|

市場調查報告書

商品編碼

2038430

全自動咖啡機市場機會、成長要素、產業趨勢分析及2026-2035年預測Automatic Coffee Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

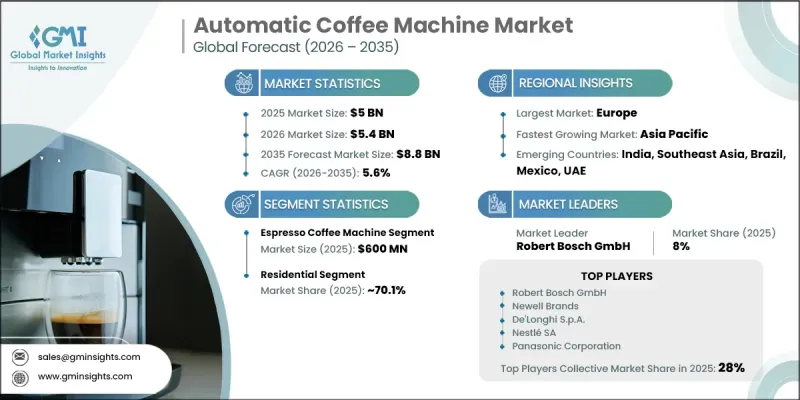

2025年全球全自動咖啡機市場價值50億美元,預計2035年將以5.6%的複合年成長率成長至88億美元。

隨著全球咖啡消費量持續成長,市場呈現穩定成長態勢,咖啡正成為已開發國家和新興國家日常生活中不可或缺的一部分。這種持續的消費趨勢推動了家用和商用用戶對自動咖啡機的青睞,他們重視咖啡品質的穩定性、速度和萃取精度。咖啡不再只是被視為一種飲品,而逐漸成為一種個人化的生活方式產品,因此,能夠在家中和職場提供咖啡館品質咖啡的自動沖泡系統需求日益成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 50億美元 |

| 預計金額 | 88億美元 |

| 複合年成長率 | 5.6% |

隨著消費者尋求既能簡化沖泡流程又能保持高品質風味的解決方案,他們對便利型家用電器的日益偏好進一步加速了市場擴張。全自動咖啡機憑藉其簡化的沖泡流程而廣受歡迎,這得益於其先進的功能,例如可編程功能、內置研磨機、自動奶泡系統和自清潔技術。這些功能使用戶能夠輕鬆沖泡各種咖啡,完美契合了快節奏都市生活對效率的追求。除了人們對優質咖啡體驗日益成長的興趣外,透過數位平台接觸全球咖啡文化的機會增加也促進了需求的成長。此外,消費者對品質、衛生和個人化客製化的期望不斷提高,推動了製造商的持續創新,從而提高了產品在住宅和商用領域的滲透率。

預計到2025年,濃縮咖啡咖啡機市場規模將達6億美元。這一細分市場深受重視濃郁風味、精準萃取和更精緻咖啡體驗的消費者的青睞。與基本沖泡系統不同,全自動義式濃縮咖啡機代表著更高階、更沉浸式的咖啡沖泡方式,吸引那些追求工藝和品質穩定性的用戶。這些消費者往往將咖啡機視為一種生活方式的長期投資,而非僅僅是廚房電器,因為它們讓他們無需專業知識即可在家中輕鬆沖泡出咖啡館品質的咖啡。人們對專門食品咖啡文化和高品質沖泡方式日益成長的興趣,也持續推動著這一細分市場的需求。

到2025年,住宅用戶將佔市場佔有率的70.1%。家庭消費仍是需求的主要驅動力,使用者群體十分多元化,涵蓋了從休閒咖啡飲用者到資深咖啡鑑賞家等各類人群。此細分市場的成長主要得益於生活方式的改變、都市區家庭數量的增加以及舊家電更換週期的縮短。此外,消費者對全球咖啡趨勢的了解不斷加深,以及對在家享用高階飲品體驗的追求,也促進了住宅咖啡機的普及。在住宅中,消費者越來越傾向於選擇那些操作簡單、設計現代、結構緊湊、性能可靠,並且能夠無縫融入日常生活的咖啡機。

