|

市場調查報告書

商品編碼

2038667

工業吸塵器市場商機、成長要素、產業趨勢分析及2026-2035年預測。Industrial Vacuum Cleaner Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

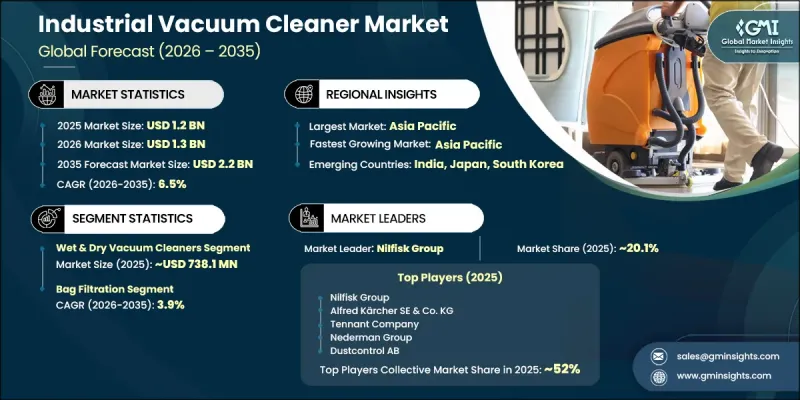

2025年全球工業吸塵器市場價值為12億美元,預計到2035年將以6.5%的複合年成長率成長至22億美元。

受工業快速擴張和各行業製造業活動持續成長的推動,該市場正經歷穩定成長。汽車、食品飲料、製藥和金屬加工等行業越來越依賴高性能的粉塵和顆粒物吸塵系統來維持安全的工作環境並確保產品品質。隨著生產設施規模和複雜性的增加,對高容量、持續運作的清潔設備的需求也不斷成長。同時,日益嚴格的環境和職業健康安全法規正在加速向先進工業真空解決方案的轉型。企業正在摒棄傳統的清潔方法,轉而採用專為提高效率和符合法規要求而設計的專用系統。對職業健康標準的日益重視也是推動市場成長的重要因素。包括北美、歐洲和亞太地區在內的主要地區的法律規範對粉塵暴露和空氣品質設定了嚴格的限制。例如,美國的 OSHA 要求和歐洲的 ATEX 指南等標準正在推動採用具備 HEPA 級過濾能力和先進密封技術的認證真空系統。這些因素共同造就了一個以安全、效率和合規性為中心的市場格局。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 12億美元 |

| 預計金額 | 22億美元 |

| 複合年成長率 | 6.5% |

預計到2025年,乾濕兩用吸塵器市場規模將達到7.381億美元,並在2026年至2035年間以1.7%的複合年成長率成長。此細分市場持續成長的關鍵在於其高度的操作柔軟性,該系統能夠在單一系統中處理液態和固態廢棄物。這種整合功能減少了對多台設備的需求,並簡化了包括建築、汽車製造、金屬加工和食品製造在內的各個行業的工業清潔作業。多種附件、過濾選項和儲存配置可供選擇,從而提高了對不同工作環境的適應性。這些系統提供移動式和固定式兩種配置,方便工業用戶依照自身營運需求和設施規模進行部署。

袋式過濾器市佔率佔27.8%,預計到2035年將以3.9%的複合年成長率成長。其強大的市場地位歸功於其成本效益高、結構簡單以及在工業清潔領域的廣泛應用。袋式過濾器系統能夠有效捕捉常見的工業粉塵,且易於更換,從而減少維護工作量和停機時間。其價格實惠且與多種真空系統相容,使其成為傳統製造環境、建築工地和一般工業維護工作的首選。

