|

市場調查報告書

商品編碼

2038681

乳糜瀉治療市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。Celiac Disease Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

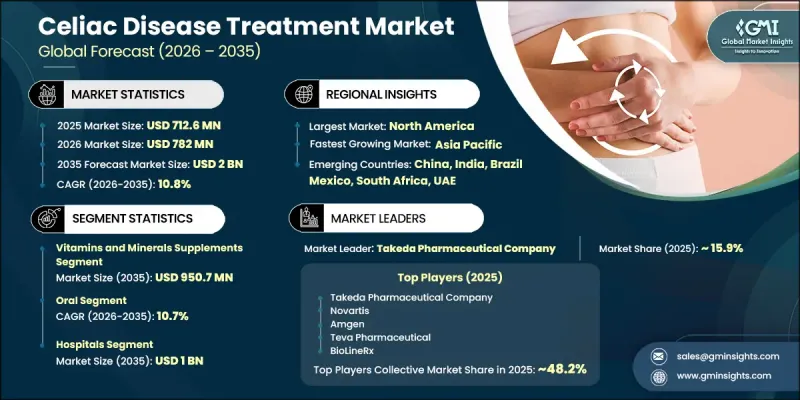

2025 年全球乳糜瀉治療市場價值為 7.126 億美元,預計到 2035 年將達到 20 億美元,年複合成長率為 10.8%。

乳糜瀉治療行業正經歷強勁成長,這主要得益於該疾病患病率的上升以及醫療專業人員對先進診斷解決方案的日益重視。隨著檢測率的提高,對有效治療方法的需求持續成長,從而推動了整體市場擴張。持續的研發工作正在推動藥物療法的創新,並促成了更多潛在治療方法進入市場。同時,無麩質飲食的日益普及以及非侵入性診斷技術的進步,正在改善疾病管理並加快診斷速度。專注於胃腸道疾病的專科醫療機構的擴張以及治療服務可及性的提高,進一步增強了患者的參與度。對先進治療方法臨床試驗投入的增加,以及長期管理輔助護理產品的普及,正在提高患者的治療依從性。醫療保健支出的成長以及醫療營養產品和處方藥分銷網路的改善,也在推動市場整體永續成長方面發揮著重要作用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 7.126億美元 |

| 預測市場規模 | 20億美元 |

| 複合年成長率 | 10.8% |

預計到2025年,維生素和礦物質補充劑市場規模將達到3.454億美元,到2035年將成長至9.507億美元。由於營養補充劑在治療疾病相關的營養缺乏方面發揮著至關重要的作用,該市場已佔據穩固地位。患者通常依賴這些補充劑來支持康復和維持整體健康,尤其是在解決營養吸收問題時。此外,針對有飲食限制人口的客製化營養產品需求不斷成長,也進一步推動了該細分市場的成長,因為這些產品有助於消化系統健康和疾病的長期管理。

預計到2025年,口服藥物市佔率將達到63.3%,並將在2035年之前以10.7%的複合年成長率成長。口服療法因其便捷易用而廣受歡迎,患者無需臨床支持即可獨立管理治療。監管機構對創新口服製劑的支持,以及持續的研發活動,正透過推出更有效、更容易取得的治療方案,推動該細分市場的擴張。

預計到2025年,北美乳糜瀉治療市場將佔據44.2%的市場佔有率,並在2035年之前以10.6%的複合年成長率成長。該地區的成長得益於完善的醫療保健基礎設施和眾多致力於自體免疫疾病研究的製藥公司的強大影響力。先進治療方法的高普及率、有利的報銷政策以及對創新治療方法臨床開發的日益重視,都進一步加速了全部區域市場的擴張。

目錄

第1章:調查方法

- 市場範圍和定義

- 研究途徑

- 對品質的承諾

- GMI的AI政策與對資料完整性的承諾

- 資訊來源一致性協議

- GMI的AI政策與對資料完整性的承諾

- 調查過程和可靠性評分

- 研究路徑的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 收入佔有率分析

- 基準年的計算

- 預測模型

- 關於調查透明度的補充信息

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 乳糜瀉盛行率增加

- 治療方案的技術進步

- 對無麩質產品的需求日益成長

- 診斷乳糜瀉的診斷技術不斷進步

- 產業潛在風險與挑戰

- 無麩質產品高成本

- 嚴格的監管核准

- 市場機遇

- 新型免疫療法的研發

- 營養補充品和營養補充品創新技術的廣泛應用

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 北美洲

- 管道分析(基於初步調查)

- 未來市場分析(基於初步研究)

- 投資和資金籌措趨勢

- 人工智慧/生成式人工智慧對市場的影響(基於初步研究)

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依治療方法,2022-2035年

- 維生素和礦物質補充劑

- 無麩質飲食

- 藥物治療

第6章 市場估計與預測:依給藥途徑分類,2022-2035年

- 口服

- 腸外

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院

- 專科診所

- 居家醫療

- 其他最終用戶

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- ActoBio

- Amgen

- Amneal Pharmaceuticals

- BioLineRx

- Calypso Biotech

- General Mills

- Glenmark Life Sciences

- Hikma Pharmaceuticals

- Innovate Biopharmaceutical

- Novartis

- Takeda Pharmaceutical Company

- Teva Pharmaceutical

- Viatris

- Zydus Pharmaceuticals

The Global Celiac Disease Treatment Market was valued at USD 712.6 million in 2025 and is estimated to grow at a CAGR of 10.8% to reach USD 2 billion by 2035.

