|

市場調查報告書

商品編碼

2038409

2026 年至 2035 年商用地暖的市場機會、成長要素、產業趨勢與預測。Commercial Underfloor Heating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

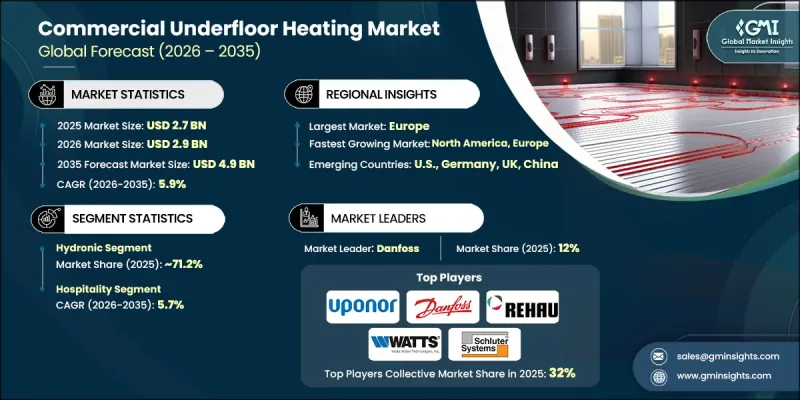

預計到 2025 年,全球商用地暖市場價值將達到 27 億美元,並預計以 5.9% 的複合年成長率成長,到 2035 年達到 49 億美元。

在現代商業基礎設施對節能供暖解決方案需求不斷成長的推動下,該市場持續擴張。已開發國家和新興國家建設活動的增加促進了辦公大樓、飯店和教育機構等場所對節能供暖解決方案的廣泛應用。消費者對舒適度和優質室內環境日益成長的期望進一步推動了先進空間加熱系統的普及。都市化和人口成長加速了商業建築的建設,而對降低營運能源成本的日益重視也推動了高效供暖技術的應用。許多地區嚴峻的氣候變遷和頻繁發生的極端天氣事件也增加了對可靠空間加熱系統的需求。此外,更嚴格的能源效率法規和排放政策迫使商業房地產開發商轉向永續供暖解決方案。憑藉健全的法規結構、廣泛的維修項目以及智慧建築技術的快速普及(這些技術能夠最佳化能源並提高建築性能),歐洲繼續保持其市場主導地位。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 27億美元 |

| 預測金額 | 49億美元 |

| 複合年成長率 | 5.9% |

預計2026年至2035年間,電暖地板市場將以4.2%的複合年成長率成長。該市場的成長主要受城市快速發展、人口密度增加以及對現代地暖解決方案日益成長的需求所驅動。能源效率方面的監管要求推動了清潔能源技術的普及,而人們對提升商業空間室內舒適度的日益關注也進一步加速了電地暖系統的推廣應用。

預計到2025年,酒店業規模將達到5.025億美元,並在2035年之前以5.7%的複合年成長率成長。這一成長主要得益於商業基礎設施的持續發展以及人們對兼顧能源效率和舒適性的供暖解決方案日益成長的需求。除了飯店、餐廳和住宿設施的擴張之外,綠建築標準的日益普及也推動了先進地暖系統在飯店環境中的廣泛應用。

預計2025年,美國商用地暖市場佔有率將達到77.5%,市場規模將達5.706億美元。市場成長的驅動力在於對高效能暖氣技術的需求不斷成長,以及人們對提升商業空間室內舒適度的日益關注。除了商業基礎設施的擴建外,現有建築的持續維修以及清潔能源系統的日益普及,也進一步推動了北美市場的發展。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 原物料供應及採購分析

- 影響價值鏈的關鍵因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 新機會與趨勢

- 利用物聯網技術實現數位轉型

- 滲透新興市場

- 投資分析及未來展望

- 人工智慧和生成式人工智慧對市場的影響(Solution Core)

- AI驅動的生產最佳化(核心解決方案)

- 預測性維護和故障檢測(解決方案核心)

- 貿易數據分析(基於初步調查)

