|

市場調查報告書

商品編碼

2038475

智慧冷藏庫市場機會、成長要素、產業趨勢分析及2026-2035年預測Smart Refrigerator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

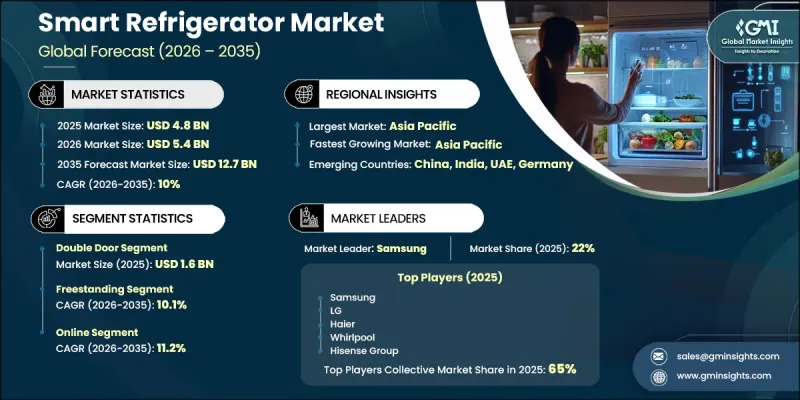

2025年全球智慧冷藏庫市場價值48億美元,預計到2035年將以10%的複合年成長率成長至127億美元。

智慧家庭生態系統的加速普及是推動該市場成長的關鍵因素之一。隨著越來越多的家庭採用智慧音箱、恆溫器和照明系統等連網設備,消費者對能夠提升便利性和能源效率的智慧家電的興趣日益濃厚。具備Wi-Fi連接、應用程式控制和語音控制功能的智慧冷藏庫,使用戶能夠輕鬆管理食物儲存、控制能源消耗並遠端監控使用情況。這些產品與連網家庭網路的無縫整合,實現了自動化、個人化和節能的家居管理。這種向互聯生活演進的趨勢,正在推動智慧廚房電器的需求成長,尤其是在精通科技的消費者和年輕一代。此外,價格親民的物聯網組件的普及和網路存取的增加,使得即使是中端家電也能輕鬆擁有先進的功能。設備間通用通訊標準的引進,進一步提升了不同品牌之間的相容性,並加速了智慧家電在全球市場的普及。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 48億美元 |

| 預測市場規模 | 127億美元 |

| 複合年成長率 | 10% |

到2025年,雙門冰箱市場規模將達到16億美元。這類冰箱因其大容量儲存、易於整理和人性化設計而日益受到歡迎。其設計便於消費者有效率地分別存放冷藏和冷凍食品,並能滿足各種小規模大規模的需求。最新的雙門冰箱配備了濕度控制、可自訂層架和食物追蹤系統等智慧功能。借助人工智慧技術,這些冰箱可以監測食物新鮮度、提供儲存提案建議並減少食物浪費,從而滿足消費者對便利性和永續性的需求。

到2025年,獨立式智慧冰箱將佔據92%的市場。獨立式智慧冷藏庫的柔軟性使其成為住宅和商業空間的理想選擇,因為在這些場所,移動和安裝的便利性至關重要。由於無需對建築結構進行改造或安裝嵌入式櫥櫃,它們不僅經濟實惠,而且能夠適應各種戶型,包括出租住宅和都市區公寓。憑藉其易於安裝和便攜性的特點,它們仍然是比嵌入式冰箱更受歡迎的選擇,尤其是在快速變化的都市區生活環境中。

美國智慧冷藏庫市場佔80%的佔有率,預計到2025年將達到12億美元。憑藉互聯技術、節能解決方案和以永續性為導向的產品設計的高普及率,美國在智慧家庭設備創新領域持續保持領先地位。精通數位技術的年輕消費群體是市場的主要驅動力,成熟的零售生態系統也為市場提供了支持,提供了豐富的品牌和先進的功能。人們對能源聯網生活的日益關注,鞏固了美國作為北美智慧冷藏庫領先市場的地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按球員類型分類的定價策略(高階/超值/成本加成)

- 進口價格與國內價格之間的差異

- 法律規範

- 貿易資料分析(HS編碼8418)

- 進出口量及進口額趨勢

- 主要貿易走廊及關稅的影響

- 主要出口國

- 主要進口國

- 貿易法規和關稅分類

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧正在改變傳統的經營模式。

- 按客戶群分類的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 整合人工智慧驅動的智慧家庭生態系統

- 波特五力分析

- PESTEL 分析

- 消費行為分析

- 購買模式

- 偏好分析

- 消費行為的區域差異

- 電子商務對購買決策的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 單門

- 雙門

- 法式門

- 門中門

- 並排

第6章 市場估價與預測:依安裝類型分類,2022-2035年

- 檯面

- 固定式

第7章 市場估計與預測:依產能分類,2022-2035年

- 小型(10-19立方英尺)