The celiac disease treatment industry is experiencing strong growth due to the rising prevalence of the condition and improved awareness among healthcare professionals regarding advanced diagnostic solutions. As detection rates increase, the demand for effective treatment options continues to rise, supporting overall market expansion. Ongoing research and development efforts are driving innovation in pharmaceutical therapies, contributing to a broader pipeline of potential treatments expected to enter the market. At the same time, the growing adoption of gluten-free dietary practices and advancements in non-invasive diagnostic methods are improving disease management and enabling quicker diagnosis. Expansion of specialized healthcare facilities focused on gastrointestinal disorders, along with better access to treatment services, is further strengthening patient adoption rates. Increasing investments in clinical trials targeting advanced therapeutic approaches, along with the availability of supportive care products for long-term management, are enhancing treatment adherence. Rising healthcare spending and improved distribution networks for medical nutrition and prescription therapies are also playing a key role in driving sustained growth across the market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $712.6 Million |

| Forecast Value | $2 Billion |

| CAGR | 10.8% |

The vitamins and minerals supplements segment reached USD 345.4 million in 2025 and is projected to increase to USD 950.7 million by 2035. This segment holds a strong position due to the essential role of nutritional supplementation in managing deficiencies associated with the condition. Patients often rely on these supplements to support recovery and maintain overall health, particularly in addressing nutrient absorption challenges. Growing demand for specialized nutritional products tailored to individuals with dietary restrictions is further contributing to segment growth, as these solutions support digestive health and long-term disease management.

The oral segment accounted for 63.3% share in 2025 and is expected to grow at a CAGR of 10.7% throughout 2035. Oral therapies are widely preferred due to their convenience and ease of administration, allowing patients to manage treatment independently without requiring clinical assistance. Regulatory support for innovative oral formulations, combined with continuous research and development activities, is leading to the introduction of more effective and accessible treatment options, which are driving segment expansion.

North America Celiac Disease Treatment Market held a 44.2% share in 2025 and is anticipated to grow at a CAGR of 10.6% through 2035. The region's growth is supported by a well-established healthcare infrastructure and a strong presence of pharmaceutical companies engaged in autoimmune disease research. High adoption of advanced therapies, favorable reimbursement policies, and increasing focus on clinical development for innovative treatments are further accelerating market expansion across the region.

Key companies operating in the Global Celiac Disease Treatment Market include Amgen, Takeda Pharmaceutical Company, ActoBio, Novartis, Teva Pharmaceutical, Viatris, Amneal Pharmaceuticals, BioLineRx, Calypso Biotech, Hikma Pharmaceuticals, Glenmark Life Sciences, Zydus Pharmaceuticals, Innovate Biopharmaceutical, and General Mills. Companies in the Celiac Disease Treatment Market are focusing on strengthening their market position through continuous innovation and strategic initiatives. Significant investments are being made in research and development to advance targeted therapies and improve treatment effectiveness. Organizations are actively pursuing collaborations, partnerships, and licensing agreements to accelerate product development and expand their therapeutic portfolios. Increasing focus on clinical trials is enabling the introduction of novel treatment options with improved efficacy and safety profiles. Companies are also enhancing their distribution networks and expanding into emerging markets to capture new growth opportunities.

Table of Contents

Chapter 1 Research methodology

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 Regional trends

- 2.2.3 Treatment trends

- 2.2.4 Route of administration trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of celiac disease

- 3.2.1.2 Technological advancements in therapeutic options

- 3.2.1.3 Increasing demand for gluten-free products

- 3.2.1.4 Increasing diagnostic technologies for celiac disease diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of gluten-free products

- 3.2.2.2 Stringent regulatory approvals

- 3.2.3 Market opportunities

- 3.2.3.1 Development of novel immunotherapies

- 3.2.3.2 Increasing adoption of nutraceutical and supplement innovation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Pipeline analysis (Driven by Primary Research)

- 3.6 Future market analysis (Driven by Primary Research)

- 3.7 Investment and funding landscape

- 3.8 Impact of AI/ Gen AI on the market (Driven by Primary Research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Vitamins and mineral supplements

- 5.3 Gluten-free diet

- 5.4 Medical therapies

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Parenteral

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Specialty clinics

- 7.4 Homecare settings

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ActoBio

- 9.2 Amgen

- 9.3 Amneal Pharmaceuticals

- 9.4 BioLineRx

- 9.5 Calypso Biotech

- 9.6 General Mills

- 9.7 Glenmark Life Sciences

- 9.8 Hikma Pharmaceuticals

- 9.9 Innovate Biopharmaceutical

- 9.10 Novartis

- 9.11 Takeda Pharmaceutical Company

- 9.12 Teva Pharmaceutical

- 9.13 Viatris

- 9.14 Zydus Pharmaceuticals

乳糜瀉治療市場 - 全球市場預測 2026-2032

乳糜瀉治療市場 - 全球市場預測 2026-2032 乳糜瀉治療市場:2025-2030 年預測

乳糜瀉治療市場:2025-2030 年預測 乳糜瀉治療市場規模、佔有率、趨勢分析報告:按療法、分銷管道、地區和細分市場預測,2025 年至 2030 年

乳糜瀉治療市場規模、佔有率、趨勢分析報告:按療法、分銷管道、地區和細分市場預測,2025 年至 2030 年