歐洲全自動咖啡機市場預計到2025年將佔據35%的市場佔有率,並在2026年至2035年間以5.5%的複合年成長率成長。該地區是全自動咖啡機市場最成熟、最成熟的市場之一,這要歸功於其悠久的咖啡傳統和對濃縮咖啡咖啡飲品的強烈偏好。在歐洲,咖啡消費已深深融入日常生活,因此人們對咖啡設備的品質、耐用性和性能有著很高的期望。該地區的消費者不僅看重全自動咖啡機的便利性,更重視其能夠始終如一地還原咖啡館風格的飲品,包括濃郁的風味和精準的口感。這種與咖啡的深厚文化聯繫持續支撐著住宅和商用對全自動咖啡機的持續需求。

全球自動咖啡機市場的主要參與者包括雀巢Nespresso SA、德龍集團、飛利浦家用電器、Jura Electroapparato AG、Panasonic Corporation、Melitta集團、Miele & Cie. KG、伊萊克斯、Hamilton Beach Brands、Keuritt de Pepper、Morphys、Newg、Newg、News Brands、Keurim de Pepper、Morphys、Newg、News、News Brands、New Spig。參與企業市場的企業正積極致力於產品創新,透過整合智慧技術(例如基於應用程式的營運、人工智慧驅動的沖泡客製化和節能系統)來提升用戶體驗。此外,各公司正在拓展其高級產品線,以滿足消費者在家中和辦公室追求更高品質咖啡體驗的偏好。他們正加強與零售連鎖店和線上平台的策略合作,以擴大分銷網路並提升品牌知名度。此外,製造商還在設計創新、永續材料和緊湊型機器設計方面進行投資,以吸引空間有限的都市區消費者。自動化、自清潔機制和多功能飲料相容性的不斷改進,進一步幫助企業在競爭激烈的市場中實現產品差異化,並加強與客戶的長期忠誠度。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 全球咖啡消費量的成長和咖啡文化的擴張

- 對便捷省時解決方案的需求日益成長

- 新興市場消費者可支配所得增加

- 產業潛在風險與挑戰

- 高昂的初始投資和實施成本

- 維護、維修和服務成本

- 機會

- 亞太地區和拉丁美洲的未開發潛力

- 訂閱模式(咖啡豆+咖啡機租借)

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 定價分析(基於初步研究)

- 根據玩家類型(高階/中階/經濟型)制定定價策略(基於初步研究)

- 按地區分析價格波動

- 特徵與價格之間的相關性

- 法律規範

- 波特五力分析

- PESTEL 分析

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧驅動的個人化和飲料客製化

- 生成式人工智慧的應用案例(預測性維護、使用者偏好學習)

- 智慧家庭整合和語音助理相容性

- 風險、限制和資料隱私考量

- 消費者購買行為分析

- 購買模式

- 偏好分析

- 消費行為的區域差異

- 電子商務對購買決策的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 滴濾咖啡機

- 單杯滴漏咖啡機

- 多杯滴漏咖啡機

- 附可編程功能的滴漏式咖啡機

- 濃縮咖啡咖啡機

- 一台可以處理從咖啡豆到咖啡杯所有工序的咖啡機

- 全自動咖啡機,相容膠囊和咖啡包

第6章 市場估算與預測:依銷售量/杯裝容量分類,2022-2035年

- 50 杯或更少

- 51-100 杯

- 101-200 杯

- 201-350 杯

- 超過350杯

第7章 市場估計與預測:依價格分類,2022-2035年

- 低價/經濟型(200美元以下)

- 中檔(200-800美元)

- 高級版(超過 800 美元)

第8章 市場估算與預測:最終用途,2022-2035年

- 住宅

- 商業的

- 咖啡館和咖啡店

- 餐廳和飯店

- 辦公室和企業設施

- 零售商店

- 醫療設施

- 其他(教育機構、共享辦公空間)

第9章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 企業網站

- 離線

- 超級市場和大賣場

- 家用電器商店

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- Breville Group Limited

- BSH Hausgerate GmbH

- De'Longhi Group

- Electrolux AB

- Hamilton Beach Brands, Inc.

- Jura Elektroapparate AG

- Keurig Dr Pepper Inc.

- Melitta Group

- Miele &Cie. KG

- Morphy Richards

- Nestle Nespresso SA

- Newell Brands

- Panasonic Corporation

- Philips Domestic Appliances

- SMEG SpA

The Global Automatic Coffee Machine Market was valued at USD 5 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 8.8 billion by 2035.

