|

市場調查報告書

商品編碼

2038664

曲棍球裝備市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。Field Hockey Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

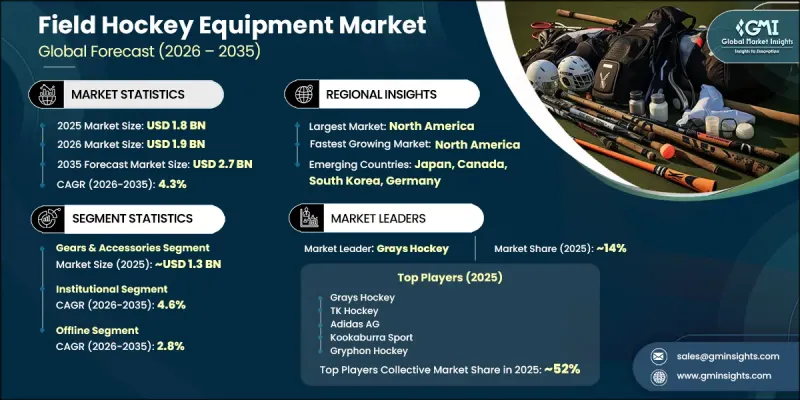

全球曲棍球裝備市場預計到 2025 年將價值 18 億美元,預計到 2035 年將以 4.3% 的複合年成長率成長至 27 億美元。

市場擴張的驅動力來自學校、大學和體育學院對曲棍球運動的日益普及,以及青少年和業餘球員參與度的提高。教育機構越來越重視體育教育和系統化的體育訓練,這推動了對球桿、球、護具和訓練配件等基本裝備的穩定需求。體育俱樂部也在擴大聯賽和訓練項目的規模,進一步強化了裝備採購週期。同時,政府主導的體育推廣政策和基層計畫正在促進曲棍球運動的更廣泛參與和人才培養。對體育基礎設施(包括現代化體育場、人工草皮草皮場地和訓練設施)的投入增加也促進了市場成長。這些設施需要符合安全性和耐用性要求的標準化高性能裝備。對球員安全、提升運動表現和遵守法規的日益關注也進一步影響消費者的購買行為。製造商正積極回應,提供耐用、輕巧且符合人體工學設計的裝備,以滿足比賽和訓練環境的需求,從而推動市場長期需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 18億美元 |

| 預測金額 | 27億美元 |

| 複合年成長率 | 4.3% |

預計到2025年,裝備及配件市場規模將達到13億美元,並在2026年至2035年間以4.4%的複合年成長率成長。該細分市場在曲棍球裝備市場中佔據主導地位,因為對安全和提升運動表現至關重要的裝備在曲棍球運動中扮演著舉足輕重的角色。此細分市場包括護腿板、手套、頭盔和護齒等防護裝備,以及握把、球包和護具等輔助裝備。由於球員對安全標準和預防傷害的意識不斷增強,各水準球員對防護裝備的使用率顯著提高。訓練和比賽中頻繁使用防護裝備會產生定期更換的需求,這進一步推動了市場成長。此外,能夠提升控球、舒適度和比賽效率的性能導向配件也越來越受到業餘和職業球員的青睞。

預計到2025年,線下銷售管道將佔據62.2%的市場佔有率,並預計在2026年至2035年間以2.8%的複合年成長率成長。線下零售之所以仍佔據主導地位,主要得益於專業運動用品店、機構供應商和多品牌零售商的強大影響力。買家,尤其是學校、俱樂部和體育組織,更傾向於在購買前親自檢查產品,以評估其品質、耐用性和舒適度。對於性能和安全性至關重要的護具和球桿而言,這一點尤其重要。線下管道還能提供即時產品供應,滿足訓練和比賽期間的緊急採購需求。銷售人員提供的個人化支援和專家產品選擇建議進一步增強了買家的信心。教育機構和體育學院透過成熟的零售網路進行大量採購,也持續鞏固了該管道的優勢。能夠親自檢查產品,加上與值得信賴的供應商建立的良好關係以及規範的採購流程,共同維持了線下分銷在市場上的主導地位。

