|

市場調查報告書

商品編碼

2038456

擬除蟲菊酯市場機會、成長要素、產業趨勢分析及2026-2035年預測Pyrethroids Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

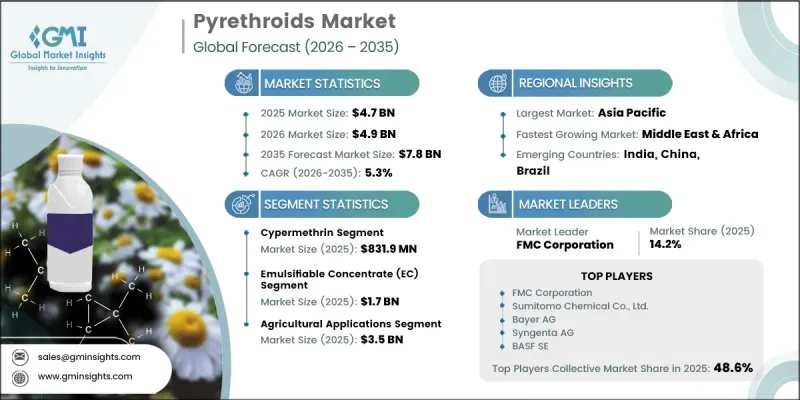

預計到 2025 年,全球擬除蟲菊酯市場價值將達到 47 億美元,並以 5.3% 的複合年成長率成長,到 2035 年將達到 78 億美元。

擬除蟲菊酯類殺蟲劑是透過化學修飾從菊花中提取的天然除蟲菊酯而開發的合成殺蟲劑化合物。這些化合物透過靶向並抑制昆蟲神經系統的功能,展現出優異的光穩定性和強效的殺蟲效果。其主要特點包括快速擊倒、廣譜害蟲防治、抗環境分解以及適用於室內外環境。由於其高效且對哺乳動物毒性相對較低,擬除蟲菊酯類殺蟲劑被廣泛應用於農業、公共衛生計畫和住宅害蟲防治。其在不同環境下的多功能性和穩定性也促使其擴大被納入綜合蟲害管理(IPM)策略。生產技術的不斷進步,包括改進的合成途徑、立體化學控制和增強的製劑技術,正在提升產品的功效和安全性。這些創新使生產商能夠精確控制產品的功效、穩定性和環境影響,從而滿足全球多個終端用戶產業日益成長的需求。這一前景反映了擬除蟲菊酯類殺蟲劑在全球已開發市場和新興市場的持續應用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 47億美元 |

| 預測市場規模 | 78億美元 |

| 複合年成長率 | 5.3% |

預計到2025年,Cypermethrin市場規模將達到8.319億美元。其市場主導地位得益於農業和建築害蟲防治領域的強勁需求,而其價格適中和廣泛的功效也使其高效性得以鞏固。該化合物在多種害蟲防治應用中繼續發揮核心作用,使其在多個應用領域的商業性重要性日益提升。同時,新型擬除蟲菊酯化合物的研發正在拓展其在特定領域的應用前景,這些領域需要更高的光穩定性和更持久的藥效,從而進一步拓寬了此類殺蟲劑的應用範圍。

預計到2025年,乳化濃縮劑(EC)製劑市場規模將達17億美元。該細分市場持續成長,主要得益於其易於操作、噴灑覆蓋率高以及活性成分供應高效等優勢。農民越來越傾向於選擇可與現有噴灑設備無縫整合的可濕性粉劑,這推動了市場需求的持續成長。乳化濃縮劑製劑的便利性、相容性和操作效率是其在病蟲害防治領域廣泛應用的關鍵因素。

預計北美擬除蟲菊酯市場規模將從2025年的13億美元成長到2035年的22億美元。這一區域成長主要得益於農業對高效作物保護解決方案的強勁需求以及綜合蟲害管理(IPM)實踐的廣泛應用。此外,先進配方技術和系統性抗性管理方案的日益普及也進一步推動了市場擴張,這些技術在提高長期蟲害防治效果的同時,也能確保產品在不同應用環境下的可靠性。

