|

市場調查報告書

商品編碼

2038763

切削刀具市場商機、成長要素、產業趨勢分析及2026-2035年預測。Cutting Tool Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

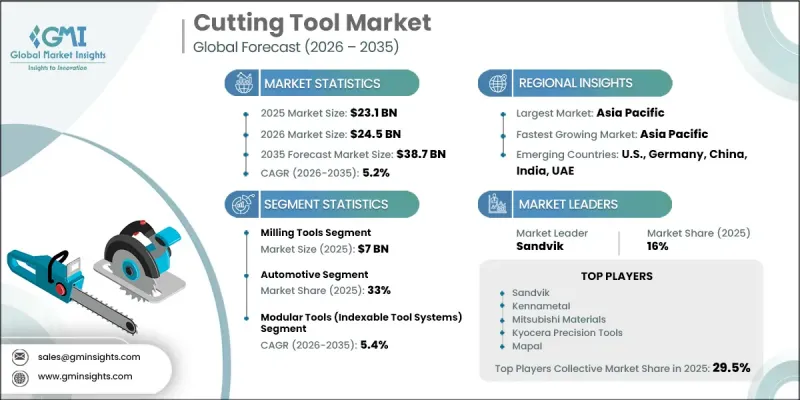

2025年全球切削刀具市場價值為231億美元,預計到2035年將以5.2%的複合年成長率成長至387億美元。

該市場正經歷顯著成長,主要得益於製造流程的進步。隨著自動化和工業4.0技術的進步,對能夠生產無缺陷零件的精密刀具的需求日益成長。汽車、航太和電子等產業尤其受益於這種高精度。此外,朝向更輕更強材料的轉變,例如複合材料和高強度合金,也需要能夠加工這些難加工材料的更先進的切削刀具。另一個主要驅動力是持續的基礎設施建設熱潮,尤其是在快速發展的經濟體中,這增加了對適用於大型機械和現場設備的刀具的需求。此外,對最佳化原料利用和最大限度減少廢棄物的重視,也促使製造商不斷追求更耐用、更經濟高效的切削刀具。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 231億美元 |

| 預測金額 | 387億美元 |

| 複合年成長率 | 5.2% |

此外,在切削刀具產業,隨著企業日益重視永續性並將其視為績效評估的重要因素,環保生產方式的推廣力度也不斷增加。製造商在生產的各個環節都推行環保措施,從原料採購到提高生產過程中的能源效率,無一例外。切削刀具塗層和材料的進步延長了刀具壽命,減少了廢棄物,並提高了切削效率。此外,切削刀具的回收和再利用也變得越來越重要,從而減輕了整體環境負擔。許多公司也致力於減少有害物質的排放,並盡可能減少生產過程中有害化學品的使用。

預計到2025年,汽車產業將佔據33%的市場佔有率,並在2026年至2035年間以5.4%的複合年成長率成長。對省油車日益成長的需求預計將推動切削刀具市場這一細分領域的強勁成長。此外,向電動車(EV)生產的持續轉型也推動了對先進切削刀具的需求成長,以支持更精確、更有效率的汽車製造流程。

預計到2025年,銑削刀具市場規模將達70億美元。這一快速成長歸功於銑削刀具在各行業的廣泛應用。銑削刀具是加工高精度、複雜形狀的關鍵工具,廣泛應用於汽車、航太和電子產業。隨著產品設計對更輕、更耐用零件的需求不斷成長,銑削刀具對先進材料加工能力的提升也推動了市場需求。此外,多功能設計和塗層技術的改進等創新也透過延長刀具壽命和降低營運成本,促進了該領域的成長。

預計2025年,美國切削刀具市場規模將達35億美元。美國製造業涵蓋眾多產業,是該市場的主要驅動力。汽車和航太產業對符合嚴格品質標準的高精度刀具的需求不斷成長。此外,機器人、感測器和雲端分析等技術在製造環境中的應用,透過提高營運效率,進一步加速了市場成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(2025 年)(基於初步調查)

- 對過去價格趨勢的分析

- 按工具類型分類的定價策略(高階/經濟型/成本加成)

- 價格波動與產品類型和技術世代有關

- 消費者價格敏感度分析

- 監理情勢

- 環境法規:REACH(歐盟)、衝突礦產合規性

- 品質與安全標準:ISO 9001、ISO 16084(切削刀具標準)

