|

市場調查報告書

商品編碼

2038644

彈藥市場商機、成長要素、產業趨勢分析及2026-2035年預測Ammunition Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

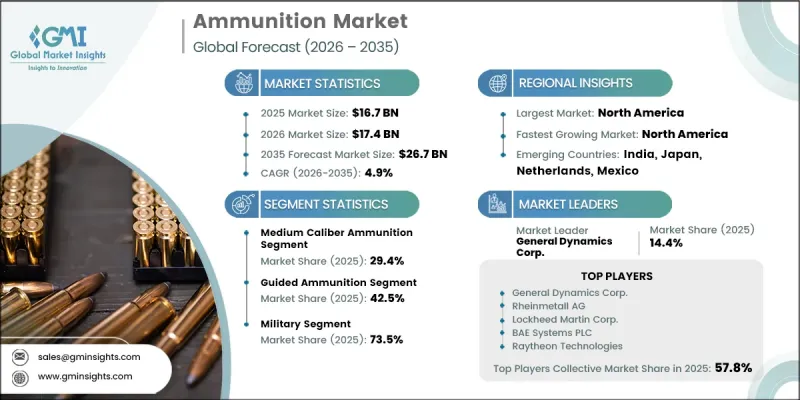

2025 年全球彈藥市場價值為 167 億美元,預計到 2035 年將達到 267 億美元,年複合成長率為 4.9%。

許多國家國防預算的增加支撐了市場成長,各國政府致力於加強軍事戰備、提升邊防安全並應對日益緊張的地緣政治局勢。先進防禦系統的採購增加以及軍隊的持續現代化也推動了彈藥需求的持續成長。除了軍事用途外,民用需求也在擴大,尤其是在北美和歐洲部分地區,這主要得益於休閒射擊和狩獵活動的日益普及,從而維持了穩定的消費水平。正規射擊場和競技射擊賽事的興起進一步強化了民用需求的成長趨勢。對國防安全保障的日益重視以及執法機關的現代化是支撐市場擴張的另一個重要因素。各國政府正在向安全部隊部署先進槍械,並維持穩定的彈藥儲備,以滿足作戰和訓練需求。新興經濟體的快速都市化和不斷變化的安全挑戰也進一步強化了採購週期。整體而言,在國防戰備和民用需求的雙重支撐下,彈藥需求保持穩定,確保了市場的長期韌性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 167億美元 |

| 預測市場規模 | 267億美元 |

| 複合年成長率 | 4.9% |

到2025年,中口徑彈藥市佔率將達到29.4%。此細分市場的成長主要得益於軍警執法機關廣泛應用於裝甲系統、海軍平台和防空作戰。其均衡的火力和高效的作戰性能正推動其不斷融入現代化防禦系統,從而支撐著市場需求的穩定成長。

到2025年,導引武器市佔率將達到42.5%。由於現代作戰場景中對精確目標捕獲能力的需求不斷成長,以及減少附帶損害的必要性,該領域正迅速擴張。先進的導航和目標捕獲技術提高了精度和作戰效能,促進了各國國防部隊的廣泛應用。智慧武器系統的持續改進也進一步加速了該領域的成長。

到2025年,北美彈藥市佔率將達到38.5%。該地區擁有高度發展的國防生態系統,這得益於強大的研發能力和政府對軍事現代化項目的持續投入。對維持戰略防禦優勢的持續重視以及主要國防製造商的存在,正在推動技術進步和先進彈藥系統的大規模採購。

洛克希德馬丁公司、雷神技術公司、英國航空航太系統公司、通用動力公司、萊茵金屬公司、諾斯羅普格魯曼公司和韓華公司是彈藥行業的主要企業。彈藥市場的企業正致力於先進產品研發、擴大產能並爭取國防契約,以鞏固其市場地位。製造商正大力投資精確導引技術和智慧彈藥系統,以滿足現代戰爭中對精度和作戰效率日益成長的需求。與國防和政府機構建立戰略夥伴關係有助於企業獲得長期供應合約。企業還透過自動化和先進製造流程來增強產能,從而提高產量並縮短前置作業時間。隨著對研發投入的不斷增加,輕量化、高性能特種彈藥領域的創新正在蓬勃發展。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 日益關注國防安全保障和執法機關現代化

- 恐怖活動和跨境衝突加劇

- 運動射擊和狩獵越來越受歡迎。

- 增加軍費預算和國防費用

- 越來越重視彈藥現代化和精確導引系統。

- 產業潛在風險與挑戰

- 供應鏈中斷與原物料價格波動

- 嚴格的法規和出口管制

- 市場機遇

- 新興國家對國防和民用應用的需求日益成長

- 輕質環保彈藥的技術進步

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 國防預算分析

- 全球國防費用趨勢

- 區域國防預算分配

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 貿易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響(基於初步研究)