- 進出口數量和價值趨勢(基於初步調查)

- 主要貿易路線及關稅的影響(基於初步調查)

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的產能(基於初步調查)

- 運轉率和擴張計劃(基於初步調查)

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場規模及預測:依技術分類,2022-2035年

- 電的

- 熱水型

第6章 市場規模與預測:依應用領域分類,2022-2035年

- 教育

- 衛生保健

- 零售

- 物流/運輸

- 辦公室

- 飯店業

- 其他

第7章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 西班牙

- 奧地利

- 比利時

- 丹麥

- 芬蘭

- 挪威

- 瑞典

- 英國

- 義大利

- 俄羅斯

- 亞太地區

- 中國

- 日本

- 澳洲

- 印度

- 韓國

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 拉丁美洲

- 巴西

- 墨西哥

第8章:公司簡介

- Amuheat

- aquatherm

- Ceilhit

- Danfoss

- ETHERMA Elektrowarme

- Flexel

- Gaia Climate Solutions

- HEATCOM

- Hemstedt

- Hush Acoustics

- Nuheat

- ProWarm

- PURMO Group

- REHAU

- Schluter Systems

- ThermaRay

- Thermo-Floor UK

- Uponor

- Warmboard

- Warmset

- Warmup

- Watts

The Global Commercial Underfloor Heating Market was valued at USD 2.7 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 4.9 billion by 2035.

The market is witnessing expansion due to increasing demand for energy-efficient heating solutions across modern commercial infrastructure. Growth in construction activity across developed and emerging economies is supporting wider adoption in offices, hospitality buildings, and educational facilities. Rising consumer expectations for enhanced indoor comfort and luxury-oriented environments are further driving the installation of advanced space heating systems. Urbanization and population growth are accelerating commercial construction, while increasing emphasis on reducing operational energy costs is encouraging the adoption of efficient heating technologies. Harsh climatic variations and frequent extreme weather conditions across multiple regions are also strengthening the need for reliable space heating systems. In addition, stricter energy efficiency regulations and emission reduction policies are pushing commercial property developers toward sustainable heating solutions. Europe continues to hold a dominant position in the market due to strong regulatory frameworks, widespread retrofitting activities, and rapid deployment of smart building technologies that enhance energy optimization and building performance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.7 Billion |

| Forecast Value | $4.9 Billion |

| CAGR | 5.9% |

The electric segment is expected to grow at a CAGR of 4.2% from 2026 to 2035. Expansion in this segment is supported by rapid urban development, increasing population density, and rising demand for modern floor heating solutions. The adoption of cleaner energy technologies is being reinforced by regulatory energy efficiency mandates, while growing focus on improving indoor comfort in commercial spaces is further accelerating the penetration of electric-based underfloor heating systems.

The hospitality segment reached USD 502.5 million in 2025 and is projected to grow at a CAGR of 5.7% through 2035. Growth in this segment is supported by the ongoing development of commercial infrastructure and increasing emphasis on energy-efficient and comfort-driven heating solutions. Expansion of hotels, restaurants, and lodging facilities, along with rising adoption of green building standards, is contributing to higher deployment of advanced underfloor heating systems in hospitality environments.

U.S. Commercial Underfloor Heating Market accounted for 77.5% share in 2025 and generated USD 570.6 million. Market growth is driven by increasing demand for efficient heating technologies and rising focus on improved indoor comfort across commercial spaces. Expansion of commercial infrastructure, combined with ongoing retrofitting of existing buildings and greater adoption of clean energy systems, is further strengthening market development across North America.

