|

市場調查報告書

商品編碼

2038688

皮膚科影像設備市場:商機、成長要素、產業趨勢分析及 2026-2035 年預測。Dermatology Imaging Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

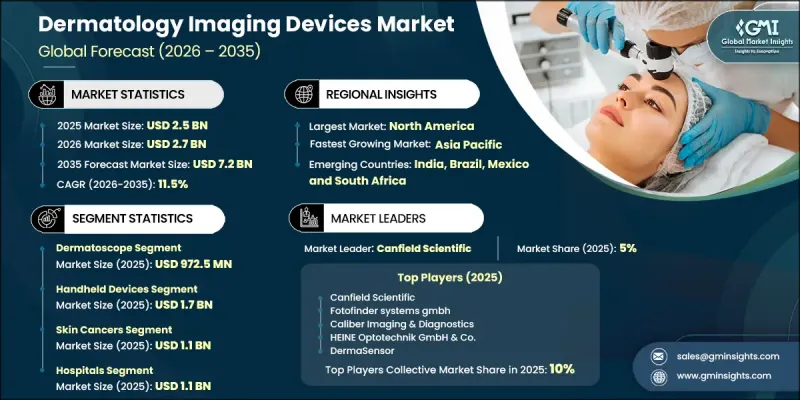

2025 年全球皮膚病影像設備市場價值 25 億美元,預計到 2035 年將達到 72 億美元,年複合成長率為 11.5%。

市場成長的促進因素包括人們對皮膚健康的日益關注、對皮膚疾病早期精準診斷需求的成長以及影像技術的不斷進步。全球皮膚癌病例的不斷增加進一步加劇了對先進診斷解決方案的需求,並推動了皮膚成像系統在醫療機構中的應用。黑色素瘤和非黑色素瘤皮膚癌日益加重的臨床負擔促使醫療專業人員採用更精準、更早期的診斷工具。同時,皮膚疾病仍然是全球最普遍的健康問題之一,影響各個年齡層的患者,並對其生理、心理和社會造成顯著影響。日益加重的疾病負擔正在加速對高解析度、人工智慧賦能的非侵入性影像解決方案的需求,這些解決方案有助於早期發現和有效管理疾病。此外,向非侵入性診斷程序的轉變以及先進影像系統普及程度的提高,也進一步促進了已開發國家和新興國家醫療系統市場的發展。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 25億美元 |

| 預計金額 | 72億美元 |

| 複合年成長率 | 11.5% |

預計到2025年,皮膚鏡市場規模將達到9.725億美元。由於其能夠清晰地顯示皮膚深層結構,皮膚鏡仍然是皮膚影像學領域應用最廣泛的設備之一。它被廣泛用於評估色素沉著模式、血管結構以及傳統檢查方法難以清晰觀察到的皮膚病變。技術的進步顯著提升了皮膚鏡的性能,最新的設備融合了偏振光照明、先進的放大倍率和數位影像處理功能,能夠更清晰、更深入地觀察皮膚層。

預計到2025年,手持式成像設備市場規模將達17億美元。該細分市場憑藉其便攜性、易用性和適用於臨床快速皮膚檢查的優勢,佔據市場主導地位。手持式影像系統廣泛應用於專科醫療和一般醫療機構,用於評估痣、皮疹和早期皮膚異常。小型化和方便用戶使用型設備的日益普及也推動了其應用範圍的擴大,使其不再局限於皮膚科診所。此外,針對基層醫療機構的新型影像解決方案正在開發中,使醫護人員能夠快速識別疑似皮膚疾病,並根據需要將患者轉診進行進一步檢查。

預計到2025年,美國皮膚科影像設備市場規模將達到8.152億美元,主要得益於強勁的醫療費用支出、先進醫療技術的高普及率以及完善的皮膚科醫療基礎設施。此外,在數位平台和健康教育措施的推動下,大眾對皮膚健康和預防性篩檢的意識不斷提高,進一步增強了全美對先進皮膚科影像解決方案的需求。

目錄

第1章:調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策和資料完整性計劃

- 資訊來源一致性協議

- GMI人工智慧政策和資料完整性計劃

- 調查過程和可靠性評分

- 調查過程的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 每種方法中基準年的計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 關於調查透明度的補充信息

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 提高對皮膚疾病的認知和早期檢測

- 皮膚影像技術的不斷進步

- 全球皮膚癌發生率正在上升。

- 皮膚病學領域對非侵入性診斷技術的興趣日益濃厚。

- 產業潛在風險與挑戰

- 設備高成本

- 皮膚科影像診斷方案缺乏標準化

- 市場機遇

- 對人工智慧驅動的皮膚癌篩檢工具的需求日益成長

- 新興市場醫療基礎設施不斷改善,蘊藏著巨大的成長潛力。

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 歐洲

- 亞太地區

- 技術趨勢(基於初步調查)

- 目前技術

- 數位工作流程整合

- 人工智慧驅動的病灶分析

- 多模態影像平台

- 基於雲端的影像管理系統

- 新興技術

- 人工智慧的應用

- 攜帶式和智慧型手機相容的成像設備

- 3D皮膚表面映射和可視化

- 光學同調斷層掃描(OCT)的整合

- 目前技術

- 未來市場趨勢(基於初步研究)