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 生產能力和生產趨勢(基於初步調查)

- 各地區及主要生產商的產能

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按收入、地區和創新能力分類的層級定位矩陣。

第5章 市場估計與預測:依口徑分類,2022-2035年

- 小口徑彈藥(小於20毫米)

- 步槍和機槍彈藥

- 手槍子彈

- 狙擊彈藥

- 霰彈槍彈藥

- 其他

- 中口徑彈藥(20毫米至100毫米)

- 機槍彈

- 可發射手榴彈

- 大口徑彈藥(100毫米或以上)

- 砲彈

- 坦克彈藥

- 迫擊砲彈

- 海軍砲彈

- 其他

第6章 市場估算與預測:依產品類型分類,2022-2035年

- 子彈

- 全金屬外殼(FMJ)

- 穿甲彈(AP)

- 空心彈

- 其他

- 砲彈

- 高爆藥(HE)

- 耀斑

- 其他

- 手榴彈

- 碎片手榴彈

- 煙霧彈

- 眩暈手榴彈

- 迫擊砲彈

- 空中炸彈

- 彈頭

- 其他

第7章 市場估計與預測:歸納法,2022-2035年

- 飛彈

- GPS導引飛彈

- 雷射導引飛彈

- 慣性導航系統

- 非導引飛彈

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 軍隊

- 軍隊

- 海軍

- 空軍

- 海軍陸戰隊/特種作戰部隊

- 執法機關和國防安全保障

- 國家警察

- 邊境和海岸警衛隊

- 其他

- 私人的

- 狩獵和運動

- 自衛

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- 世界玩家

- BAE Systems PLC

- Northrop Grumman Corporation

- General Dynamics Corporation

- Rheinmetall AG

- Hanwha Corporation

- Lockheed Martin Corporation

- Raytheon Technologies Corporation

- 該地區頂尖公司

- Nammo AS

- FN Helstar(歐洲)

- Singapore Technologies Engineering Ltd

- Denel SOC Ltd

- CBC Global Ammunition

- 新興企業

- AMMO, Inc.

- Hornady Manufacturing, Inc.

- Nosler Inc.

- Fiocchi Munizioni SpA

- Prvi Partizan AD

The Global Ammunition Market was valued at USD 16.7 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 26.7 billion by 2035.

Market growth is supported by rising defense budgets across multiple countries as governments focus on strengthening military readiness, enhancing border protection, and addressing rising geopolitical tensions. Increased procurement of advanced defense systems and continuous modernization of armed forces are also driving sustained ammunition demand. Alongside military applications, civilian demand is expanding due to the growing popularity of recreational shooting and hunting activities, particularly in North America and parts of Europe, which is contributing to consistent consumption levels. The development of organized shooting ranges and competitive shooting events is further reinforcing civilian demand streams. Rising emphasis on homeland security and law enforcement modernization is another key factor supporting market expansion, as governments are equipping security forces with advanced firearms and maintaining steady ammunition stockpiles for operational and training requirements. Rapid urbanization and evolving security challenges in emerging economies are further strengthening procurement cycles. Overall, ammunition demand remains stable due to its dual reliance on defense preparedness and civilian usage patterns, ensuring long-term market resilience.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16.7 Billion |

| Forecast Value | $26.7 Billion |

| CAGR | 4.9% |

The medium caliber ammunition segment accounted for 29.4% share in 2025. Growth in this segment is driven by increasing adoption across military and law enforcement applications, where it is widely used in armored systems, naval platforms, and air defense operations. Its balance of firepower and operational efficiency supports its continued integration into modernized defense systems, reinforcing steady demand growth.

The guided ammunition segment held a 42.5% share in 2025. This segment is expanding rapidly due to rising demand for precision targeting capabilities and reduced collateral impact in modern combat scenarios. Advanced navigation and targeting technologies are enhancing accuracy and operational effectiveness, supporting increased adoption across defense forces. Ongoing improvements in intelligent weapon systems are further accelerating segment expansion.

North America Ammunition Market accounted for 38.5% share in 2025. The region represents a highly developed defense ecosystem supported by strong research and development capabilities and consistent government investments in military modernization programs. Continuous focus on maintaining strategic defense superiority and the presence of major defense manufacturers are driving technological advancements and large-scale procurement of advanced ammunition systems.

Lockheed Martin Corporation, Raytheon Technologies Corporation, BAE Systems PLC, General Dynamics Corporation, Rheinmetall AG, Northrop Grumman Corporation, and Hanwha Corporation are among the leading companies operating in the ammunition industry. Companies in the Ammunition Market focus on advanced product development, capacity expansion, and defense contract acquisitions to strengthen their market position. Manufacturers are investing heavily in precision-guided technologies and smart ammunition systems to meet the growing demand for accuracy and operational efficiency in modern warfare. Strategic partnerships with defense agencies and government bodies help firms secure long-term supply agreements. Companies are also enhancing production capabilities through automation and advanced manufacturing processes to improve output and reduce lead times. Increasing emphasis on research and development is driving innovation in lightweight, high-performance, and specialized ammunition types.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Caliber trends

- 2.2.2 Product type trends

- 2.2.3 Guidance mechanism trends

- 2.2.4 End-user application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing focus on homeland security and law enforcement modernization

- 3.2.1.2 Rising terrorism activities and cross border conflicts.

