|

市場調查報告書

商品編碼

2038739

罐裝水果市場:商機、成長要素、產業趨勢分析及2026-2035年預測Canned Fruits Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

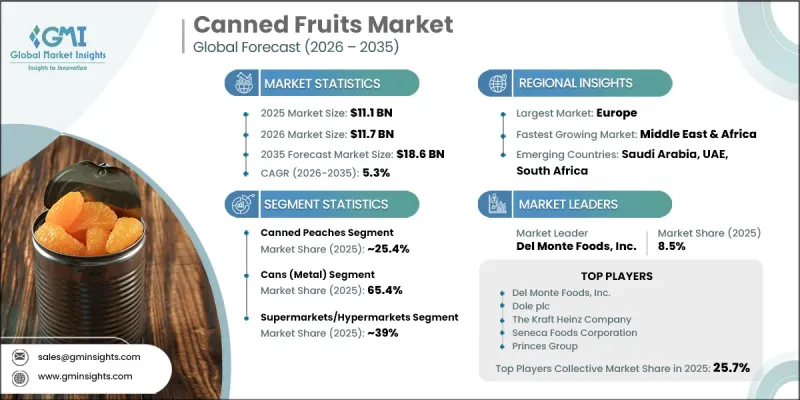

預計到 2025 年,全球罐裝水果市場價值將達到 111 億美元,並預計以 5.3% 的複合年成長率成長,到 2035 年達到 186 億美元。

市場成長的驅動力在於消費者對便利、保存期限長且營養豐富的水果類食品的偏好日益成長,這不僅體現在家庭消費中,也體現在餐飲服務業。都市化和快節奏的生活方式推動了人們對「即食」水果產品的需求,這類產品只需極少的烹飪準備即可提供必需的營養。罐裝水果是家庭和商用廚房中用途廣泛的食材,可用於製作甜點、烘焙食品、沙拉和飲料等。此外,先進的加工技術能夠更好地保留水果中的必需維生素和礦物質,使其越來越受到注重健康的消費者的青睞。產品類型水果種類繁多,能夠滿足不同的口味偏好,並彌補季節性供應缺口。其價格實惠且全年供應充足,進一步鞏固了其市場地位,尤其是在生鮮食品供應有限的地區。更長的保存期限也有助於減少食物廢棄物,從而提升了其價值提案。除了零售網路的穩定擴張外,有組織的食品分銷管道和線上食品雜貨平台的日益普及也進一步加速了全球市場產品的供應和消費。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 111億美元 |

| 預測金額 | 186億美元 |

| 複合年成長率 | 5.3% |

預計到2025年,罐裝桃子市場佔有率將達到25.4%,並在2035年之前以5.5%的複合年成長率成長。由於其較高的消費者認知度、良好的口感以及從直接食用到烹飪的多功能性,罐裝桃子持續推動著罐裝水果市場的發展。罐裝桃子是家庭食品儲藏室和餐飲服務業的必備品,常用於甜點、烘焙點心和零食。其穩定的風味和口感,以及在各種菜餚中的便利性,支撐著持續的需求。此外,較高的品牌知名度和已形成的消費習慣也促進了該細分市場的成長,從而提高了消費者的重複購買率。商用廚房和加工食品製造業對「即用型」水果配料的需求不斷成長,也持續推動該細分市場的成長。諸如降低糖漿含量、減少糖分以及推出不含防腐劑的產品等創新舉措,進一步提升了消費者的興趣,並促進了注重健康的消費者群體對罐裝桃子產品的廣泛使用。

預計到2025年,金屬罐市佔率將達到65.4%,並在2026年至2035年間以5%的複合年成長率成長。包裝創新和永續性考量是推動該細分市場發展的主要因素。金屬罐因其耐用性、較長的保存期限以及能夠長時間保持產品新鮮度而成為首選包裝形式。其輕巧的結構和高抗污染性使其既適用於散裝儲存,也適用於零售分銷。此外,這種包裝形式在大規模食品供應鏈中具有顯著優勢,能夠實現高效運輸並防止產品變質。人們對可回收和環保包裝解決方案的日益關注進一步促進了金屬罐的普及。製造商正日益致力於改進塗層技術和減少材料用量,以在維持產品品質的同時提升永續性。

