|

市場調查報告書

商品編碼

2038480

無線耳機市場機會、成長要素、產業趨勢分析及2026-2035年預測Wireless Earphone Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

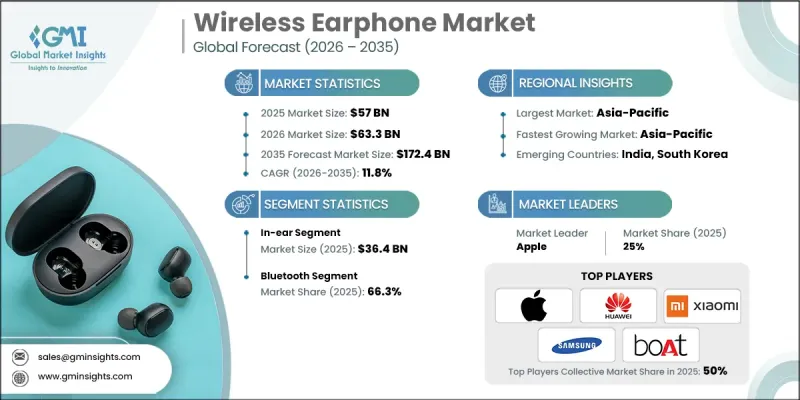

2025 年全球無線耳機市場價值 570 億美元,預計到 2035 年將達到 1,724 億美元,年複合成長率為 11.8%。

市場發展勢頭受消費者日常偏好,他們優先考慮易用性、便攜性和擺脫實體連結的自由。隨著攜帶式電子設備日益融入日常生活,無線耳機逐漸被視為必備配件。無線連接和音訊性能的不斷提升,提高了設備間的兼容性,並帶來更穩定的聆聽體驗。工作方式和生活方式的改變也影響市場需求,使用者希望耳機能同時滿足商務溝通、娛樂和自我表達等各種需求。受健身趨勢和靈活辦公環境的廣泛影響,消費者對耳機的耐用性、舒適性和沈浸式音效的期望也在穩步提高。同時,市場仍以創新主導,各大品牌不斷投資研發更智慧的功能,以滿足不斷變化的用戶需求。智慧軟體功能和新型聆聽技術的融合,顯示無線耳機正在從單純的音訊工具演變為多功能設備。持續的設計創新和快速的技術迭代,不斷鞏固全球市場的強勁成長潛力。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 570億美元 |

| 預測金額 | 1724億美元 |

| 複合年成長率 | 11.8% |

至2025年,入耳式耳機市場規模將達364億美元。該細分市場之所以能保持領先地位,是因為其體積小巧、便於攜帶、適合長時間佩戴,並且即使在運動中也能提供穩固的貼合感。入耳式設計完美契合了消費者對輕便產品的偏好,使其能夠無縫融入積極、移動的生活方式。

2025年,藍牙市佔率達到66.3%,繼續保持主導地位。其強大的市場地位得益於與整體個人電子設備的兼容性、可靠的配對性能以及通訊範圍和功率效率的持續提升,使其成為無線音頻傳輸的首選方案。

美國無線耳機市場佔77%的佔有率,預計2025年市場規模將達到122億美元。市場成長的驅動力包括先進音訊解決方案的普及、智慧設備的高滲透率以及消費者對高品質聆聽體驗的投入意願。成熟的數位生態系統促進了新功能的快速普及以及與互聯技術的無縫整合。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 對攜帶式音訊設備的需求日益成長。

- 藍牙和降噪技術的進步

- 生活方式的改變和數位內容消費的擴展

- 產業潛在風險與挑戰

- 仿冒品增多

- 安全和駭客攻擊問題

- 機會

- 虛擬實境和高效能音訊應用的日益普及

- 線上零售通路的快速擴張

- 促進因素

- 成長潛力分析

- 關鍵市場趨勢與顛覆性因素

- 未來市場趨勢

- 風險分析及緩解措施

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按類型

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 波特五力分析

- PESTEL 分析

- 消費行為分析

- 購買模式

- 偏好分析

- 不同地區的消費行為差異

- 電子商務對購買決策的影響

- 交易資料分析(基於付費資料來源)

- 進出口量和進出口額趨勢(基於初步調查)

- 主要貿易走廊及關稅影響(基於初步調查)