美國曲棍球裝備市場預計到2025年將達到6.515億美元,並在2026年至2035年間以4.6%的複合年成長率成長。儘管美國市場仍屬於小眾市場,但其組織結構完善,需求主要集中在學校、學院和正規運動項目。大學體育項目和教育機構在推動球桿、球、護具和訓練配件的穩定需求方面發揮著重要作用。產品創新著重於輕質複合材料、提高耐用性以及針對人造草坪場地最佳化的符合人工草皮的設計。分銷主要透過體育用品零售商、機構採購系統和支援結構化採購週期的線上管道進行。遵守大學體育標準和監管準則對產品設計和材料選擇有顯著影響。女子大學聯賽和青少年發展項目的參與度不斷提高,進一步推動了市場的穩定成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 擴大學校和體育俱樂部曲棍球運動的參與度

- 增加對體育基礎設施和訓練設施的投資

- 輕量化和高性能設備的技術進步

- 陷阱與挑戰

- 在某些地區,它的受歡迎程度與其他主流運動相比有限。

- 專業級設備高成本

- 機會

- 在全球擴大女子和青少年冰球項目

- 對客製化、球員專用裝備的需求日益成長

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 價格分析(基於初步調查)

- 過去價格趨勢分析(基於初步調查)(2019-2024 年)

- 根據業務類型(高階、中階、經濟型)制定的定價策略(基於初步調查)

- 不同分銷管道的價格波動

- 區域價格基準

- 影響定價的因素

- 貿易數據分析(基於付費資料庫)

- 進出口量和進口額趨勢(基於付費資料庫)(2019-2024 年)

- 主要貿易路線和主要進出口國(基於付費資料庫)

- 關稅和貿易壁壘的影響

- 區域貿易趨勢和機遇

- 分銷基礎設施和通路滲透狀況(基於初步調查)

- 按地區和業務類型(專賣店、電子商務、量販店)分類的通路覆蓋率(基於初步調查)

- 最後一公里基礎設施差異和新興管道變化(基於初步研究)

- 全通路策略的實施與數位化成熟度

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 工具

- 曲棍球桿

- 曲棍球

- 裝備和配件

- 服飾

- 鞋類

- 口罩和護目鏡

- 手套墊

- 頭盔

- 其他

- 訓練和設施設備

第6章 市場估算與預測:依最終用戶分類,2022-2035年

- 個人

- 對機構而言

- 晉升

第7章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 離線

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第9章:公司簡介

- Grays Hockey

- Gryphon Hockey Ltd

- Harrow Sports

- Kookaburra Sport Pty Ltd

- Mazon Hockey

- OBO Hockey

- Osaka World

- Ritual Hockey

- STX

- Atlas Hockey

- Adidas AG

- Dita International BV

- Y1 Sport Limited

- TK Hockey

- Voodoo Hockey

The Global Field Hockey Equipment Market was valued at USD 1.8 billion in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 2.7 billion by 2035.

Market expansion is supported by the rising inclusion of field hockey across schools, universities, and sports academies, along with increasing participation among youth and amateur players. Educational institutions are placing greater emphasis on physical education and structured sports training, which is boosting consistent demand for essential equipment such as sticks, balls, protective gear, and training accessories. Sports clubs are also expanding organized leagues and training programs, which further strengthen equipment procurement cycles. In parallel, government-backed sports development initiatives and grassroots programs are encouraging wider participation and talent development in field hockey. Increased investment in sports infrastructure, including modern stadiums, synthetic turf fields, and training complexes, is also contributing to market growth. These facilities require standardized, high-performance equipment that meets safety and durability expectations. Growing emphasis on player safety, performance enhancement, and regulatory compliance is further influencing purchasing behavior. Manufacturers are responding with durable, lightweight, and ergonomically designed equipment suited for both competitive and training environments, reinforcing long-term market demand.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.8 Billion |