Key companies operating in the Global Commercial Underfloor Heating Market include Danfoss, REHAU, Uponor, Watts, Schluter Systems, Warmup, PURMO Group, Flexel, Ceilhit, Nuheat, Warmset, Thermo-Floor UK, Hush Acoustics, ETHERMA Elektrowarme, aquatherm, Warmboard, Gaia Climate Solutions, HEATCOM, Amuheat, ThermoRay, and Hemstedt. Companies in the commercial underfloor heating market are focusing on product innovation, energy efficiency improvements, and smart system integration to strengthen their market position. Manufacturers are increasingly developing advanced heating systems compatible with smart building technologies and automated energy management platforms. Expansion of distribution networks and strategic partnerships with construction firms and real estate developers are helping increase market penetration. Firms are also investing in research and development to enhance thermal efficiency, reduce installation complexity, and improve system durability. Sustainability initiatives, including low-energy consumption designs and eco-friendly materials, are being prioritized to align with regulatory standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid Sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Technology trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digital transformation with IoT technologies

- 3.7.2 Emerging market penetration

- 3.8 Investment analysis & future outlook

- 3.9 Impact of AI & Generative AI on the market (Solution Core)

- 3.9.1 AI-Driven production optimization (Solution Core)

- 3.9.2 Predictive maintenance & fault detection (Solution Core)

- 3.10 Trade data analysis (Driven by Primary Research)

- 3.10.1 Import/export volume & value trends (Driven by Primary Research)

- 3.10.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.11 Capacity & production landscape (Driven by Primary Research)

- 3.11.1 Capacity by region & key producer (Driven by Primary Research)

- 3.11.2 Capacity utilization rates & expansion pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Electric

- 5.3 Hydronic

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Education

- 6.3 Healthcare

- 6.4 Retail

- 6.5 Logistics & transportation

- 6.6 Offices

- 6.7 Hospitality

- 6.8 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Spain

- 7.3.4 Austria

- 7.3.5 Belgium

- 7.3.6 Denmark

- 7.3.7 Finland

- 7.3.8 Norway

- 7.3.9 Sweden

- 7.3.10 UK

- 7.3.11 Italy

- 7.3.12 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 Australia

- 7.4.4 India

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Mexico

Chapter 8 Company Profiles

- 8.1 Amuheat

- 8.2 aquatherm

- 8.3 Ceilhit

- 8.4 Danfoss

- 8.5 ETHERMA Elektrowarme

- 8.6 Flexel

- 8.7 Gaia Climate Solutions

- 8.8 HEATCOM

- 8.9 Hemstedt

- 8.10 Hush Acoustics

- 8.11 Nuheat

- 8.12 ProWarm

- 8.13 PURMO Group

- 8.14 REHAU

- 8.15 Schluter Systems

- 8.16 ThermaRay

- 8.17 Thermo-Floor UK

- 8.18 Uponor

- 8.19 Warmboard

- 8.20 Warmset

- 8.21 Warmup

- 8.22 Watts

地暖市場-2026-2032年全球市場預測

地暖市場-2026-2032年全球市場預測 2026 年至 2035 年住宅地暖系統的市場機會、成長要素、產業趨勢與預測。

2026 年至 2035 年住宅地暖系統的市場機會、成長要素、產業趨勢與預測。 2026年全球地暖市場報告

2026年全球地暖市場報告 全球電地暖市場:市場規模、佔有率、趨勢和成長分析(2026-2034)

全球電地暖市場:市場規模、佔有率、趨勢和成長分析(2026-2034) 地暖市場分析及預測(至2035年):按類型、產品類型、技術、組件、應用、材質、安裝方法、設備、解決方案和最終用戶分類全球住宅地暖市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球地暖市場規模、佔有率、趨勢和成長分析報告(2026-2034)

地暖市場分析及預測(至2035年):按類型、產品類型、技術、組件、應用、材質、安裝方法、設備、解決方案和最終用戶分類全球住宅地暖市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球地暖市場規模、佔有率、趨勢和成長分析報告(2026-2034) 地暖市場規模、佔有率和趨勢分析報告:按產品類型、應用、系統、安裝方式、地區和細分市場預測,2026-2033年

地暖市場規模、佔有率和趨勢分析報告:按產品類型、應用、系統、安裝方式、地區和細分市場預測,2026-2033年 地暖市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、組件、安裝類型、應用、地區和競爭格局分類,2021-2031年地暖市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

地暖市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、組件、安裝類型、應用、地區和競爭格局分類,2021-2031年地暖市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)