預計到2025年,北美罐裝水果市佔率將達到24.5%。該地區消費者對營養食品的選擇意識日益增強,並偏好有機和健康加工食品。忙碌的都市區居民對便捷即食水果產品的需求特別旺盛。罐裝水果因其便攜性、保存期限長以及在家庭烹飪和餐飲服務業中的易用性而日益受到歡迎。超級市場和大賣場是零售分銷的強大支撐,而線上食品銷售平台則因數位化進步和消費者對便利性消費的日益重視而蓬勃發展。永續性趨勢也影響市場成長,製造商紛紛採用可回收材料和環保包裝。持續的產品創新、口味多樣化以及潔淨標示策略的推廣,進一步推動了全部區域市場的擴張。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 罐裝蘋果

- 罐裝杏

- 罐裝漿果

- 罐裝櫻桃

- 罐裝柑橘類水果

- 罐裝葡萄

- 罐裝什錦水果

- 罐裝桃子

- 罐裝梨

- 罐裝鳳梨

- 罐裝李子

- 其他

第6章 市場估價與預測:依包裝類型分類,2022-2035年

- 罐(金屬)

- 玻璃瓶

- 其他

第7章 市場估價與預測:依通路分類,2022-2035年

- 超級市場/大賣場

- 便利商店

- 線上零售

- 專賣店

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- A. Clouet &Co.(KL)Sdn. Bhd.

- CHB Group

- Conserve Italia

- Del Monte Foods, Inc.

- Dole plc

- Golden Circle

- Goya Foods, Inc.

- Kangfa Food Co., Ltd.

- Princes Group

- RFG Foods

- Rhodes Food Group

- Seneca Foods Corporation

- The Kraft Heinz Company

The Global Canned Fruits Market was valued at USD 11.1 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 18.6 billion by 2035.

Market growth is supported by rising consumer preference for convenient, shelf-stable, and nutritious fruit-based food options across households and foodservice industries. Increasing urbanization and fast-paced lifestyles are encouraging demand for ready-to-eat fruit products that require minimal preparation while still offering essential nutrients. Canned fruits are widely used across desserts, baking applications, salads, and beverages, making them a versatile ingredient in both domestic and commercial kitchens. They retain essential vitamins and minerals through modern processing methods, which enhances their appeal among health-conscious consumers. The product category offers a wide assortment of fruit varieties that cater to diverse taste preferences and seasonal availability gaps. In addition, affordability and year-round accessibility continue to strengthen their market position, particularly in regions with limited access to fresh produce. Longer shelf life also helps reduce food waste, further improving their value proposition. The steady expansion of retail networks, combined with increasing penetration of organized food distribution channels and online grocery platforms, is further accelerating product availability and consumption across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.1 Billion |

| Forecast Value | $18.6 Billion |

| CAGR | 5.3% |

The canned peaches segment accounted for a 25.4% share in 2025 and is projected to grow at a CAGR of 5.5% through 2035. This segment continues to lead the canned fruits market due to its strong consumer familiarity, pleasant taste profile, and wide usability across both direct consumption and culinary applications. Canned peaches are frequently used in desserts, baking recipes, and snack preparations, making them a staple in household pantries as well as foodservice operations. Their consistent flavor, texture retention, and ease of incorporation into multiple dishes support sustained demand. The segment also benefits from strong brand recognition and established consumption habits, which contribute to repeat purchases. Additionally, increasing demand for ready-to-use fruit ingredients in commercial kitchens and packaged food production continues to reinforce segment growth. Product innovation in syrup levels, reduced sugar formulations, and preservative-free options is further enhancing consumer appeal and expanding usage across health-conscious demographics.