- 還款方案(基於初步調查)

- 專利分析(基於初步研究)

- 人工智慧和生成式人工智慧對市場的影響(基於初步研究)

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依治療方式分類,2022-2035年

- 皮膚鏡

- 數位照片

- 光學同調斷層掃描(OCT)

- 高頻超音波

- 反射式共聚焦顯微鏡(RCM)

- 其他方式

第6章 市場估算與預測:依設備類型分類,2022-2035年

- 手持裝置

- 桌上型/寬探針設備

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 皮膚癌

- 發炎性皮膚病

- 銀屑病

- 異位性皮膚炎

- 其他發炎性皮膚病

- 整形和重組外科

- 燒傷治療

- 其他用途

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 醫院

- 皮膚病中心

- 專科診所

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 3Derm Systems

- Barco NV

- BOMTECH ELECTRONICS CO.

- Caliber Imaging & Diagnostics

- Canfield Scientific

- Clarius Mobile Health

- Cortex Technology ApS

- Courage+Khazaka electronic GmbH

- DeepX Health

- DermaSensor

- Firefly Global

- FotoFinder Systems GmbH

- Fujifilm Holdings Corporation

- HEINE Optotechnik GmbH & Co.

- Illuco Corporation Ltd.

- KIRCHNER & WILHELM GmbH+Co.

- MetaOptima Technology

- Michelson Diagnostics

- Pixience

- Shenzhen Iboolo Optics Co.

The Global Dermatology Imaging Devices Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 11.5% to reach USD 7.2 billion by 2035.

Market growth is driven by rising awareness of skin health, increasing demand for early and accurate diagnosis of dermatological conditions, and continuous advancements in imaging technologies. The global rise in skin cancer cases is further strengthening the need for advanced diagnostic solutions, supporting broader adoption of dermatology imaging systems across healthcare settings. The increasing clinical burden of both melanoma and non-melanoma skin cancers is pushing healthcare providers to adopt more precise and early-stage diagnostic tools. At the same time, dermatological conditions remain among the most widespread health issues globally, affecting patients across all age groups and contributing to significant physical, psychological, and social impacts. This growing disease burden is accelerating demand for high-resolution, AI-enabled, and non-invasive imaging solutions that support early detection and effective disease management. In addition, the shift toward non-invasive diagnostic procedures and improved accessibility of advanced imaging systems is further contributing to market expansion across developed and emerging healthcare systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $7.2 Billion |

| CAGR | 11.5% |

The dermatoscope segment accounted for USD 972.5 million in 2025. This segment remains one of the most widely utilized categories within dermatology imaging due to its ability to provide detailed visualization of subsurface skin structures. It is extensively used for evaluating pigmentation patterns, vascular structures, and skin lesions that cannot be clearly observed through conventional examination methods. Technological improvements have significantly enhanced dermatoscope performance, with modern devices incorporating polarized illumination, advanced magnification, and digital imaging capabilities that enable deeper and clearer visualization of skin layers.

The handheld devices segment generated USD 1.7 billion in 2025. This segment holds a dominant position due to its portability, ease of use, and suitability for rapid skin examinations in clinical settings. Handheld imaging systems are widely used for assessing moles, rashes, and early-stage skin abnormalities in both specialist and general healthcare environments. The growing availability of compact, user-friendly devices is also enabling wider use beyond dermatology clinics. In addition, newer imaging solutions are being developed for use in primary care settings, allowing healthcare professionals to identify suspicious skin conditions quickly and refer patients for further evaluation when necessary.

U.S. Dermatology Imaging Devices Market reached USD 815.2 million in 2025 supported by strong healthcare expenditure, high adoption of advanced medical technologies, and well-established dermatology care infrastructure. Increasing public awareness of skin health and preventive screening, supported by digital platforms and health education initiatives, is further strengthening demand for advanced dermatology imaging solutions across the United States.

Key companies operating in the Global Dermatology Imaging Devices Market include Canfield Scientific, FotoFinder Systems GmbH, Fujifilm Holdings Corporation, Barco NV, DermaSensor, Clarius Mobile Health, MetaOptima Technology, Firefly Global, Caliber Imaging & Diagnostics, DeepX Health, Cortex Technology ApS, 3Derm Systems, HEINE Optotechnik GmbH & Co., Courage+ Khazaka electronic GmbH, Illuco Corporation Ltd., Pixience, BOMTECH ELECTRONICS CO., Michelson Diagnostics, KIRCHNER & WILHELM GmbH + Co., and Shenzhen Iboolo Optics Co. Companies in the Dermatology Imaging Devices Market are focusing on technological innovation, AI integration, and product miniaturization to strengthen their competitive position. Continuous investment in research and development is enabling improvements in image resolution, diagnostic accuracy, and real-time data analysis. Manufacturers are increasingly integrating artificial intelligence and cloud-based platforms to support automated lesion detection and patient data management. Strategic partnerships with healthcare providers and dermatology clinics are helping expand clinical adoption and improve market penetration. Firms are also emphasizing the development of portable and cost-effective devices to increase accessibility across different healthcare settings.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.1.1 Key market trends