FMC公司、先正達公司、拜耳公司、BASF公司、住友化學株式會社、UPL有限公司、ADAMA農業解決方案有限公司、江蘇揚農化工有限公司、賀蘭巴實業有限公司、Megmani Organics有限公司、Garuda Chemicals 有限公司、Tagros Chemicals India Private Limited、南南紅日市有限公司、Sinoharvest Corporation、Sinoharvest Corporation 有限公司的主要市場。這些企業致力於透過不斷創新配方技術和提高活性成分的功效來鞏固其市場地位。每家公司都在研發方面投入巨資,以提高產品穩定性、增強害蟲抗藥性管理能力並拓展應用領域。策略聯盟和夥伴關係關係,以及向高成長農業地區進行地理擴張,也是提高市場滲透率的優先事項。此外,製造商也正在採用先進的合成技術和最佳化的生產流程,以提高成本效益和產品均一性。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- Bifenthrin

- Deltamethrin

- Permethrin

- Cypermethrin

- Cyfluthrin

- 蘭姆達西哈洛特林

- 其他

第6章 市場估算與預測:依製劑類型分類,2022-2035年

- 濃縮液(EC)

- 可濕性粉劑(WP)

- 可濕性顆粒劑(WG)

- 顆粒劑(GR)

- 超低容量噴塗(ULV)

- 其他

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 農業用途

- 糧食

- 油籽/豆類

- 水果和蔬菜

- 其他

- 非農業用途

- 公共衛生

- 住宅

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- FMC Corporation

- Sumitomo Chemical Co., Ltd.

- Bayer AG

- Syngenta AG

- BASF SE

- ADAMA Agricultural Solutions Ltd.

- UPL Limited

- Jiangsu Yangnong Chemical Co., Ltd.

- Nanjing Red Sun Co., Ltd.

- Tagros Chemicals India Pvt. Ltd.

- Heranba Industries Limited

- Gharda Chemicals Limited

- Meghmani Organics Ltd.

- SinoHarvest Corp.

- Zhejiang Xinan Chemical Industrial Group

The Global Pyrethroids Market was valued at USD 4.7 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 7.8 billion in 2035.

Pyrethroids are synthetic insecticidal compounds developed through chemical modification of naturally occurring pyrethrins derived from chrysanthemum flowers. These compounds are engineered to provide enhanced photostability and strong insecticidal performance by targeting and disrupting the nervous systems of insects. Their key properties include rapid knockdown action, broad-spectrum pest control capability, resistance to environmental degradation, and suitability for both indoor and outdoor applications. Pyrethroids are widely utilized across agriculture, public health programs, and residential pest management due to their effectiveness and relatively low toxicity toward mammals. They are also increasingly incorporated into integrated pest management strategies because of their versatility and consistent performance across varied environments. Continuous advancements in production technologies, including improved synthesis routes, stereochemical control, and enhanced formulation techniques, have strengthened product efficiency and safety profiles. These innovations enable manufacturers to achieve precise control over efficacy, stability, and environmental behavior, supporting expanding global demand across multiple end-use industries. This outlook reflects sustained adoption across both developed and emerging markets globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.7 Billion |

| Forecast Value | $7.8 Billion |

| CAGR | 5.3% |

The cypermethrin segment reached USD 831.9 million in 2025. Its dominance is supported by strong demand in agricultural protection and structural pest control applications, where its affordability and wide-spectrum efficacy make it highly effective. The compound continues to play a central role in controlling a broad range of insect pests, reinforcing its commercial importance across multiple usage areas. At the same time, the development of newer pyrethroid variants is expanding opportunities in specialized segments that require improved photostability and longer residual performance, further widening the application scope of this class of insecticides.

The emulsifiable concentrate (EC) formulations segment generated USD 1.7 billion in 2025. This segment continues to gain traction due to its ease of handling, improved spray coverage, and efficient delivery of active ingredients. Farmers increasingly prefer water-dispersible solutions that integrate seamlessly with existing spraying equipment, supporting consistent demand growth. The convenience, compatibility, and operational efficiency of EC formulations are key factors driving their widespread adoption across pest control applications.

North America Pyrethroids Market is projected to grow from USD 1.3 billion in 2025 to USD 2.2 billion in 2035. Growth in this region is primarily driven by strong agricultural demand for effective crop protection solutions and the widespread implementation of integrated pest management practices. Market expansion is further supported by increasing adoption of advanced formulation technologies and structured resistance management programs that enhance long-term pest control effectiveness while maintaining product reliability across diverse application settings.

