|

市場調查報告書

商品編碼

2038647

超級跑車市場機會、成長要素、產業趨勢分析及2026-2035年預測。Hyper Cars Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025年全球超級跑車市場價值58億美元,預計2035年將以6.6%的複合年成長率成長至109億美元。

由於市場對兼具極致速度、先進工程技術和獨特性的超豪華高性能汽車的需求不斷成長,超級跑車市場正在蓬勃發展。超級跑車是專為精英客戶和收藏家設計的限量版車型,擁有最先進的空氣動力學設計、輕量化結構和先進的動力系統。為了滿足不斷變化的性能和監管要求,製造商除了採用高功率內燃機外,還擴大將混合動力和純電動動力傳動系統整合到超級跑車中。先進的數位系統、智慧駕駛輔助功能和豪華內裝的運用進一步提升了這些車輛的吸引力。消費者對個人化、獨特性和高階汽車體驗的日益成長的偏好也推動了市場的擴張。碳纖維和高強度合金等輕量化材料的不斷進步正在提升車輛的速度、操控性和效率。此外,主動式空氣動力學、自我調整懸吊系統和高性能電子設備的創新正在重新定義駕駛動態。傳統工藝與現代卓越工程技術的融合,持續塑造全球超級跑車產業的競爭格局。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 58億美元 |

| 預測市場規模 | 109億美元 |

| 複合年成長率 | 6.6% |

預計到2025年,內燃機市佔率將達到71%,並在2035年之前以6.5%的複合年成長率成長。該細分市場憑藉其高性能、獨特的引擎聲音和精緻的駕駛體驗,持續吸引消費者的濃厚興趣。傳統動力傳動系統技術因其反應迅速、技術成熟,以及即使在嚴苛的駕駛條件下也能提供穩定性能,仍備受青睞。

標準型超級跑車預計在2025年佔據82%的市場佔有率,並將在2026年至2035年間以6.5%的複合年成長率成長。此類別車型旨在提供極致性能的同時,兼顧日常駕駛的實用性。這些車型通常在高速性能和舒適性配置之間取得平衡,例如自動空調系統、整合式資訊娛樂系統以及便利的上下車設計,使其在豪華性能車領域更具實用性。

預計到2035年,義大利超級跑車市場將以5.6%的複合年成長率成長。義大利的優勢在於其深厚的高階汽車工程傳統和以性能為導向的車輛研發。混合動力技術、碳纖維結構和空氣動力學設計的不斷進步,正協助下一代超級跑車的生產。義大利製造商正日益將電氣化技術與傳統的性能工程相結合,以在滿足不斷變化的排放氣體法規的同時,提升效率和駕駛體驗。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 超級富豪階級人士(UHNWI)數量增加以及奢侈品支出成長

- 對限量生產的高性能汽車的需求日益成長

- 向電動動力傳動系統技術的轉型和日益增強的環保意識

- 輕質材料和動態的技術進步

- 增加對賽道日體驗和賽車運動傳統的投入。

- 產業潛在風險與挑戰

- 過高的購置和擁有成本

- 生產量限制及交貨日期延期

- 複雜的型式認可和監管合規要求

- 傳統車迷對電動動力傳動系統的抗拒情緒

- 市場機遇

- 新興的電動超級跑車市場正在吸引新的參與企業。

- 亞太和中東超豪華市場需求不斷成長

- 高性能車輛中的數位化和互聯化

- 擴大專門針對超級跑車的活動、集會和品牌體驗。

- 專業製造商與主要OEM製造商之間的策略合作夥伴關係

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國環保署(EPA)排放標準(CAA 和 Tier 3 法規)

- 加州「先進清潔汽車II」法規

- 美國國家公路交通安全管理局對小批量製造商的限制

- 歐洲

- 歐盟二氧化碳排放標準(歐盟6/7法規)

- 歐盟小批量型式認證 (SSTA)

- 英國強制推行零排放車輛(ZEV)

- 法國的火星二氧化碳稅收獎勵制度

- 亞太地區

- 中國的新能源汽車政策

- 日本的綠色成長策略(2050年碳中和)

- 韓國的環保車輛政策

- 新加坡車輛排放氣體法規(VES)

- 拉丁美洲

- 巴西 PROCONVE排放標準

- 墨西哥的NOM排放法規

- 智利的電動旅遊戰略

- 中東和非洲(MEA)

- 阿拉伯聯合大公國2030年綠色交通戰略

- 沙烏地阿拉伯2030願景(交通電氣化)