中國工業吸塵器市場預計到2025年將達到1.408億美元,並在2026年至2035年間以8.2%的複合年成長率成長。中國仍然是重要的成長中心,這得益於其龐大且快速發展的製造業生態系統。電子組裝、汽車製造、金屬加工和食品加工等行業的生產活動不斷擴大,為市場需求提供了強勁支撐。在這些行業中,高效的粉塵管理對於確保工作場所安全至關重要。遍布各地的工業園區和製造群持續推動對可攜式和固定式吸塵器系統的穩定需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 關鍵終端用戶產業的工業化和製造業活動擴張

- 嚴格的職業健康與安全 (OHS) 和環境法規

- 在食品飲料和製藥製造業的應用不斷擴大。

- 陷阱與挑戰

- 先進系統的高初始投資和總擁有成本

- 低成本取代傳統清潔方法的方案

- 機會

- 高效能空氣微粒過濾與先進粉塵控制技術的融合

- 物聯網賦能的智慧監控與預測性維護功能的實施現狀

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析(基於初步研究)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 區域價格波動

- 原物料成本對價格的影響

- 價格因產品類型和過濾技術而異。

- 貿易資料分析(HS編碼8508.60)(基於付費資料庫)

- 進出口量和進口額趨勢(基於付費資料庫)

- 主要貿易路線及關稅的影響(基於付費資料庫)

- 主要出口國

- 主要進口國

- 貿易政策變化及其影響評估

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- GenAI 各細分市場的應用案例與部署藍圖

- 預測性維護的最佳化

- 自主導航和路線規劃

- 智慧過濾監控和警報

- 面向服務承包商的人工智慧需求預測

- 風險、限制和監管考量

- 人工智慧真空系統投資趨勢

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要製造商分類的已安裝產能(基於初步調查)

- 運轉率和擴張計劃(基於初步調查)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 乾式吸塵器

- 用於清洗的吸塵器

- 乾濕兩用吸塵器

第6章 市場估算與預測:依過濾技術分類,2022-2035年

- 袋式過濾

- 濾芯過濾

- 旋風過濾

- 高效能空氣過濾(HEPA過濾)

- 混合過濾系統

第7章 市場估計與預測:依動力來源,2022-2035年

- 電的

- 氣動型

- 電池供電

- 燃油動力

第8章 市場估算與預測:依系統類型分類,2022-2035年

- 可攜式的

- 固定式

第9章 市場估計與預測:依最終用戶產業分類,2022-2035年

- 食品/飲料

- 製藥

- 金屬加工

- 車

- 其他(建築、製造等)

第10章 市場估價與預測:依銷售管道分類,2022-2035年

- 線上

- 離線

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第12章:公司簡介

- 全球主要公司

- Alfred Karcher SE & Co. KG

- Nilfisk Group

- Tennant Company

- Ruwac Industriesauger GmbH

- Delfin Industrial Vacuums

- Nederman Group

- Depureco Industrial Vacuums Srl

- 該地區頂尖公司

- American Vacuum Company

- Tiger-Vac International Inc.

- Vac-U-Max

- Goodway Technologies

- RGS Vacuum Systems(RGS Impianti)

- Dustcontrol

- G-Winner Ltd.

- Emerging & Specialized Players

- Pullman-Ermator AB

- Waidr Vacuum Cleaner(Shanghai)Co., Ltd

- Delfin Pharma Range

- Ruwac Battery-Powered Series

- Nilfisk Battery-Powered Industrial Line

- Tiger-Vac Cleanroom Systems

- Dustless Technologies

The Global Industrial Vacuum Cleaner Market was valued at USD 1.2 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 2.2 billion by 2035.

