|

市場調查報告書

商品編碼

2038394

迷你電腦市場商機、成長要素、產業趨勢分析及2026-2035年預測Mini PCs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

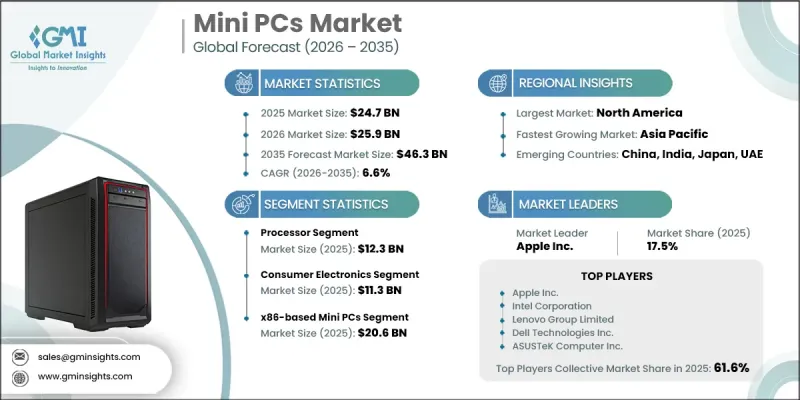

全球迷你電腦市場預計到 2025 年將達到 247 億美元,並以 6.6% 的複合年成長率成長,到 2035 年達到 463 億美元。

受終端用戶在不同環境下對緊湊型、節能型運算系統需求不斷成長的推動,該市場正在蓬勃發展。企業、教育和住宅應用領域的廣泛採用,進一步促進了此類產品的持續普及。邊緣運算基礎設施的擴展也發揮著重要作用,因為企業越來越依賴本地資料處理來降低延遲並提高營運效率。處理器技術和溫度控管的不斷進步,進一步提升了小型化設備的效能。此外,模組化和超小型運算架構的興起,使得辦公室、工業和嵌入式應用領域的靈活部署成為可能。迷你PC與物聯網生態系統和智慧基礎設施的日益融合,也進一步推動了市場需求。企業優先考慮低功耗、節省空間的系統,這些系統既能支援現代工作負載,又能降低營運成本。總而言之,市場正朝著高效、可擴展且針對特定應用的運算解決方案發展,與整個產業的數位轉型趨勢相契合。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 247億美元 |

| 預測金額 | 463億美元 |

| 複合年成長率 | 6.6% |

預計到2025年,處理器市場規模將達到123億美元,在決定迷你PC系統的速度、效率和多任務處理性能方面發揮著至關重要的作用。處理器使緊湊型運算系統能夠高效處理企業工作負載、邊緣運算任務和日常生產力功能。晶片設計和整合技術的不斷改進,在保持低發熱量的同時,不斷提升運算能力。領先的半導體開發商的技術進步,正推動著核心數量的增加、整合圖形性能的提升,以及將人工智慧處理能力整合到緊湊、節能的架構中。

到2025年,家用電子電器市場規模將達到113億美元。這一市場主導地位主要得益於消費者對迷你電腦在個人電腦、家庭娛樂系統和一般辦公室應用領域的強勁需求。消費者越來越傾向於選擇體積小巧、節能高效且效能可靠的設備,以滿足串流媒體播放、網頁瀏覽和基本內容創作等需求。持續的產品創新和不斷提升的用戶體驗進一步推動了迷你電腦在該領域的普及,使其成為滿足現代家庭運算需求的理想選擇。

預計到2025年,北美迷你PC市佔率將達到26.7%。該地區市場成長的主要驅動力是辦公室環境、工業自動化、智慧製造設施、數位電子看板看板應用和教育機構對小型運算系統的日益普及。各組織機構擴大使用迷你PC來最佳化工作空間利用率、降低能耗、支援混合辦公模式以及用於邊緣運算應用。對數位基礎設施、智慧城市建設和人工智慧驅動的邊緣技術的持續投資,正在進一步加速全部區域市場的擴張。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 對緊湊型和節能型運算設備的需求日益成長

- 擴展邊緣運算和物聯網基礎設施

- 商業應用中的推廣應用

- 轉型

- 處理器效能和熱效率的提升

- 產業潛在風險與挑戰

- 與傳統桌上型電腦相比,成本更高

- 高負載環境下的溫度控管和效能限制

- 市場機遇

- 迷你PC在邊緣人工智慧和智慧基礎設施領域的應用日益廣泛

- 數位電子看板和自助服務生態系統對迷你電腦的需求日益成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢(基於付費資料庫)

- 歷史價格分析(2022-2025)

- 影響價格趨勢的因素

- 區域價格波動

- 價格預測(2026-2035)