- 南非汽車產業總體規劃(SAAM 2035)

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 電動動力傳動系統技術的演進

- 混合動力推進系統架構

- 先進的空氣動力學設計創新

- 新興技術

- 輕量化材料技術(碳纖維、鈦合金)

- 主動懸吊和底盤控制系統

- 當前技術趨勢

- 專利分析(基於初步研究)

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(高階、超值、成本加成)

- 貿易數據分析(基於付費資料庫)

- 進出口量和進出口額的趨勢

- 主要貿易走廊及關稅的影響

- 跨境電商分銷趨勢

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的設備產能

- 運轉率和擴張計劃

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 永續性和環境影響分析

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 關於碳足跡的考量

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按銷售額、地區和創新能力分類的層級定位矩陣。

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依促進因素分類,2022-2035年

- 內燃機(ICE)

- 電池式電動車

- 混合

第6章 市場估價與預測:依車身類型分類,2022-2035年

- 小轎車

- 敞篷車

- Roadster

第7章 市場估算與預測:依引擎排氣量分類,2022-2035年

- 排氣量小於1499毫升(緊湊型)

- 1500-2499 cc(中型)

- 超過 2500cc(全尺寸)

第8章 市場估算與預測:依績效類別分類,2022-2035年

- 標準超級跑車

- 超級跑車/超高性能

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 個人所有

- 賽道/比賽用途

- 汽車活動和展覽

- 租賃和體驗服務

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 瑞典

- 丹麥

- 波蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 以色列

第11章:公司簡介

- 世界公司

- Aston Martin Lagonda

- Bugatti Automobiles

- Ferrari

- Koenigsegg Automotive

- Lamborghini

- Lotus Cars

- McLaren Automotive

- Pagani Automobili

- Porsche

- 本地球員

- Hennessey Performance Engineering

- Rimac Automobili

- SSCDR

- W Motors

- 新興企業

- Apollo Automobil

- Aspark

- Czinger Vehicles

- Devel Motors

- Gordon Murray Automotive

- Pininfarina Automobili

- Zenvo Automotive

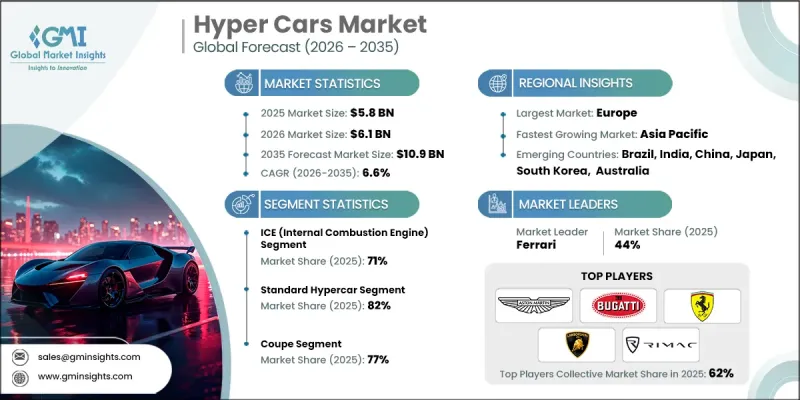

The Global Hyper Cars Market was valued at USD 5.8 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 10.9 billion by 2035.

The market is witnessing growth due to rising demand for ultra-luxury, high-performance vehicles that combine extreme speed with advanced engineering and exclusivity. Hyper cars are limited-production automobiles designed for elite customers and collectors, offering cutting-edge aerodynamics, lightweight construction, and advanced propulsion technologies. Manufacturers are increasingly integrating hybrid and fully electric powertrains alongside high-output internal combustion engines to meet evolving performance and regulatory expectations. The incorporation of advanced digital systems, intelligent driving support features, and luxury-focused interiors is further enhancing the appeal of these vehicles. Growing consumer preference for personalization, exclusivity, and high-end automotive experiences is also supporting market expansion. Continuous advancements in lightweight materials such as carbon fiber and high-strength alloys are improving speed, handling, and efficiency. In addition, innovation in active aerodynamics, adaptive suspension systems, and performance-focused electronics is redefining driving dynamics. The combination of heritage craftsmanship and modern engineering excellence continues to shape the competitive landscape of the hyper cars industry globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.8 Billion |

| Forecast Value | $10.9 Billion |

| CAGR | 6.6% |

The internal combustion engine segment held a 71% share in 2025 and is expected to grow at a CAGR of 6.5% through 2035. This segment continues to attract strong interest due to its high-performance characteristics, distinctive engine acoustics, and refined driving experience. Traditional powertrain technologies remain widely valued for their responsiveness, engineering maturity, and ability to deliver consistent performance under extreme driving conditions.