The metal cans segment held a share of 65.4% in 2025 and is anticipated to grow at a CAGR of 5% between 2026 and 2035. Packaging innovation and sustainability considerations are key drivers shaping this segment. Metal cans remain the preferred packaging format due to their durability, long shelf life protection, and ability to preserve product freshness over extended periods. Their lightweight structure, combined with high resistance to contamination, makes them suitable for both bulk storage and retail distribution. The packaging type also supports efficient transportation and reduces product spoilage, which is a critical advantage in large-scale food supply chains. Growing emphasis on recyclable and environmentally responsible packaging solutions is further strengthening the adoption of metal cans. Manufacturers are increasingly focusing on improving coating technologies and reducing material usage to enhance sustainability performance while maintaining product integrity.

North America Canned Fruits Market accounted for a 24.5% share in 2025. The region is characterized by strong consumer awareness regarding nutritional food choices and a growing preference for organic and health-oriented packaged foods. Demand for convenient, ready-to-eat fruit products is rising, particularly among urban populations with fast-paced lifestyles. Canned fruits are increasingly being preferred for their portability, long shelf life, and ease of use in home cooking and foodservice applications. Retail distribution is strongly supported by supermarkets and hypermarkets, while online grocery platforms are gaining momentum due to rising digital adoption and convenience-driven shopping behavior. Sustainability trends are also influencing market growth, with manufacturers adopting recyclable materials and eco-friendly packaging formats. Continuous product innovation, flavor diversification, and clean-label positioning are further strengthening market expansion across the region.

Major players operating in the Global Canned Fruits Industry include CHB Group, A. Clouet & Co. (KL) Sdn. Bhd., Conserve Italia, Dole plc, Del Monte Foods, Inc., Goya Foods, Inc., Golden Circle, Kangfa Food Co., Ltd., Princes Group, RFG Foods, Rhodes Food Group, Seneca Foods Corporation, and The Kraft Heinz Company. Companies in the Canned Fruits Market are focusing on expanding product portfolios through diversified fruit offerings and healthier formulations with reduced sugar and preservative content. They are strengthening supply chain efficiency by investing in advanced processing technologies and automation to ensure consistent quality and longer shelf life. Strategic partnerships with retail chains and foodservice distributors are being used to improve market penetration. Firms are also investing heavily in sustainable packaging solutions, particularly recyclable and lightweight metal cans, to align with environmental expectations. Digital marketing and e-commerce expansion are playing a key role in enhancing brand visibility and consumer reach. Additionally, companies are introducing premium and organic product lines to target health-conscious consumers, while innovation in flavor combinations and packaging formats is helping to differentiate offerings in a competitive market landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Packaging type

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Canned apples

- 5.3 Canned apricots

- 5.4 Canned berries

- 5.5 Canned cherries

- 5.6 Canned citrus fruits

- 5.7 Canned grapes

- 5.8 Canned mixed fruits

- 5.9 Canned peaches

- 5.10 Canned pears

- 5.11 Canned pineapples

- 5.12 Canned plums

- 5.13 Others

Chapter 6 Market Estimates and Forecast, By Packaging Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cans (metal)

- 6.3 Glass jars

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Supermarkets/hypermarkets

- 7.3 Convenience stores

- 7.4 Online retail

- 7.5 Specialty stores

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 A. Clouet & Co. (KL) Sdn. Bhd.

- 9.2 CHB Group

- 9.3 Conserve Italia

- 9.4 Del Monte Foods, Inc.

- 9.5 Dole plc

- 9.6 Golden Circle

- 9.7 Goya Foods, Inc.

- 9.8 Kangfa Food Co., Ltd.

- 9.9 Princes Group

- 9.10 RFG Foods

- 9.11 Rhodes Food Group

- 9.12 Seneca Foods Corporation

- 9.13 The Kraft Heinz Company