The market is experiencing steady growth as coffee consumption continues to rise globally, reinforcing its position as a daily essential across both developed and emerging economies. This sustained consumption trend is encouraging wider adoption of automatic coffee machines among households and commercial users who prioritize consistency, speed, and brewing precision. Coffee is increasingly being viewed as a personalized lifestyle product rather than a simple beverage, which is strengthening demand for automated brewing systems that deliver cafe-like quality at home or in workplaces.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5 Billion |

| Forecast Value | $8.8 Billion |

| CAGR | 5.6% |

The growing preference for convenience-oriented appliances is further accelerating market expansion, as consumers seek solutions that simplify preparation while maintaining premium taste standards. Automatic coffee machines are gaining traction due to their ability to streamline brewing through advanced features such as programmable functions, integrated grinders, automated milk frothing systems, and self-cleaning technologies. These capabilities allow users to prepare a wide range of coffee styles with minimal effort, aligning with fast-paced urban lifestyles where time efficiency is essential. Rising interest in premium coffee experiences, along with increasing exposure to global coffee culture through digital platforms, is also contributing to stronger demand. In addition, evolving consumer expectations around consistency, hygiene, and customization are pushing manufacturers to innovate continuously, thereby expanding product penetration across both residential and commercial segments.

In 2025, the espresso coffee machines segment accounted for USD 600 million. This segment appeals strongly to consumers who prioritize rich flavor profiles, brewing precision, and a more refined coffee experience. Unlike basic brewing systems, automatic espresso machines are associated with a more premium and immersive approach to coffee preparation, attracting users who value craftsmanship and consistency. These consumers often view such machines as long-term lifestyle investments rather than simple kitchen appliances, as they enable cafe-quality beverages to be prepared conveniently at home without requiring professional expertise. The growing interest in specialty coffee culture and high-quality brewing methods continues to support demand for this segment.

The residential segment held a 70.1% share in 2025. Household consumption remains the primary driver of demand, spanning a wide range of users from casual drinkers to dedicated coffee enthusiasts. Growth in this segment is supported by evolving lifestyle patterns, increasing urban household formation, and rising replacement cycles for older appliances. Additionally, greater exposure to global coffee trends and the shift toward premium in-home beverage experiences are strengthening residential adoption. Within households, consumers increasingly prefer machines that combine ease of use with modern design, compact structure, and reliable performance, ensuring seamless integration into daily routines.

Europe Automatic Coffee Machine Market held 35% share in 2025 and is projected to grow at a CAGR of 5.5% during 2026-2035. The region represents one of the most established and mature markets for automatic coffee machines, shaped by long-standing coffee traditions and a strong preference for espresso-based beverages. Coffee consumption in Europe is deeply embedded in daily lifestyle habits, influencing high expectations for quality, durability, and performance in coffee equipment. Consumers in the region evaluate automatic coffee machines not only on convenience but also on their ability to consistently replicate authentic cafe-style beverages, including flavor intensity and texture precision. This strong cultural connection to coffee continues to support sustained demand across both residential and commercial applications.

The key companies operating in the Global Automatic Coffee Machine Market include Nestle Nespresso S.A., De'Longhi Group, Philips Domestic Appliances, Jura Elektroapparate AG, Panasonic Corporation, BSH Hausgerate GmbH, Breville Group Limited, Melitta Group, Miele & Cie. KG, Electrolux AB, Hamilton Beach Brands, Inc., Keurig Dr Pepper Inc., Morphy Richards, Newell Brands, and SMEG S.p.A. Market participants are actively focusing on product innovation by integrating smart technologies such as app-based controls, AI-driven brewing customization, and energy-efficient systems to enhance user experience. Companies are also expanding their premium product portfolios to cater to evolving consumer preferences for high-end coffee experiences at home and in offices. Strategic partnerships with retail chains and online platforms are being strengthened to improve distribution reach and brand visibility. In addition, manufacturers are investing in design innovation, sustainability-focused materials, and compact machine formats to attract urban consumers with space constraints. Continuous upgrades in automation features, self-cleaning mechanisms, and multi-beverage capabilities are further helping companies differentiate their offerings and strengthen long-term customer loyalty in a highly competitive market landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Capacity/cup size

- 2.2.4 Price range

- 2.2.5 End-use application

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global coffee consumption & coffee culture expansion

- 3.2.1.2 Growing demand for convenience & time-saving solutions

- 3.2.1.3 Increasing consumer disposable incomes in emerging markets

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment & acquisition costs

- 3.2.2.2 Maintenance, repair & servicing expenses

- 3.2.3 Opportunities

- 3.2.3.1 Untapped potential in Asia Pacific & Latin America

- 3.2.3.2 Subscription-based models (coffee beans + machine rental)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Pricing Strategy by player type (premium/mid-range/budget) (driven by primary research)