- 3.2.1.3 Growing popularity of sport-shooting and hunting.

- 3.2.1.4 Rising military budgets and defense expenditures.

- 3.2.1.5 Increasing focus on ammunition modernization and precision-guided systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain disruptions and raw material price volatility

- 3.2.2.2 Stringent regulations and export controls

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand from emerging economies for defense and civilian applications

- 3.2.3.2 Technological advancements in lightweight and eco-friendly ammunition

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Defense budget analysis

- 3.9 Global defense spending trends

- 3.10 Regional defense budget allocation

- 3.10.1 North America

- 3.10.2 Europe

- 3.10.3 Asia Pacific

- 3.10.4 Middle East and Africa

- 3.10.5 Latin America

- 3.11 Pricing Analysis (Driven by Primary Research)

- 3.11.1 Historical Price Trend Analysis

- 3.11.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.12 Trade Data Analysis (Based on Paid Database)

- 3.12.1 Import/Export Volume & Value Trends

- 3.12.2 Key Trade Corridors & Tariff Impact

- 3.13 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.13.1 AI-Driven Disruption of Existing Business Models

- 3.13.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.13.3 Risks, Limitations & Regulatory Considerations

- 3.14 Capacity & Production Landscape (Driven by Primary Research)

- 3.14.1 Production Capacity by Region & Key Producer

- 3.14.2 Capacity Utilization Rates & Expansion Pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia-Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By Region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Caliber, 2022-2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Small caliber ammunition (below 20mm)

- 5.2.1 Rifle & machine gun rounds

- 5.2.2 Handgun rounds

- 5.2.3 Sniper rounds

- 5.2.4 Shotgun rounds

- 5.2.5 Others

- 5.3 Medium caliber ammunition (20mm to 100mm)

- 5.3.1 Autocannon rounds

- 5.3.2 Launched grenades

- 5.4 Large caliber ammunition (above 100mm)

- 5.4.1 Artillery ammunition

- 5.4.2 Tank ammunition

- 5.4.3 Mortar ammunition

- 5.4.4 Naval ammunition

- 5.4.5 Others

Chapter 6 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Bullets

- 6.2.1 Full metal jacket (FMJ)

- 6.2.2 Armor piercing (AP)

- 6.2.3 Hollow point

- 6.2.4 Others

- 6.3 Artillery shells

- 6.3.1 High explosive (HE)

- 6.3.2 Illumination rounds

- 6.3.3 Others

- 6.4 Grenades

- 6.4.1 Fragmentation grenades

- 6.4.2 Smoke grenades

- 6.4.3 Stun grenades

- 6.5 Mortar rounds

- 6.6 Aerial bombs

- 6.7 Warheads

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Guidance Mechanism, 2022-2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Guided ammunition

- 7.2.1 GPS-guided projectiles

- 7.2.2 Laser-guided munitions

- 7.2.3 Inertial navigation systems

- 7.3 Non-guided ammunition

Chapter 8 Market Estimates and Forecast, By End User, 2022-2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Military

- 8.2.1 Army

- 8.2.2 Navy

- 8.2.3 Air force

- 8.2.4 Marines / special operations forces

- 8.3 Law enforcement & homeland security

- 8.3.1 National police force

- 8.3.2 Border & coast protection units

- 8.3.3 Others

- 8.4 Civilian

- 8.4.1 Hunting & sports

- 8.4.2 Personal defense

- 8.4.3 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 BAE Systems PLC

- 10.1.2 Northrop Grumman Corporation

- 10.1.3 General Dynamics Corporation

- 10.1.4 Rheinmetall AG

- 10.1.5 Hanwha Corporation

- 10.1.6 Lockheed Martin Corporation

- 10.1.7 Raytheon Technologies Corporation

- 10.2 Regional Champions

- 10.2.1 Nammo AS

- 10.2.2 FN Herstal (Europe)

- 10.2.3 Singapore Technologies Engineering Ltd

- 10.2.4 Denel SOC Ltd

- 10.2.5 CBC Global Ammunition

- 10.3 Emerging Players

- 10.3.1 AMMO, Inc.

- 10.3.2 Hornady Manufacturing, Inc.

- 10.3.3 Nosler Inc.

- 10.3.4 Fiocchi Munizioni S.p.A.

- 10.3.5 Prvi Partizan A.D.