- 跨境電子商務流分析

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 細分市場生成式人工智慧用例和實施藍圖

- 風險、限制和監管考量

- 生態系鎖定效應:三星Galaxy生態系與蘋果生態系的分析

- 分銷基礎設施和通路滲透狀況(基於初步調查)

- 按地區和業態(現代零售與傳統零售)分類的通路覆蓋率(基於初步調查)

- 最後一公里基礎設施的差異和新管道的變化(基於初步研究)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 貼耳式

- 入耳式

第6章 市場估算與預測:以連結方式分類,2022-2035年

- Bluetooth

- Wi-Fi

- NFC

第7章 市場估價與預測:依電池壽命分類,2022-2035年

- 最多 12 小時

- 12-24小時

- 超過24小時

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 音樂與娛樂

- 遊戲

- 健身與運動

- 其他

第9章 市場估計與預測:依價格分類,2022-2035年

- 低價位

- 中等的

- 高價位範圍

第10章 市場估價與預測:依最終用戶分類,2022-2035年

- 一般消費者

- 公司和組織

第11章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 離線

第12章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 土耳其

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第13章:公司簡介

- Anker

- Apple

- Beats

- boAt(Imagine Marketing)

- Bose

- Huawei

- JBL

- Noise

- Nothing

- OnePlus

- OPPO

- Realme

- Samsung

- Sony

- Xiaomi

The Global Wireless Earphone Market was valued at USD 57 billion in 2025 and is estimated to grow at a CAGR of 11.8% to reach USD 172.4 billion by 2035.

Market momentum is shaped by everyday consumer preferences that prioritize ease of use, mobility, and freedom from physical connections. As portable electronics become deeply embedded in daily routines, wireless earphones are increasingly viewed as an essential accessory. Continuous enhancements in wireless connectivity and audio performance are improving compatibility across devices and delivering more stable listening experiences. Shifts in work habits and lifestyle patterns are also influencing demand, with users seeking earphones that support professional communication, entertainment, and personal expression in a single product. Expectations around durability, comfort, and immersive sound have risen steadily, reflecting broader changes in fitness trends and flexible working environments. At the same time, the market remains innovation-driven, with brands investing in smarter functionalities that align with evolving user needs. The integration of intelligent software features and new listening technologies demonstrates how wireless earphones are evolving into multifunctional devices rather than simple audio tools. Ongoing design innovation and rapid technology cycles continue to reinforce strong growth potential across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $57 Billion |

| Forecast Value | $172.4 Billion |

| CAGR | 11.8% |

In 2025, the in-ear category accounted for USD 36.4 billion. This segment remains dominant due to its compact form, ease of transport, and suitability for extended wear, while also offering stability during movement. In-ear designs align well with consumer preferences for lightweight products that fit seamlessly into active and on-the-go lifestyles.

The bluetooth segment held 66.3% share in 2025, maintaining its lead as the most widely adopted wireless standard. Its strong presence is supported by universal compatibility across personal electronics, reliable pairing performance, and continued improvements in range and power efficiency, making it the preferred option for wireless audio transmission.

United States Wireless Earphone Market held 77% share, generating USD 12.2 billion in 2025. Market growth is supported by strong adoption of advanced audio solutions, high penetration of smart devices, and consumer willingness to invest in premium listening experiences. A mature digital ecosystem enables rapid acceptance of new features and seamless integration with connected technologies.

Key companies active in the Global Wireless Earphone Market include Samsung, Apple, Sony, Bose, Xiaomi, JBL (Harman/Samsung), Huawei, OPPO, Realme, Beats, Sennheiser, Jabra (GN Store Nord), Anker (Soundcore), boAt (Imagine Marketing), and Noise. Companies operating in the wireless earphone market are reinforcing their market position through continuous product innovation, brand differentiation, and ecosystem integration. Many players focus on improving sound quality, battery performance, and comfort while embedding intelligent software capabilities that enhance usability. Strategic pricing across multiple product tiers helps brands address both mass-market and premium consumers. Investment in design aesthetics and ergonomic research strengthens brand appeal and user loyalty. Firms are also expanding distribution through online platforms and partnerships to improve global reach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 By regional

- 2.2.2 By type

- 2.2.3 By connectivity

- 2.2.4 By battery life

- 2.2.5 By price

- 2.2.6 By application

- 2.2.7 By end user

- 2.2.8 By distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for portable and convenient audio devices