- 影響工具出口的貿易政策和關稅

- 區域法規結構

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧正在改變傳統的經營模式。

- 按客戶群分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 人工智慧驅動的智慧家庭生態系統的整合

- 貿易資料分析(基於付費資料庫)(HS編碼:8207)

- 進出口量及進口額趨勢

- 主要貿易走廊及關稅的影響

- 分銷基礎設施和通路滲透狀況(基於初步調查)

- 按地區和分銷管道(現代分銷與傳統分銷)分類的分銷網路覆蓋範圍

- 缺乏最後一公里基礎設施和分銷管道的變化

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依工具類型分類,2022-2035年

- 鑽井工具

- 麻花鑽

- 槍鑽

- 索引式鑽頭

- 硬質合金鑽頭

- 切削刀具

- 端銑刀

- 平面銑刀

- 硬質合金磨機

- 車削工具

- 插入式車削切屑

- 保齡球酒吧

- 開槽刀具和切削刀具

- 螺紋加工工具

- 跑步機

- 輕敲

- 螺紋成型工具

- 鉸刀

- 機用鉸刀

- 手鉸刀

- 可調式鉸刀

- 沉孔和去毛邊工具

- 沉頭鑽

- 去毛邊工具

- 倒角銑床

- 深孔鑽井工具

第6章 市場估算與預測:依切割材料分類,2022-2035年

- 硬質合金刀具

- 多晶鑽石(PCD)工具

- 多晶立方氮化硼(PCBN)工具

- 高速鋼(HSS)刀具

- 金屬陶瓷工具

- 陶瓷工具

第7章 市場估計與預測:依工具配置分類,2022-2035年

- 模組化工具(索引工具系統)

- 一體式工具(實心/硬焊工具)

第8章 市場估算與預測:依最終用途產業分類,2022-2035年

- 車

- 航太/國防

- 建造

- 家用電子電器

- 能源

- 工具和模具製造

- 其他(船舶、農業等)

第9章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 全球主要公司

- Iscar(IMC Group)

- Kennametal

- Kyocera Precision Tools

- Mitsubishi Materials

- Sandvik Coromant

- Seco Tools

- Sumitomo Electric Hardmetal

- 按地區分類的主要公司

- Ingersoll Cutting Tools

- Korloy

- Mapal

- OSG Corporation

- Walter

- Widia

- Zhuzhou Cemented Carbide

- Emerging and Specialized Players

- Allied Machine &Engineering

- BIG Kaiser Precision

- Carmex Precision Tools

- Fullerton Tool

- Greenleaf Corporation

- Harvey Tool

- Monster Tool Company

The Global Cutting Tool Market was valued at USD 23.1 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 38.7 billion by 2035.

This market is experiencing significant growth, driven largely by advancements in manufacturing methods. With the rise of automation and Industry 4.0 practices, there is an increasing demand for precision tools that produce defect-free parts. Industries like automotive, aerospace, and electronics particularly benefit from such accuracy. Additionally, the shift toward using lighter and stronger materials, including composites and high strength alloys, necessitates more advanced cutting tools that can handle these tough materials. Another key driver is the ongoing infrastructure boom, especially in rapidly developing economies, which raises the need for tools suitable for large machines and site equipment. Along with this, the focus on optimizing raw material use and minimizing waste continues to push manufacturers toward more durable, cost-effective cutting tools.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $23.1 Billion |

| Forecast Value | $38.7 Billion |

| CAGR | 5.2% |

Furthermore, the drive for greener production methods is accelerating within the cutting tools industry, as companies increasingly prioritize sustainability alongside performance. Manufacturers are adopting eco-friendly practices at every stage, from sourcing raw materials to improving energy efficiency during the manufacturing process. Advances in cutting tool coatings and materials are enabling longer tool lifespans and reduced waste, while also enhancing cutting efficiency. Additionally, there is a growing emphasis on recycling and reusing cutting tools, reducing the overall environmental footprint. Many companies are also focusing on reducing hazardous emissions and minimizing the use of harmful chemicals during the production process.

In 2025, the automotive segment held a 33% share and is projected to grow at a CAGR of 5.4% from 2026 to 2035. Strong growth in this segment is expected within the cutting tools market due to rising demand for fuel-efficient vehicles. The ongoing shift toward electric vehicle production is also increasing the requirement for advanced cutting tools to support more precise and efficient automotive manufacturing processes.

