

- 世界主要公司

- Exyte GmbH

- DuPont

- Illinois Tool Works(ITW)

- Ansell Ltd.

- Terra Universal, Inc.

- Azbil Telstar

- KCC Corporation

- 該地區的領先企業

- ABN Cleanroom Technology

- Ardmac

- Clean Air Products

- Labconco Corporation

- Airex Filter Corporation

- Kleanlabs

- Emerging & Specialized Players

- ICLEAN Technologies

- Nicomac Taikisha Clean Rooms

- Kleanlabs

The Global Cleanroom Technology Market was valued at USD 5.9 billion in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 11.9 billion by 2035.

Market growth is strongly influenced by increasingly strict regulatory requirements and quality compliance standards across pharmaceuticals, biotechnology, and advanced healthcare manufacturing sectors. Companies are being compelled to invest in high-performance cleanroom systems to ensure contamination-free production environments and maintain regulatory approvals. Rising costs associated with product recalls, contamination risks, and production failures are also encouraging wider adoption of controlled environments. Cleanroom technologies are becoming essential in the manufacturing of complex therapies, precision medical devices, and advanced biologics, where product integrity and sterility are critical. Growing advancements in drug development, particularly in cell and gene-based therapies, are further increasing reliance on ultra-clean manufacturing environments. These systems enable strict control over airborne particles, temperature stability, and humidity levels, ensuring consistent production quality. The expanding complexity of healthcare products and the need for highly controlled manufacturing conditions continue to reinforce the importance of cleanroom infrastructure across global life sciences industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.9 Billion |

| Forecast Value | $11.9 Billion |

| CAGR | 7.3% |

The equipment segment accounted for USD 2.8 billion in 2025. This segment includes essential systems such as air handling units, filtration solutions, laminar airflow systems, transfer chambers, and monitoring instruments. These technologies are critical for maintaining controlled environments required in high-precision manufacturing operations across healthcare and life sciences sectors.

The pharmaceutical sector held a 43.4% share in 2025. This dominance is attributed to the extensive use of cleanroom facilities in the production of sterile medicines and contamination-sensitive formulations. Cleanroom environments are particularly important in aseptic manufacturing processes, where maintaining sterility throughout production is essential to ensure product safety and regulatory compliance.

U.S. Cleanroom Technology Market held a 76.% share, generating USD 1.5 billion in 2025. Strong market performance is supported by a highly developed pharmaceutical and biotechnology sector, along with strict regulatory oversight that enforces high manufacturing standards. Continuous investment in biomanufacturing capacity, particularly in advanced therapeutic areas, is also driving demand for modern cleanroom facilities across the country.

Key companies operating in the Global Cleanroom Technology Market include Exyte GmbH, DuPont, Illinois Tool Works (ITW), Ansell Ltd., Terra Universal, Inc., Azbil Telstar, KCC Corporation, ABN Cleanroom Technology, Ardmac, Clean Air Products, Labconco Corporation, Airex Filter Corporation, Kleanlabs, ICLEAN Technologies, and Nicomac Taikisha Clean Rooms. Companies in the Cleanroom Technology Market are focusing on strengthening their market position through continuous innovation and expansion of integrated contamination control solutions. They are investing in advanced HVAC systems, energy-efficient filtration technologies, and modular cleanroom designs to improve operational flexibility and cost efficiency. Strategic partnerships with pharmaceutical and biotechnology firms are helping manufacturers expand their customer base and enhance solution customization. Many players are also increasing investment in R&D to develop smart monitoring systems that enable real-time environmental tracking and predictive maintenance.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 By regional

- 2.2.2 By Type

- 2.2.3 By Airflow

- 2.2.4 By ISO Classification

- 2.2.5 By End User

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Pharmaceutical & biotechnology expansion

- 3.2.1.2 Stringent regulatory requirements

- 3.2.1.3 Growth in personalized medicine

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital investment

- 3.2.2.2 Complex maintenance requirements

- 3.2.3 Opportunities

- 3.2.3.1 Modular cleanroom solutions

- 3.2.3.2 Smart monitoring systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 ISO 14644 Standards (Global Classification)

- 3.4.2 cGMP Requirements (FDA/EMA)

- 3.4.3 21 CFR Part 117 (Food Processing Cleanrooms)

- 3.5 Reimbursement scenario

- 3.6 Pricing analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium/Value/Cost-plus) (Driven by Primary Research)

- 3.6.3 Construction Cost Benchmarks by Cleanroom Type

- 3.7 Technology landscape

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Trade Data Analysis (Driven by paid data sources)

- 3.11.1 Import & Export Volume & Value Trends (Driven by Primary Research)

- 3.11.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-Driven Disruption of Existing Business Models