FMC Corporation, Syngenta AG, Bayer AG, BASF SE, Sumitomo Chemical Co., Ltd., UPL Limited, ADAMA Agricultural Solutions Ltd., Jiangsu Yangnong Chemical Co., Ltd., Heranba Industries Limited, Meghmani Organics Ltd., Gharda Chemicals Limited, Tagros Chemicals India Pvt. Ltd., Nanjing Red Sun Co., Ltd., SinoHarvest Corp., and Zhejiang Xinan Chemical Industrial Group are among the leading companies operating in the pyrethroids market. Companies operating in the pyrethroids industry are focusing on strengthening their market position through continuous innovation in formulation technologies and active ingredient efficiency. They are investing heavily in research and development to enhance product stability, improve pest resistance management, and expand application versatility. Strategic collaborations, partnerships, and geographic expansion into high-growth agricultural regions are also being prioritized to increase market penetration. Manufacturers are further adopting advanced synthesis techniques and optimized production processes to improve cost efficiency and product consistency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Formulation Type

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Million Litters)

- 5.1 Key trends

- 5.2 Bifenthrin

- 5.3 Deltamethrin

- 5.4 Permethrin

- 5.5 Cypermethrin

- 5.6 Cyfluthrin

- 5.7 Lambda-Cyhalothrin

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Formulation Type, 2022-2035 (USD Billion) (Million Litters)

- 6.1 Key trends

- 6.2 Emulsifiable Concentrate (EC)

- 6.3 Wettable Powder (WP)

- 6.4 Water-Dispersible Granules (WG)

- 6.5 Granular (GR)

- 6.6 Ultra-Low Volume (ULV)

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Million Litters)

- 7.1 Key trends

- 7.2 Agricultural Applications

- 7.2.1 Cereals & Grains

- 7.2.2 Oilseeds & Pulses

- 7.2.3 Fruits & Vegetables

- 7.2.4 Others

- 7.3 Non-Agricultural Applications

- 7.3.1 Public Health

- 7.3.2 Residential

- 7.3.3 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 FMC Corporation

- 9.2 Sumitomo Chemical Co., Ltd.

- 9.3 Bayer AG

- 9.4 Syngenta AG

- 9.5 BASF SE

- 9.6 ADAMA Agricultural Solutions Ltd.

- 9.7 UPL Limited

- 9.8 Jiangsu Yangnong Chemical Co., Ltd.

- 9.9 Nanjing Red Sun Co., Ltd.

- 9.10 Tagros Chemicals India Pvt. Ltd.

- 9.11 Heranba Industries Limited

- 9.12 Gharda Chemicals Limited

- 9.13 Meghmani Organics Ltd.

- 9.14 SinoHarvest Corp.

- 9.15 Zhejiang Xinan Chemical Industrial Group

擬除蟲菊酯市場:全球市場預測,2026-2032年

擬除蟲菊酯市場:全球市場預測,2026-2032年 Permethrin市場規模、佔有率和成長分析:按等級、劑型、應用和地區分類-2026-2033年產業預測

Permethrin市場規模、佔有率和成長分析:按等級、劑型、應用和地區分類-2026-2033年產業預測 擬除蟲菊酯市場報告:按產品類型、作物類型、害蟲類型和地區分類(2026-2034 年)

擬除蟲菊酯市場報告:按產品類型、作物類型、害蟲類型和地區分類(2026-2034 年) 2026年全球擬除蟲菊酯類殺蟲劑市場報告合成擬除蟲菊酯類殺蟲劑市場按類型、施用方式、應用及通路分類,全球預測(2026-2032年)按劑型、作物類型、應用、最終用戶和銷售管道的Deltamethrin市場—2026-2032年全球預測

2026年全球擬除蟲菊酯類殺蟲劑市場報告合成擬除蟲菊酯類殺蟲劑市場按類型、施用方式、應用及通路分類,全球預測(2026-2032年)按劑型、作物類型、應用、最終用戶和銷售管道的Deltamethrin市場—2026-2032年全球預測 擬除蟲菊酯市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、作物類型、地區和競爭格局分類,2020-2030年預測

擬除蟲菊酯市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、作物類型、地區和競爭格局分類,2020-2030年預測 氯菊酯市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

氯菊酯市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 擬除蟲菊酯市場按類型、用途和地區分類

擬除蟲菊酯市場按類型、用途和地區分類