- 中型(20-29立方英尺)

- 大型(30立方英尺或以上)

第8章 市場估計與預測:依價格分類,2022-2035年

- 低的

- 中等的

- 高的

第9章 市場估價與預測:依最終用戶分類,2022-2035年

- 住宅

- 商業的

- 飯店和餐廳

- 食品和飲料零售

- 藥局

- 衛生保健

- 其他(旅舍、設施等)

第10章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 企業網站

- 離線

- 超級市場/大賣場

- 專賣店

- 其他(例如獨立經營零售商店)

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 全球主要公司

- Bosch

- Electrolux

- Haier

- Hisense

- LG Electronics

- Midea

- Panasonic

- Samsung Electronics

- Whirlpool

- 按地區分類的主要公司

- Godrej Appliances

- Hitachi Appliances

- Sharp Corporation

- TCL Corporation

- Vestel

- Voltas Beko

- Emerging and Specialized Players

- Bertazzoni

- Changhong

- Gram Commercial

- Gree Electric Appliances

- Skyworth

- Viking Range

The Global Smart Refrigerator Market was valued at USD 4.8 billion in 2025 and is estimated to grow at a CAGR of 10% to reach USD 12.7 billion by 2035.

The accelerating adoption of smart home ecosystems is one of the leading factors driving this market's growth. With more homes integrating connected devices such as smart speakers, thermostats, and lighting systems, consumers are increasingly drawn to smart appliances that enhance convenience and energy efficiency. Smart refrigerators, equipped with Wi-Fi connectivity, app-based controls, and voice-command functionality, allow users to manage food storage, energy consumption, and remote monitoring with ease. Their seamless integration into connected home networks enables automated, personalized, and energy-efficient household management. This evolution toward interconnected living is propelling the demand for intelligent kitchen appliances, especially among tech-savvy and younger consumers. Additionally, the rollout of affordable IoT components and wider internet accessibility has made advanced features more attainable, even in mid-range appliances. The introduction of universal communication standards across devices has further enhanced compatibility among different brands, encouraging adoption across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.8 Billion |

| Forecast Value | $12.7 Billion |

| CAGR | 10% |

In 2025, the double-door segment generated USD 1.6 billion. These models are increasingly preferred for their large storage capacity, improved organization, and user-friendly features. Their design allows consumers to separate and efficiently manage refrigerated and frozen goods, catering to both small and large households. Modern double-door models are enhanced with smart features such as humidity control, customizable shelving, and food tracking systems. Through AI-enabled functionalities, these appliances can monitor freshness, suggest storage arrangements, and reduce food wastage, aligning with consumer preferences for convenience and sustainability.

The freestanding segment held a 92% share in 2025. The flexibility of freestanding smart refrigerators makes them an ideal option for residential and commercial spaces where mobility and easy installation are key factors. They do not require structural modifications or built-in cabinetry, which makes them cost-effective and adaptable to diverse layouts, including rental homes and urban apartments. Their convenience in placement and portability continues to make them the preferred choice over built-in alternatives, especially in dynamic urban living environments.

U.S. Smart Refrigerator Market held 80% share, generating USD 1.2 billion in 2025. The country remains at the forefront of smart appliance innovation due to the high adoption of connected technologies, energy-efficient solutions, and sustainability-driven product design. A digitally aware and youthful consumer base is propelling the market forward, supported by a mature retail ecosystem that offers a wide selection of brands and advanced features. The increasing emphasis on energy conservation and connected living has positioned the U.S. as a major market for smart refrigerators in North America.

Key players operating in the Global Smart Refrigerator Industry include Samsung Electronics, LG Electronics, Whirlpool, Bosch Home Appliances, Haier Smart Home, GE Appliances, Panasonic, Siemens Home Appliances, Sharp Corporation, Fisher & Paykel Appliances, Hisense Group, Sony, Electrolux, Miele & Cie., and Beko. Companies in the Smart Refrigerator Market are strengthening their presence through innovation, connectivity, and strategic collaborations. Many leading manufacturers are investing heavily in artificial intelligence, IoT integration, and machine learning to improve user interaction, energy management, and predictive maintenance. Expanding partnerships with smart home technology providers ensures compatibility across ecosystems and enhances the consumer experience. Firms are also focusing on sustainable design, developing energy-efficient models that comply with global energy standards.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Installation type