The milling tools segment accounted for USD 7 billion in 2025. The rapid expansion of this segment can be attributed to the wide range of tasks milling tools can handle in multiple industries. These tools are essential for producing complex profiles with high precision, and they are commonly used in automotive, aerospace, and electronics. As product designs demand lighter yet more durable parts, milling tools are gaining popularity due to their ability to cut through advanced materials. Innovations, such as multi-purpose designs and improved coatings, have also contributed to the segment's growth by extending tool life and reducing operational costs.

United States Cutting Tool Market was valued at USD 3.5 billion in 2025. The U.S. manufacturing sector, which spans a wide range of industries, is a key factor driving this dominance. The automotive and aerospace sectors fuel the demand for highly accurate tools that meet stringent quality standards. Additionally, the integration of robotics, sensors, and cloud analytics in manufacturing further boosts market growth by enhancing operational efficiency.

Key companies in the Global Cutting Tool Industry include Ceratizit S.A., Cougar Cutting Tools, Emuge Corporation, Greenleaf Corporation, Ingersoll Cutting Tools, Iscar Ltd., Kennametal Inc., Mapal Inc., Mitsubishi Materials Corporation, Mohawk Special Cutting Tools, OSG Corporation, Sandvik Coromant, Seco Tools AB, Tungaloy Corporation, and Walter Technologies. In response to the increasing demand for cutting-edge products, companies in the cutting tool market are focusing on technological advancements to enhance their market position. Leading players are investing heavily in research and development to improve the performance of their tools and increase their lifespan. They are also actively exploring sustainable manufacturing techniques to meet environmental regulations and consumer demands for greener products. Additionally, strategic partnerships, mergers, and acquisitions are being utilized to expand product offerings and strengthen supply chains. Companies are also incorporating digital tools, such as smart sensors and IoT-enabled devices, to enhance precision and operational efficiency in manufacturing.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Tool Type

- 2.2.3 Cutting Material

- 2.2.4 Tool Configuration

- 2.2.5 End Use Industry

- 2.2.6 Distribution Channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2025 (driven by primary research)

- 3.6.1 Historical price trend analysis

- 3.6.2 Pricing strategy by tool type (premium / value / cost-plus)

- 3.6.3 Price variation by product type & technology generation

- 3.6.4 Consumer price sensitivity analysis

- 3.7 Regulatory landscape

- 3.7.1 Environmental regulations: REACH (EU), conflict minerals compliance

- 3.7.2 Quality and safety standards: ISO 9001, ISO 16084 (cutting tool standards)

- 3.7.3 Trade policies and tariffs impacting tool exports

- 3.7.4 Regional regulatory frameworks

- 3.8 Impact of AI & generative AI on the market

- 3.8.1 AI-driven disruption of traditional business models

- 3.8.2 GenAI use cases & adoption roadmap by customer segment

- 3.8.3 Risks, limitations & regulatory considerations

- 3.8.4 AI-enabled smart home ecosystem integration

- 3.9 Trade data analysis (driven by paid database) (HS Code: 8207)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.10.1 Channel coverage by region & format (modern vs. traditional trade)

- 3.10.2 Last-mile infrastructure gaps & emerging channel shifts

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Tool Type, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Drilling tools

- 5.2.1 Twist drills

- 5.2.2 Gun drills

- 5.2.3 Indexable drills

- 5.2.4 Solid carbide drills

- 5.3 Milling tools

- 5.3.1 End mills

- 5.3.2 Face mills

- 5.3.3 Solid carbide mills

- 5.4 Turning tools

- 5.4.1 Indexable turning inserts

- 5.4.2 Boring bars

- 5.4.3 Grooving and parting tools

- 5.5 Threading tools

- 5.5.1 Thread mills

- 5.5.2 Taps

- 5.5.3 Thread forming tools

- 5.6 Reaming tools

- 5.6.1 Machine reamers

- 5.6.2 Hand reamers

- 5.6.3 Adjustable reamers

- 5.7 Countersinking and deburring tools

- 5.7.1 Countersinks

- 5.7.2 Deburring tools

- 5.7.3 Chamfer mills

- 5.8 Deep-hole drilling tools

Chapter 6 Market Estimates & Forecast, By Cutting Material, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Solid carbide tools