- 2.1.2 Modality trends

- 2.1.3 Device Type trends

- 2.1.4 Application trends

- 2.1.5 End use trends

- 2.1.6 Regional trends

- 2.2 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Enhanced awareness and timely identification of dermatological issues

- 3.2.1.2 Continuous advancements in dermatology imaging technologies

- 3.2.1.3 Increasing incidence of skin cancer worldwide

- 3.2.1.4 Growing focus on non-invasive diagnostic techniques in dermatology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices

- 3.2.2.2 Lack of standardization in dermatology imaging protocols

- 3.2.3 Market opportunity

- 3.2.3.1 Rising demand for AI-powered skin cancer screening tools

- 3.2.3.2 Growth potential in emerging markets with improving healthcare infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological landscape (Driven by Primary Research)

- 3.5.1 Current technologies

- 3.5.1.1 Digital workflow integration

- 3.5.1.2 AI-assisted lesion analysis

- 3.5.1.3 Multi-modal imaging platforms

- 3.5.1.4 Cloud-based image management systems

- 3.5.2 Emerging technologies

- 3.5.2.1 Artificial intelligence applications

- 3.5.2.2 Portable and smartphone-compatible imaging devices

- 3.5.2.3 3D skin surface mapping and visualization

- 3.5.2.4 Optical coherence tomography (OCT) integration

- 3.5.1 Current technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Reimbursement scenario (Driven by Primary Research)

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Impact of AI and Generative AI on the market (Driven by Primary Research)

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Modality, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Dermatoscope

- 5.3 Digital photographic imaging

- 5.4 Optical coherence tomography (OCT)

- 5.5 High-frequency ultrasound

- 5.6 Reflectance confocal microscopy (RCM)

- 5.7 Other modalities

Chapter 6 Market Estimates and Forecast, By Device Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Handheld devices

- 6.3 Benchtop/ wide-probe devices

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Skin cancers

- 7.3 Inflammatory dermatoses

- 7.3.1 Skin psoriasis

- 7.3.2 Atopic dermatitis

- 7.3.3 Other inflammatory dermatoses

- 7.4 Plastic and reconstructive surgery

- 7.5 Burn management

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Dermatology centers

- 8.4 Specialty clinics

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3Derm Systems

- 10.2 Barco NV

- 10.3 BOMTECH ELECTRONICS CO.

- 10.4 Caliber Imaging & Diagnostics

- 10.5 Canfield Scientific

- 10.6 Clarius Mobile Health

- 10.7 Cortex Technology ApS

- 10.8 Courage+ Khazaka electronic GmbH

- 10.9 DeepX Health

- 10.10 DermaSensor

- 10.11 Firefly Global

- 10.12 FotoFinder Systems GmbH

- 10.13 Fujifilm Holdings Corporation

- 10.14 HEINE Optotechnik GmbH & Co.

- 10.15 Illuco Corporation Ltd.

- 10.16 KIRCHNER & WILHELM GmbH + Co.

- 10.17 MetaOptima Technology

- 10.18 Michelson Diagnostics

- 10.19 Pixience

- 10.20 Shenzhen Iboolo Optics Co.

皮膚影像設備市場預測至2034年-按產品、模式、技術、應用、最終用戶和地區分類的全球分析

皮膚影像設備市場預測至2034年-按產品、模式、技術、應用、最終用戶和地區分類的全球分析 2026年全球皮膚病診斷影像設備市場報告

2026年全球皮膚病診斷影像設備市場報告 2026-2034年全球皮膚影像設備市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球皮膚影像設備市場規模、佔有率、趨勢和成長分析報告 診斷皮膚病學影像設備市場—全球產業規模、佔有率、趨勢、機會和預測(按模式、按應用、按最終用戶、按地區和競爭細分,2020-2030 年)

診斷皮膚病學影像設備市場—全球產業規模、佔有率、趨勢、機會和預測(按模式、按應用、按最終用戶、按地區和競爭細分,2020-2030 年) 全球皮膚病診斷影像設備市場:市場規模、佔有率、趨勢分析(按方式、應用、最終用途和地區)、細分市場預測(2025-2030 年)

全球皮膚病診斷影像設備市場:市場規模、佔有率、趨勢分析(按方式、應用、最終用途和地區)、細分市場預測(2025-2030 年) 皮膚科影像設備市場,按影像類型、按應用、按最終用戶、按國家和地區 - 2025 年至 2032 年的行業分析、市場規模、市場佔有率和預測美國皮膚科影像設備市場規模、佔有率、趨勢分析報告:按模式、按應用、按最終用途、細分市場預測,2024-2030 年

皮膚科影像設備市場,按影像類型、按應用、按最終用戶、按國家和地區 - 2025 年至 2032 年的行業分析、市場規模、市場佔有率和預測美國皮膚科影像設備市場規模、佔有率、趨勢分析報告:按模式、按應用、按最終用途、細分市場預測,2024-2030 年