- 3.2.1.2 Advancements in bluetooth and noise-cancellation technologies

- 3.2.1.3 Lifestyle shifts and expansion of digital content consumption

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Rising prevalence of counterfeit products

- 3.2.2.2 Security and hacking concerns

- 3.2.3 Opportunities

- 3.2.3.1 Growing adoption of virtual reality and high-performance audio applications

- 3.2.3.2 Rapid expansion of online retail channels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and Disruptions

- 3.5 Future market trends

- 3.6 Risk and mitigation Analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By type

- 3.9 Regulatory landscape

- 3.9.1 North America

- 3.9.2 Europe

- 3.9.3 Asia-Pacific

- 3.9.4 Middle East and Africa

- 3.9.5 Latin America

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Consumer behaviour analysis

- 3.12.1 Purchasing patterns

- 3.12.2 Preference analysis

- 3.12.3 Regional variations in consumer behavior

- 3.12.4 Impact of e-commerce on buying decisions

- 3.13 Trade Data Analysis (Driven by paid data sources)

- 3.13.1 Import & Export Volume & Value Trends (Driven by Primary Research)

- 3.13.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.13.3 Cross-Border E-Commerce Flow Analysis

- 3.14 Impact of AI & Generative AI on the Market

- 3.14.1 AI-Driven Disruption of Existing Business Models

- 3.14.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.14.3 Risks, Limitations & Regulatory Considerations

- 3.14.4 Ecosystem Lock-In Effects: Samsung Galaxy vs Apple Ecosystem Analysis

- 3.15 Distribution Infrastructure & Channel Penetration Landscape (Driven by Primary Research)

- 3.15.1 Channel Coverage by Region & Format (Modern vs. Traditional Trade) (Driven by Primary Research)

- 3.15.2 Last-Mile Infrastructure Gaps & Emerging Channel Shifts (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022-2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 On-ear

- 5.3 In-ear

Chapter 6 Market Estimates & Forecast, By Connectivity, 2022-2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Bluetooth

- 6.3 Wi-Fi

- 6.4 NFC

Chapter 7 Market Estimates & Forecast, By Battery Life, 2022-2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Up to 12 hours

- 7.3 12 to 24 hours

- 7.4 Above 24 hours

Chapter 8 Market Estimates & Forecast, By Application, 2022-2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Music & entertainment

- 8.3 Gaming

- 8.4 Fitness & sports

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Price, 2022-2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Low

- 9.3 Medium

- 9.4 High

Chapter 10 Market Estimates & Forecast, By End User, 2022-2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Individual Consumers

- 10.3 Enterprise/Institutional

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Online

- 11.3 Offline

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Turkey

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 Japan

- 12.4.3 India

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Anker

- 13.2 Apple

- 13.3 Beats

- 13.4 boAt (Imagine Marketing)

- 13.5 Bose

- 13.6 Huawei

- 13.7 JBL

- 13.8 Noise

- 13.9 Nothing

- 13.10 OnePlus

- 13.11 OPPO

- 13.12 Realme

- 13.13 Samsung

- 13.14 Sony

- 13.15 Xiaomi

無線耳機市場:2026-2032年全球市場預測(依產品類型、連接方式、技術、應用、電池續航力、銷售管道及最終用戶分類)

無線耳機市場:2026-2032年全球市場預測(依產品類型、連接方式、技術、應用、電池續航力、銷售管道及最終用戶分類) 全球無線耳機市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球無線耳機市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 無線耳機市場規模、佔有率和成長分析(按產品類型、技術、價格分佈範圍、最終用戶、分銷管道和地區分類)—產業預測(2026-2033 年)

無線耳機市場規模、佔有率和成長分析(按產品類型、技術、價格分佈範圍、最終用戶、分銷管道和地區分類)—產業預測(2026-2033 年) 無線耳機市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、配銷通路、地區和競爭情況細分,2020-2030 年全球無線耳機市場規模(按技術、應用、最終用戶、區域範圍)預測(至 2025 年)

無線耳機市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、配銷通路、地區和競爭情況細分,2020-2030 年全球無線耳機市場規模(按技術、應用、最終用戶、區域範圍)預測(至 2025 年) 全球耳機市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)耳機的全球市場 - 全球產業分析,規模,佔有率,成長,趨勢,預測(2031年)

全球耳機市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)耳機的全球市場 - 全球產業分析,規模,佔有率,成長,趨勢,預測(2031年)