The standard hypercar segment accounted for 82% share in 2025 and is projected to expand at a CAGR of 6.5% during 2026-2035. This category includes vehicles engineered for extreme performance while maintaining a degree of usability for regular driving. These models typically balance high-speed capability with comfort-oriented features such as climate control systems, infotainment integration, and improved cabin accessibility, making them more practical within the luxury performance segment.

Italy Hyper Cars Market is expected to grow at a CAGR of 5.6% through 2035. The country benefits from a strong heritage in luxury automotive engineering and performance-focused vehicle development. Continuous advancements in hybrid technologies, carbon-fiber construction, and aerodynamic design are supporting next-generation hypercar production. Italian manufacturers are increasingly combining electrification with traditional performance engineering, enhancing both efficiency and driving experience while meeting evolving emissions standards.

Key companies operating in the Global Hyper Cars Market include Ferrari, Bugatti, McLaren, Lamborghini, Aston Martin, Koenigsegg, Rimac, Pagani, Lotus, and Mercedes-AMG. Companies in the Hyper Cars Market are focusing on strengthening their competitive position through continuous innovation in powertrain technologies, lightweight materials, and aerodynamic engineering. Manufacturers are investing heavily in hybrid and electric performance systems to align with evolving emission standards while maintaining extreme performance levels. Strategic emphasis is being placed on exclusivity, limited production models, and highly personalized vehicle configurations to enhance brand value. Collaborations with advanced material suppliers and technology firms are enabling improvements in carbon fiber usage, battery systems, and vehicle intelligence platforms. Companies are also expanding their global presence through selective market entry strategies and exclusive dealership networks.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Propulsion

- 2.2.3 Body Style

- 2.2.4 Engine Size

- 2.2.5 Performance Tier

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising ultra-high-net-worth individual (UHNWI) population & luxury spending

- 3.2.1.2 Growing demand for exclusive, limited-edition performance vehicles

- 3.2.1.3 Shift toward electric powertrain technology & environmental consciousness

- 3.2.1.4 Technological advancements in lightweight materials & aerodynamics

- 3.2.1.5 Increasing investment in track-day experiences & motorsport heritage

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Prohibitively high acquisition & ownership costs

- 3.2.2.2 Limited production volumes & extended waiting periods

- 3.2.2.3 Complex homologation & regulatory compliance requirements

- 3.2.2.4 Customer resistance to electric powertrains among traditional enthusiasts

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging electric hypercar segment attracting new entrants

- 3.2.3.2 Growing appetite in Asia Pacific & Middle East ultra-luxury markets

- 3.2.3.3 Digitalization & connectivity integration in performance vehicles

- 3.2.3.4 Expansion of hypercar-focused events, rallies & brand experiences

- 3.2.3.5 Strategic partnerships between boutique manufacturers & established OEMs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. EPA Emission Standards (CAA & Tier 3 Regulations)

- 3.4.1.2 California Advanced Clean Cars II Regulation

- 3.4.1.3 NHTSA Low Volume Manufacturer Regulations

- 3.4.2 Europe

- 3.4.2.1 EU CO2 Emission Standards (Euro 6/7 Regulations)

- 3.4.2.2 EU Small Series Type Approval (SSTA)

- 3.4.2.3 United Kingdom Zero Emission Vehicle (ZEV) Mandate

- 3.4.2.4 France Bonus-Malus CO2 Tax System

- 3.4.3 Asia Pacific

- 3.4.3.1 China New Energy Vehicle (NEV) Policy

- 3.4.3.2 Japan Green Growth Strategy (Carbon Neutrality 2050)

- 3.4.3.3 South Korea Eco-Friendly Vehicle Policy

- 3.4.3.4 Singapore Vehicular Emissions Scheme (VES)

- 3.4.4 Latin America

- 3.4.4.1 Brazil PROCONVE Emission Standards

- 3.4.4.2 Mexico NOM Emission Regulations

- 3.4.4.3 Chile Electromobility Strategy

- 3.4.5 MEA

- 3.4.5.1 UAE Green Mobility Strategy 2030

- 3.4.5.2 Saudi Arabia Vision 2030 (Transport Electrification)

- 3.4.5.3 South Africa Automotive Masterplan (SAAM 2035)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Electric powertrain technology evolution