- 3.12.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.12.3 Risks, Limitations & Regulatory Considerations

- 3.12.4 Ecosystem Lock-In Effects: Samsung Galaxy vs Apple Ecosystem Analysis

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Cleanroom Capacity by Region & Key Producer (Driven by Primary Research)

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Consumable

- 5.2.1 Gloves

- 5.2.2 Apparel

- 5.2.3 Wipes

- 5.2.4 Vacuum systems

- 5.2.5 Other consumables

- 5.3 Equipment

- 5.3.1 HVAC systems

- 5.3.2 Cleanroom air filters

- 5.3.3 Laminar air flow cabinet

- 5.3.4 Air diffusers and showers

- 5.3.5 Pass through

- 5.3.6 Other equipment

- 5.4 Structure

- 5.4.1 Conventional cleanrooms

- 5.4.2 Modular cleanrooms

- 5.4.2.1 Hardwall

- 5.4.2.2 Softwall

- 5.4.2.3 Hybrid

Chapter 6 Market Estimates and Forecast, By Airflow Type, 2022 - 2035(USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Unidirectional Airflow (Laminar Flow)

- 6.3 Non-Unidirectional Airflow (Turbulent Flow)

Chapter 7 Market Estimates and Forecast, By ISO Classification, 2022 - 2035(USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 ISO Class 1-4 (Ultra-Clean)

- 7.3 ISO Class 5-6 (Aseptic Processing)

- 7.4 ISO Class 7-8 (General Manufacturing)

- 7.5 ISO Class 9 (Light Assembly)

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035(USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Pharmaceutical industry

- 8.3 Biotechnology industry

- 8.4 Medical device industry

- 8.5 Hospitals & clinics

- 8.6 Other

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Poland

- 9.3.7 Sweden

- 9.3.8 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Indonesia

- 9.4.7 Philippines

- 9.4.8 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Columbia

- 9.5.5 Chile

- 9.5.6 Peru

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Turkey

- 9.6.5 Iran

- 9.6.6 Israel

Chapter 10 Company Profiles

- 10.1 Top Global Players

- 10.1.1 Exyte GmbH

- 10.1.2 DuPont

- 10.1.3 Illinois Tool Works (ITW)

- 10.1.4 Ansell Ltd.

- 10.1.5 Terra Universal, Inc.

- 10.1.6 Azbil Telstar

- 10.1.7 KCC Corporation

- 10.2 Regional Champions

- 10.2.1 ABN Cleanroom Technology

- 10.2.2 Ardmac

- 10.2.3 Clean Air Products

- 10.2.4 Labconco Corporation

- 10.2.5 Airex Filter Corporation

- 10.2.6 Kleanlabs

- 10.3 Emerging & Specialized Players

- 10.3.1 ICLEAN Technologies

- 10.3.2 Nicomac Taikisha Clean Rooms

- 10.3.3 Kleanlabs

無塵室技術市場:按交付方式、建造類型、技術、應用和最終用戶產業分類-2026-2032年全球市場預測

無塵室技術市場:按交付方式、建造類型、技術、應用和最終用戶產業分類-2026-2032年全球市場預測 潔淨室技術市場:按類型、產品類型、最終用戶和地區分類通風櫃監視器市場:按類型、安裝類型、技術、應用、最終用戶和銷售管道分類 - 2026-2032年全球預測

潔淨室技術市場:按類型、產品類型、最終用戶和地區分類通風櫃監視器市場:按類型、安裝類型、技術、應用、最終用戶和銷售管道分類 - 2026-2032年全球預測 無塵室技術市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、設備及最終用戶分類

無塵室技術市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、設備及最終用戶分類 全球無塵室技術市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球無塵室技術市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 無塵室技術市場規模、佔有率及成長分析(按產品、類型、最終用戶和地區分類)-2026-2033年產業預測

無塵室技術市場規模、佔有率及成長分析(按產品、類型、最終用戶和地區分類)-2026-2033年產業預測 2025年無塵室技術全球市場報告

2025年無塵室技術全球市場報告 無塵室技術市場,規模,佔有率,趨勢,產業分析報告:各產品類型,各最終用途,各地區,2025年~2034年的市場預測

無塵室技術市場,規模,佔有率,趨勢,產業分析報告:各產品類型,各最終用途,各地區,2025年~2034年的市場預測 全球無塵室技術市場:按設備和耗材、類型(標準、模組化、移動式)、最終用戶和地區預測到 2032 年

全球無塵室技術市場:按設備和耗材、類型(標準、模組化、移動式)、最終用戶和地區預測到 2032 年 通風櫃監控市場,按產品類型、移動性、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

通風櫃監控市場,按產品類型、移動性、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測