| Forecast Value | $2.7 Billion |

| CAGR | 4.3% |

The gears and accessories segment accounted for USD 1.3 billion in 2025 and is projected to grow at a CAGR of 4.4% from 2026 to 2035. This segment holds a dominant position in the field hockey equipment market due to the essential role of safety and performance-enhancing gear in the sport. It includes protective equipment such as shin guards, gloves, helmets, and mouthguards, along with supporting accessories like grips, bags, and protective wear. Rising awareness of athlete safety standards and injury prevention has significantly increased the adoption of protective gear across all skill levels. Frequent usage during training sessions and matches leads to regular replacement demand, which further sustains market growth. In addition, performance-oriented accessories that improve control, comfort, and gameplay efficiency are gaining traction among both amateur and professional players.

The offline distribution channel held a share of 62.2% in 2025 and is expected to grow at a CAGR of 2.8% from 2026 to 2035. Offline retail continues to dominate due to the strong presence of specialty sports stores, institutional suppliers, and multi-brand retail outlets. Buyers, particularly schools, clubs, and sports organizations, prefer physical evaluation of equipment to assess quality, durability, and comfort before purchase. This is especially important for protective gear and sticks, where performance and safety considerations are critical. Offline channels also provide immediate product availability, which supports urgent procurement needs during training cycles and competitive seasons. Personalized assistance from sales staff and expert guidance on product selection further enhances buyer confidence. Bulk purchasing by educational institutions and sports academies through established retail networks continues to reinforce this channel's strength. The ability to physically inspect products, combined with trusted supplier relationships and structured procurement processes, sustains the dominance of offline distribution in the market.

U.S. Field Hockey Equipment Market captured USD 651.5 million in 2025 and is anticipated to grow at a CAGR of 4.6% from 2026 to 2035. The market in the United States remains niche but well-organized, with demand largely concentrated within schools, colleges, and structured athletic programs. Collegiate sports programs and educational institutions play a key role in driving consistent demand for sticks, balls, protective equipment, and training accessories. Product innovation is focused on lightweight composite materials, enhanced durability, and ergonomic designs optimized for artificial turf playing conditions. Distribution is primarily managed through sports retailers, institutional procurement systems, and online channels that support structured purchasing cycles. Compliance with collegiate sports standards and regulatory guidelines significantly influences product design and material selection. Growing participation in women's collegiate leagues and youth development programs further supports steady market expansion.

Major players operating in the Global Field Hockey Equipment Industry include Adidas AG, Atlas Hockey, Dita International B.V., Grays Hockey, Gryphon Hockey Ltd, Harrow Sports, Kookaburra Sport Pty Ltd, Mazon Hockey, OBO Hockey, Osaka World, Ritual Hockey, STX, TK Hockey, Voodoo Hockey, and Y1 Sport Limited. Companies in the Field Hockey Equipment Market are focusing on expanding product innovation pipelines by developing lightweight, high-durability materials that improve performance and safety. They are strengthening brand presence through sponsorships of schools, clubs, and tournaments to increase visibility among young athletes. Strategic collaborations with sports academies and institutional buyers are helping secure bulk procurement contracts. Manufacturers are also investing in advanced manufacturing technologies to enhance precision and consistency in equipment quality. Digital distribution channels and direct-to-consumer platforms are being expanded to improve accessibility. Product customization options are being introduced to cater to player-specific requirements. In addition, companies are emphasizing sustainability by using eco-friendly materials and recyclable packaging. Aggressive marketing through sports endorsements and athlete partnerships is further reinforcing brand trust and expanding global reach across competitive and grassroots segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 End User

- 2.2.4 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing participation in field hockey across schools and sports clubs

- 3.2.1.2 Rising investments in sports infrastructure and training facilities

- 3.2.1.3 Technological advancements in lightweight and high-performance equipment

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Limited popularity compared to other mainstream sports in certain regions

- 3.2.2.2 High cost of professional-grade equipment

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of women's and youth hockey programs globally