- 3.7.1.2 Hybrid propulsion systems architecture

- 3.7.1.3 Advanced aerodynamic design innovations

- 3.7.2 Emerging technologies

- 3.7.2.1 Lightweight material technologies (carbon fiber, titanium)

- 3.7.2.2 Active suspension & chassis control systems

- 3.7.1 Current technological trends

- 3.8 Patent analysis (Driven by primary research)

- 3.9 Pricing analysis (Driven by primary research)

- 3.9.1 Historical price trend analysis

- 3.9.2 Pricing strategy by player type (premium, value, cost-plus)

- 3.10 Trade data analysis (Driven by paid database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.10.3 Cross-border e-commerce flows

- 3.11 Capacity & production landscape (Driven by primary research)

- 3.11.1 Installed capacity by region & key producer

- 3.11.2 Capacity utilization rates & expansion pipelines

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Sustainability and environmental impact analysis

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates and Forecast, By Propulsion, 2022 - 2035 ($ Million, Units)

- 5.1 Key trends

- 5.2 ICE (Internal Combustion Engine)

- 5.3 Battery electric

- 5.4 Hybrid

Chapter 6 Market Estimates and Forecast, By Body Style, 2022 - 2035 ($ Million, Units)

- 6.1 Key trends

- 6.2 Coupe

- 6.3 Convertible

- 6.4 Roadster

Chapter 7 Market Estimates and Forecast, By Engine Size, 2022 - 2035 ($ Million, Units)

- 7.1 Key trends

- 7.2 Below 1499 cc (Compact)

- 7.3 1500-2499 cc (Mid-size)

- 7.4 Above 2500 cc (Full-size)

Chapter 8 Market Estimates and Forecast, By Performance Tier, 2022 - 2035 ($ Million, Units)

- 8.1 Key trends

- 8.2 Standard hypercar

- 8.3 Mega car/ultra-performance

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Million, Units)

- 9.1 Key trends

- 9.2 Private ownership

- 9.3 Track / racing use

- 9.4 Automotive events & exhibitions

- 9.5 Rental & experiential services

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aston Martin Lagonda

- 11.1.2 Bugatti Automobiles

- 11.1.3 Ferrari

- 11.1.4 Koenigsegg Automotive

- 11.1.5 Lamborghini

- 11.1.6 Lotus Cars

- 11.1.7 McLaren Automotive

- 11.1.8 Pagani Automobili

- 11.1.9 Porsche

- 11.2 Regional Players

- 11.2.1 Hennessey Performance Engineering

- 11.2.2 Rimac Automobili

- 11.2.3 SSC North America

- 11.2.4 W Motors

- 11.3 Emerging Players

- 11.3.1 Apollo Automobil

- 11.3.2 Aspark

- 11.3.3 Czinger Vehicles

- 11.3.4 Devel Motors

- 11.3.5 Gordon Murray Automotive

- 11.3.6 Pininfarina Automobili

- 11.3.7 Zenvo Automotive

2026年全球超級跑車市場報告

2026年全球超級跑車市場報告 2026-2034年全球超級跑車市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球超級跑車市場規模、佔有率、趨勢和成長分析報告 2026-2030年全球超級跑車市場

2026-2030年全球超級跑車市場 超級跑車市場 - 全球產業規模、佔有率、趨勢、機會及預測(按動力系統、應用、車輛類型、地區和競爭格局分類,2021-2031年)

超級跑車市場 - 全球產業規模、佔有率、趨勢、機會及預測(按動力系統、應用、車輛類型、地區和競爭格局分類,2021-2031年) 超級跑車市場規模、佔有率和成長分析(按動力系統、最終用途和地區分類)—2026-2033年產業預測

超級跑車市場規模、佔有率和成長分析(按動力系統、最終用途和地區分類)—2026-2033年產業預測 全球超跑市場

全球超跑市場 超級跑車市場 -;車輛尺寸:緊湊型、中型和全尺寸;推進系統:內燃機、電動 - 全球產業分析、規模、佔有率、成長、趨勢及預測(2025-2035)

超級跑車市場 -;車輛尺寸:緊湊型、中型和全尺寸;推進系統:內燃機、電動 - 全球產業分析、規模、佔有率、成長、趨勢及預測(2025-2035) 全球超級跑車市場:市場規模、市場佔有率、趨勢、行業分析(依推進方式、應用和地區)、未來預測(2025-2034年)

全球超級跑車市場:市場規模、市場佔有率、趨勢、行業分析(依推進方式、應用和地區)、未來預測(2025-2034年)