The market is experiencing consistent growth driven by rapid industrial expansion and the continuous rise in manufacturing activities across multiple sectors. Industries such as automotive, food and beverage, pharmaceuticals, and metal fabrication are increasingly dependent on high-performance dust and particulate extraction systems to maintain safe working conditions and ensure product quality. The growing scale and complexity of production facilities are strengthening the demand for high-capacity, continuous-duty cleaning equipment. At the same time, stricter environmental and workplace safety regulations are accelerating the shift toward advanced industrial vacuum solutions. Organizations are moving away from traditional cleaning methods and adopting specialized systems designed for efficiency and compliance. Increasing focus on occupational health standards is also acting as a strong growth catalyst. Regulatory frameworks across major regions, including North America, Europe, and Asia Pacific, are enforcing strict limits on dust exposure and air quality. Standards such as OSHA requirements in the United States and ATEX guidelines in Europe are driving the adoption of certified vacuum systems equipped with HEPA-grade filtration and advanced containment technologies. These combined factors are shaping a market landscape centered on safety, efficiency, and regulatory compliance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.2 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 6.5% |

The wet and dry vacuum cleaners segment generated USD 738.1 million in 2025 and is projected to grow at a CAGR of 1.7% from 2026 to 2035. This segment continues to lead the market due to its high operational flexibility, allowing it to handle both liquid and dry waste within a single system. This integrated capability reduces the need for multiple machines and streamlines industrial cleaning operations across various sectors, including construction, automotive production, metal processing, and food manufacturing. The availability of different attachments, filtration options, and storage configurations enhances its adaptability across diverse working environments. These systems are offered in both mobile and fixed formats, enabling industrial users to deploy them based on operational requirements and facility scale.

The bag filtration segment held a 27.8% share and is expected to grow at a CAGR of 3.9% through 2035. Its strong market presence is attributed to its cost efficiency, simple structure, and wide usage across industrial cleaning applications. Bag filtration systems are highly effective in capturing standard industrial dust and are easy to replace, which reduces maintenance effort and downtime. Their affordability and compatibility with a wide range of vacuum systems make them a preferred choice across traditional manufacturing environments, construction activities, and general industrial maintenance operations.

China Industrial Vacuum Cleaner Market reached USD 140.8 million in 2025 and is projected to grow at a CAGR of 8.2% from 2026 to 2035. The country remains a key growth center due to its large-scale and rapidly evolving manufacturing ecosystem. Demand is strongly supported by expanding production activities in sectors such as electronics assembly, automotive manufacturing, metalworking, and food processing, where efficient dust management is essential for operational safety. The extensive network of industrial zones and manufacturing clusters continues to generate sustained demand for both portable and stationary vacuum systems.

Key companies operating in the Global Industrial Vacuum Cleaner Market include Alfred Karcher SE & Co. KG, Nilfisk Group, Tennant Company, Nederman Group, Delfin Industrial Vacuums, Ruwac Industriesauger GmbH, Depureco Industrial Vacuums Srl, American Vacuum Company, Tiger-Vac International Inc., Vac-U-Max, Goodway Technologies, RGS Vacuum Systems (RGS Impianti), Dustcontrol, G-Winner Ltd., Pullman-Ermator AB, Waidr Vacuum Cleaner (Shanghai) Co., Ltd, Delfin Pharma Range, Ruwac Battery-Powered Series, Nilfisk Battery-Powered Industrial Line, Tiger-Vac Cleanroom Systems, and Dustless Technologies. Companies in the Industrial Vacuum Cleaner Market are strengthening their competitive position through continuous product innovation, technological upgrades, and expansion of application-specific solutions. Manufacturers are increasingly focusing on energy-efficient and high-capacity systems that meet evolving industrial cleaning requirements. The integration of advanced filtration technologies, including HEPA systems and improved dust containment mechanisms, is becoming a core development area. Many players are also investing in portable and battery-operated designs to enhance operational flexibility. Strategic partnerships with industrial end users are helping companies develop customized solutions tailored to specific operational environments. Expansion of distribution networks and regional manufacturing facilities is further supporting market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.3 Research approach

- 1.4 Data collection methods

- 1.5 Data mining sources

- 1.5.1 Global

- 1.5.2 Regional/Country

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.6.2 Key trends for market estimation

- 1.7 Primary research and validation

- 1.7.1 Primary sources

- 1.7.2 Forecast model

- 1.7.3 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Filtration Technology