- 3.2.3.2 Growing demand for customized and player-specific gear

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research) (2019-2024)

- 3.9.2 Pricing strategy by player type (premium, mid-range, value) (driven by primary research)

- 3.9.3 Price variation across distribution channels

- 3.9.4 Regional price benchmarking

- 3.9.5 Factors influencing price points

- 3.10 Trade data analysis (driven by paid database)

- 3.10.1 Import/export volume & value trends (driven by paid database) (2019-2024)

- 3.10.2 Key trade corridors & major importers/exporters (driven by paid database)

- 3.10.3 Tariff impact & trade barriers

- 3.10.4 Regional trade dynamics & opportunities

- 3.11 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.11.1 Channel coverage by region & format (specialty stores, e-commerce, mass retail) (driven by primary research)

- 3.11.2 Last-mile infrastructure gaps & emerging channel shifts (driven by primary research)

- 3.11.3 Omnichannel strategy adoption & digital maturity

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Equipment

- 5.2.1 Field hockey stick

- 5.2.2 Field hockey ball

- 5.3 Gears & Accessories

- 5.3.1 Apparel

- 5.3.2 Footwear

- 5.3.3 Masks & goggles

- 5.3.4 Gloves & pads

- 5.3.5 Helmets

- 5.3.6 Others

- 5.4 Training & Facility Equipment

Chapter 6 Market Estimates & Forecast, By End User, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Individual

- 6.3 Institutional

- 6.4 Promotional

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Online

- 7.3 Offline

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Grays Hockey

- 9.2 Gryphon Hockey Ltd

- 9.3 Harrow Sports

- 9.4 Kookaburra Sport Pty Ltd

- 9.5 Mazon Hockey

- 9.6 OBO Hockey

- 9.7 Osaka World

- 9.8 Ritual Hockey

- 9.9 STX

- 9.10 Atlas Hockey

- 9.11 Adidas AG

- 9.12 Dita International B.V.

- 9.13 Y1 Sport Limited

- 9.14 TK Hockey

- 9.15 Voodoo Hockey

冰球裝備市場報告:依產品類型、通路、最終用戶和地區分類,2026-2034年

冰球裝備市場報告:依產品類型、通路、最終用戶和地區分類,2026-2034年 曲棍球裝備市場:依裝備類型、材質、價格範圍、銷售管道和最終用戶分類-2026-2032年全球市場預測冰球裝備市場:2026-2032年全球市場預測(依裝備類型、性別、最終用戶和通路分類)

曲棍球裝備市場:依裝備類型、材質、價格範圍、銷售管道和最終用戶分類-2026-2032年全球市場預測冰球裝備市場:2026-2032年全球市場預測(依裝備類型、性別、最終用戶和通路分類) 冰球裝備市場分析及預測(至2035年):依類型、產品類型、材質、最終使用者、應用、技術、製造流程及安裝類型分類

冰球裝備市場分析及預測(至2035年):依類型、產品類型、材質、最終使用者、應用、技術、製造流程及安裝類型分類 全球冰球裝備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球冰球裝備市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 冰球滑冰市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年曲棍球裝備市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、運動類型、通路、地區和競爭格局分類,2021-2031年冰球裝備市場-全球產業規模、佔有率、趨勢、機會和預測,依產品類型、銷售通路、地區和競爭格局分類,2021-2031年預測

冰球滑冰市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年曲棍球裝備市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、運動類型、通路、地區和競爭格局分類,2021-2031年冰球裝備市場-全球產業規模、佔有率、趨勢、機會和預測,依產品類型、銷售通路、地區和競爭格局分類,2021-2031年預測 冰球裝備市場規模、佔有率和成長分析(按產品、材料、價格分佈、通路、最終用戶和地區分類)-2026-2033年產業預測

冰球裝備市場規模、佔有率和成長分析(按產品、材料、價格分佈、通路、最終用戶和地區分類)-2026-2033年產業預測 全球冰上曲棍球鞋市場

全球冰上曲棍球鞋市場