- 2.2.4 Capacity

- 2.2.5 Price

- 2.2.6 End user

- 2.2.7 Distribution channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Historical price trend analysis

- 3.6.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.6.3 Import vs domestic price differential

- 3.7 Regulatory framework

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 Latin America

- 3.7.5 Middle East and Africa

- 3.8 Trade data analysis (HS Code 8418)

- 3.8.1 Import/Export Volume & Value Trends

- 3.8.2 Key Trade Corridors & Tariff Impact

- 3.8.3 Top Exporting Countries

- 3.8.4 Top Importing Countries

- 3.8.5 Trade Regulations & Customs Classification

- 3.9 Impact of AI & generative ai on the market

- 3.9.1 AI-driven disruption of traditional business models

- 3.9.2 GenAI use cases & adoption roadmap by customer segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.9.4 AI-enabled smart home ecosystem integration

- 3.10 Porter's five forces analysis

- 3.11 PESTEL analysis

- 3.12 Consumer behavior analysis

- 3.12.1 Purchasing patterns

- 3.12.2 Preference analysis

- 3.12.3 Regional variations in consumer behavior

- 3.12.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Single door

- 5.3 Double door

- 5.4 French door

- 5.5 Door-in-door

- 5.6 Side by side

Chapter 6 Market Estimates & Forecast, By Installation Type, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Countertop

- 6.3 Freestanding

Chapter 7 Market Estimates & Forecast, By Capacity, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Small (10-19 cubic feet)

- 7.3 Medium (20-29 cubic feet)

- 7.4 Large (30+ cubic feet)

Chapter 8 Market Estimates & Forecast, By Price, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates & Forecast, By End User, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.3.1 Hotels & restaurants

- 9.3.2 Food & beverage retail

- 9.3.3 Pharmacy

- 9.3.4 Healthcare

- 9.3.5 Others (hostel, institution, etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce

- 10.2.2 Company websites

- 10.3 Offline

- 10.3.1 Supermarkets/hypermarket

- 10.3.2 Specialty retail stores

- 10.3.3 Others (independent retailer etc.)

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Top Global Players

- 12.1.1 Bosch

- 12.1.2 Electrolux

- 12.1.3 Haier

- 12.1.4 Hisense

- 12.1.5 LG Electronics

- 12.1.6 Midea

- 12.1.7 Panasonic

- 12.1.8 Samsung Electronics

- 12.1.9 Whirlpool

- 12.2 Regional Key Players

- 12.2.1 Godrej Appliances

- 12.2.2 Hitachi Appliances

- 12.2.3 Sharp Corporation

- 12.2.4 TCL Corporation

- 12.2.5 Vestel

- 12.2.6 Voltas Beko

- 12.3 Emerging and Specialized Players

- 12.3.1 Bertazzoni

- 12.3.2 Changhong

- 12.3.3 Gram Commercial

- 12.3.4 Gree Electric Appliances

- 12.3.5 Skyworth

- 12.3.6 Viking Range

智慧家庭設備市場-2026-2032年全球市場預測智慧冷藏庫市場:2026-2032年全球市場預測(按產品類型、組件、技術、分銷管道和最終用戶分類)

智慧家庭設備市場-2026-2032年全球市場預測智慧冷藏庫市場:2026-2032年全球市場預測(按產品類型、組件、技術、分銷管道和最終用戶分類) 智慧家庭設備市場規模、佔有率和成長分析:按產品類型、連接技術、應用、銷售管道、最終用戶和地區分類-2026-2033年產業預測

智慧家庭設備市場規模、佔有率和成長分析:按產品類型、連接技術、應用、銷售管道、最終用戶和地區分類-2026-2033年產業預測 消費機器人和智慧家居設備

消費機器人和智慧家居設備 智慧家庭設備市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、形式、最終用戶及功能分類

智慧家庭設備市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、形式、最終用戶及功能分類 全球智慧冷藏庫市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球智慧冷藏庫市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球智慧冷藏庫市場報告

2026年全球智慧冷藏庫市場報告 智慧家居設備市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、最終用戶、銷售管道、地區和競爭格局分類,2021-2031年

智慧家居設備市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、最終用戶、銷售管道、地區和競爭格局分類,2021-2031年 智慧冷藏庫市場規模、佔有率和成長分析(按門類型、最終用途、分銷管道和地區分類)—產業預測(2026-2033 年)

智慧冷藏庫市場規模、佔有率和成長分析(按門類型、最終用途、分銷管道和地區分類)—產業預測(2026-2033 年) 智慧冷藏庫:全球市場佔有率和排名、總銷售額和需求預測(2025-2031 年)

智慧冷藏庫:全球市場佔有率和排名、總銷售額和需求預測(2025-2031 年)