- 2.2.4 Power Source

- 2.2.5 System Type

- 2.2.6 End User

- 2.2.7 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising industrialization and manufacturing activities across key end-use sectors

- 3.2.1.2 Strict occupational health & safety (OHS) and environmental regulations

- 3.2.1.3 Growing deployment in food & beverage and pharmaceutical manufacturing

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High initial investment and total cost of ownership for advanced systems

- 3.2.2.2 Availability of low-cost conventional cleaning substitutes

- 3.2.3 Opportunities

- 3.2.3.1 Integration of HEPA filtration and advanced dust containment technologies

- 3.2.3.2 Adoption of IoT-enabled smart monitoring and predictive maintenance features

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.9.3 Regional price variations

- 3.9.4 Impact of raw material costs on pricing

- 3.9.5 Pricing by product type and filtration technology

- 3.10 Trade data analysis (HS code 8508.60) (driven by paid database)

- 3.10.1 Import/export volume and value trends (driven by paid database)

- 3.10.2 Key trade corridors and tariff impact (driven by paid database)

- 3.10.3 Leading exporting countries

- 3.10.4 Leading importing countries

- 3.10.5 Trade policy changes and impact assessment

- 3.11 Impact of AI and generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases and adoption roadmap by segment

- 3.11.3 Predictive maintenance optimization

- 3.11.4 Autonomous navigation and path planning

- 3.11.5 Smart filtration monitoring and alerts

- 3.11.6 AI-powered demand forecasting for service contractors

- 3.11.7 Risks, limitations and regulatory considerations

- 3.11.8 Investment trends in AI-enabled vacuum systems

- 3.12 Capacity and production landscape (driven by primary research)

- 3.12.1 Installed capacity by region and key producer (driven by primary research)

- 3.12.2 Capacity utilization rates and expansion pipelines (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Dry Vacuum Cleaners

- 5.3 Wet Vacuum Cleaners

- 5.4 Wet & Dry Vacuum Cleaners

Chapter 6 Market Estimates & Forecast, By Filtration Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Bag Filtration

- 6.3 Cartridge Filtration

- 6.4 Cyclonic Filtration

- 6.5 HEPA Filtration

- 6.6 Hybrid Filtration Systems

Chapter 7 Market Estimates & Forecast, By Power Source, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Electric

- 7.3 Pneumatic

- 7.4 Battery-Powered

- 7.5 Fuel-Powered

Chapter 8 Market Estimates & Forecast, By System Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Portable

- 8.3 Stationary

Chapter 9 Market Estimates & Forecast, By End User Industry, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Food & Beverage

- 9.3 Pharmaceutical

- 9.4 Metal Working

- 9.5 Automotive

- 9.6 Others (construction, manufacturing, etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.3 Offline

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Top Global Players

- 12.1.1 Alfred Karcher SE & Co. KG

- 12.1.2 Nilfisk Group

- 12.1.3 Tennant Company

- 12.1.4 Ruwac Industriesauger GmbH

- 12.1.5 Delfin Industrial Vacuums

- 12.1.6 Nederman Group

- 12.1.7 Depureco Industrial Vacuums Srl

- 12.2 Regional Champions

- 12.2.1 American Vacuum Company

- 12.2.2 Tiger-Vac International Inc.

- 12.2.3 Vac-U-Max

- 12.2.4 Goodway Technologies

- 12.2.5 RGS Vacuum Systems (RGS Impianti)

- 12.2.6 Dustcontrol

- 12.2.7 G-Winner Ltd.

- 12.3 Emerging & Specialized Players

- 12.3.1 Pullman-Ermator AB

- 12.3.2 Waidr Vacuum Cleaner (Shanghai) Co., Ltd

- 12.3.3 Delfin Pharma Range

- 12.3.4 Ruwac Battery-Powered Series

- 12.3.5 Nilfisk Battery-Powered Industrial Line

- 12.3.6 Tiger-Vac Cleanroom Systems

- 12.3.7 Dustless Technologies