- 3.6.2 Regional price variation analysis

- 3.6.3 Feature-to-price correlation

- 3.7 Regulatory framework

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-driven personalization & beverage customization

- 3.10.2 GenAI use cases (predictive maintenance, user preference learning)

- 3.10.3 Smart home integration & voice assistant compatibility

- 3.10.4 Risks, limitations & data privacy considerations

- 3.11 Consumer buying behavior analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behavior

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Drip filter coffee machine

- 5.2.1 Single-serve drip machines

- 5.2.2 Multi-cup drip machines

- 5.2.3 Programmable drip machines

- 5.3 Espresso coffee machine

- 5.4 Bean-to-cup machine

- 5.5 Capsule/pod-compatible automatic machine

Chapter 6 Market Estimates and Forecast, By Capacity/Cup Size, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 ≤50 cups

- 6.3 51-100 cups

- 6.4 101-200 cups

- 6.5 201-350 cups

- 6.6 >350 cups

Chapter 7 Market Estimates and Forecast, By Price, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Budget/Economy (<$200)

- 7.3 Mid-range ($200-$800)

- 7.4 Premium (>$800)

Chapter 8 Market Estimates and Forecast, By End-Use Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Cafes & coffee shops

- 8.3.2 Restaurants & hotels

- 8.3.3 Offices & corporate workplaces

- 8.3.4 Retail outlets

- 8.3.5 Healthcare facilities

- 8.3.6 Others (educational institutions, co-working spaces)

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce

- 9.2.2 Company websites

- 9.3 Offline

- 9.3.1 Supermarkets & hypermarkets

- 9.3.2 Specialty appliance stores

- 9.3.3 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Breville Group Limited

- 11.2 BSH Hausgerate GmbH

- 11.3 De'Longhi Group

- 11.4 Electrolux AB

- 11.5 Hamilton Beach Brands, Inc.

- 11.6 Jura Elektroapparate AG

- 11.7 Keurig Dr Pepper Inc.

- 11.8 Melitta Group

- 11.9 Miele & Cie. KG

- 11.10 Morphy Richards

- 11.11 Nestle Nespresso S.A.

- 11.12 Newell Brands

- 11.13 Panasonic Corporation

- 11.14 Philips Domestic Appliances

- 11.15 SMEG S.p.A.

全球全自動咖啡機市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球全自動咖啡機市場規模、佔有率、趨勢和成長分析報告(2026-2034) 全自動咖啡機市場:按型號、連接方式、銷售管道和最終用戶分類-2026-2032年全球市場預測全自動洗衣機市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,預測2026-2034年

全自動咖啡機市場:按型號、連接方式、銷售管道和最終用戶分類-2026-2032年全球市場預測全自動洗衣機市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,預測2026-2034年 全自動咖啡機市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、銷售管道、地區和競爭對手分類,2021-2031年全自動嵌入式咖啡機市場:依產品類型、價格範圍、通路和最終用戶分類-2026-2032年全球預測按產品類型、機器類型、價格範圍、分銷管道和最終用戶分類的緊湊型全自動咖啡機市場-2026年至2032年全球預測

全自動咖啡機市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、銷售管道、地區和競爭對手分類,2021-2031年全自動嵌入式咖啡機市場:依產品類型、價格範圍、通路和最終用戶分類-2026-2032年全球預測按產品類型、機器類型、價格範圍、分銷管道和最終用戶分類的緊湊型全自動咖啡機市場-2026年至2032年全球預測 全自動咖啡機器的全球市場,類別,各用途,各流通管道,各地區,機會,預測,2018年~2032年

全自動咖啡機器的全球市場,類別,各用途,各流通管道,各地區,機會,預測,2018年~2032年 自動咖啡機市場預測至2032年:按產品類型、自動化程度、分銷管道、最終用戶和地區進行的全球分析

自動咖啡機市場預測至2032年:按產品類型、自動化程度、分銷管道、最終用戶和地區進行的全球分析 全自動咖啡機市場規模、佔有率、成長分析、按類型、最大杯產量、安裝位置、地區 - 產業預測,2025-2032

全自動咖啡機市場規模、佔有率、成長分析、按類型、最大杯產量、安裝位置、地區 - 產業預測,2025-2032