- 6.3 Polycrystalline diamond (PCD) tools

- 6.4 Polycrystalline cubic boron nitride (PCBN) tools

- 6.5 High-speed steel (HSS) tools

- 6.6 Cermet tools

- 6.7 Ceramic tools

Chapter 7 Market Estimates & Forecast, By Tool Configuration, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Modular tools (indexable tool systems)

- 7.3 Monolithic tools (solid/brazed tools)

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Aerospace & defense

- 8.4 Construction

- 8.5 Consumer electronics

- 8.6 Energy

- 8.7 Tool and mold making

- 8.8 Others (marine, agriculture etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Top Global Players

- 11.1.1 Iscar (IMC Group)

- 11.1.2 Kennametal

- 11.1.3 Kyocera Precision Tools

- 11.1.4 Mitsubishi Materials

- 11.1.5 Sandvik Coromant

- 11.1.6 Seco Tools

- 11.1.7 Sumitomo Electric Hardmetal

- 11.2 Regional Key Players

- 11.2.1 Ingersoll Cutting Tools

- 11.2.2 Korloy

- 11.2.3 Mapal

- 11.2.4 OSG Corporation

- 11.2.5 Walter

- 11.2.6 Widia

- 11.2.7 Zhuzhou Cemented Carbide

- 11.3 Emerging and Specialized Players

- 11.3.1 Allied Machine & Engineering

- 11.3.2 BIG Kaiser Precision

- 11.3.3 Carmex Precision Tools

- 11.3.4 Fullerton Tool

- 11.3.5 Greenleaf Corporation

- 11.3.6 Harvey Tool

- 11.3.7 Monster Tool Company

徑向螺紋滾壓頭市場預測至 2034 年—按類型、材質、銷售管道、應用和地區進行全球分析。

徑向螺紋滾壓頭市場預測至 2034 年—按類型、材質、銷售管道、應用和地區進行全球分析。 高速鋼切削刀具市場報告:按類型、技術、終端用戶產業和地區分類(2026-2034 年)

高速鋼切削刀具市場報告:按類型、技術、終端用戶產業和地區分類(2026-2034 年) 切割工具的全球市場:終端用戶,競爭企業 - 分析與預測(2024年~2030年)- 全4卷套組

切割工具的全球市場:終端用戶,競爭企業 - 分析與預測(2024年~2030年)- 全4卷套組 單晶鑽石切割工具市場:按工具類型、材料、應用、終端用戶產業和銷售管道分類-2026-2032年全球市場預測齒輪切削刀具市場:2026-2032年全球市場預測(依齒輪切削方法、工具機類型、應用、終端用戶產業、材料及銷售管道)PCD切削刀具市場:依刀具類型、加工製程、基材、粘合劑類型、產品等級及最終用途產業分類-2026-2032年全球預測基於數控技術的鑽石切割刀具市場:按刀具類型、鑽石類型、工具機類型、應用和最終用戶產業分類-2026-2032年全球預測多晶鑽石市場:依產品類型、應用、終端用戶產業和銷售管道-2026-2032年全球預測鑽石多線切割機市場:按機器類型、材質、銷售管道、終端用戶產業和應用程式分類-2026-2032年全球預測切削刀具回收市場:依服務類型、刀具類型、材料、機器類型、最終用戶和銷售管道,全球預測,2026-2032年

單晶鑽石切割工具市場:按工具類型、材料、應用、終端用戶產業和銷售管道分類-2026-2032年全球市場預測齒輪切削刀具市場:2026-2032年全球市場預測(依齒輪切削方法、工具機類型、應用、終端用戶產業、材料及銷售管道)PCD切削刀具市場:依刀具類型、加工製程、基材、粘合劑類型、產品等級及最終用途產業分類-2026-2032年全球預測基於數控技術的鑽石切割刀具市場:按刀具類型、鑽石類型、工具機類型、應用和最終用戶產業分類-2026-2032年全球預測多晶鑽石市場:依產品類型、應用、終端用戶產業和銷售管道-2026-2032年全球預測鑽石多線切割機市場:按機器類型、材質、銷售管道、終端用戶產業和應用程式分類-2026-2032年全球預測切削刀具回收市場:依服務類型、刀具類型、材料、機器類型、最終用戶和銷售管道,全球預測,2026-2032年