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的設備產能

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按收入、地區和創新能力分類的層級定位矩陣。

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 完全組裝迷你電腦

- 準系統迷你電腦

- 無風扇/加固型迷你電腦

第6章 市場估計與預測:依組件分類,2022-2035年

- 處理器

- 記憶

- 貯存

- GPU

- 其他

第7章 市場估算與預測:依處理器架構分類,2022-2035年

- 基於 x86 的迷你電腦

- 基於ARM的迷你電腦

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 個人/家庭電腦

- 家庭娛樂媒體

- 數位電子看板亭

- 遊戲和內容創作

- 商務/辦公室

- 工業和邊緣運算

- 其他

第9章 市場估計與預測:依產業分類,2022-2035年

- 家用電子電器

- 零售

- 製造業

- 教育

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 全球主要公司

- Acer Inc.

- Apple Inc.

- ASUSTeK Computer Inc.

- Dell Technologies Inc.

- HP Inc.

- Intel Corporation

- Lenovo Group Limited

- GIGA-BYTE Technology Co., Ltd.

- 按地區分類的主要公司

- ASRock Inc.

- Azulle

- Beelink

- Elitegroup Computer Systems Co. Ltd.

- Hasee

- Miniforum

- 特殊玩家/干擾者

- Thinvent

- WEY Technology AG

The Global Mini PCs Market was valued at USD 24.7 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 46.3 billion by 2035.

The market is experiencing growth driven by increasing demand for compact, energy-efficient computing systems across diverse end-use environments. Rising adoption in enterprise environments, education systems, and residential applications is supporting sustained product penetration. Expansion of edge computing infrastructure is also playing a major role, as organizations increasingly rely on localized data processing to reduce latency and improve operational efficiency. Continuous advancements in processor technology and thermal management are further enhancing system performance within smaller form factors. Additionally, the growing shift toward modular and ultra-compact computing architectures is enabling flexible deployment across office, industrial, and embedded applications. Increasing integration of mini PCs into IoT ecosystems and smart infrastructure is further strengthening demand. Enterprises are prioritizing low-power, space-efficient systems that can support modern workloads while reducing operational costs. Overall, the market is evolving toward highly efficient, scalable, and application-specific computing solutions that align with digital transformation trends across industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $24.7 Billion |

| Forecast Value | $46.3 Billion |

| CAGR | 6.6% |

The processor segment reached USD 12.3 billion in 2025, owing to its essential role in defining system speed, efficiency, and multitasking performance in mini PCs. Processors enable compact computing systems to efficiently handle enterprise workloads, edge computing tasks, and everyday productivity functions. Ongoing improvements in chip design and integration technologies are enhancing computing capabilities while maintaining low thermal output. Advancements from major semiconductor developers are contributing to higher core counts, integrated graphics performance, and built-in AI processing features, all within compact power-efficient architectures.

The consumer electronics segment accounted for USD 11.3 billion in 2025. This dominance is supported by strong demand for mini PCs in personal computing, home entertainment systems, and general productivity use. Consumers are increasingly choosing compact and energy-efficient devices that offer reliable performance for streaming, browsing, and basic content creation activities. Continuous product innovation and enhanced user experience features are further strengthening adoption in this segment, making mini PCs a preferred choice for modern home computing needs.

North America Mini PCs Market represented 26.7% share in 2025. Market growth in the region is supported by rising adoption of compact computing systems across office environments, industrial automation, smart manufacturing facilities, digital signage applications, and educational institutions. Organizations are increasingly using mini PCs to optimize workspace utilization, reduce energy consumption, and support hybrid working models along with edge computing applications. Continued investment in digital infrastructure, smart city development, and AI-driven edge technologies is further accelerating market expansion across the region.

Key companies operating in the Global Mini PCs Market include Apple Inc., Dell Technologies Inc., HP Inc., Lenovo Group Limited, Intel Corporation, Acer Inc., ASUSTeK Computer Inc., GIGA-BYTE Technology Co. Ltd., ASRock Inc., Azulle, Beelink, Elitegroup Computer Systems Co. Ltd., Hasee, Minisforum, Thinvent, WEY Technology AG, Zotac Technology Limited, and ASUSTeK Computer Inc. Companies in the Mini PCs Market are focusing on strengthening their competitive position through continuous product innovation and performance optimization. Manufacturers are investing heavily in advanced processor integration and energy-efficient system designs to enhance computing power within compact form factors. Expansion into edge computing and IoT-compatible devices is a key strategy, enabling broader application across industrial and commercial environments. Firms are also prioritizing modular and customizable product architectures to support diverse enterprise requirements. Strategic partnerships with technology providers are helping improve ecosystem integration and accelerate adoption across end-use sectors. Additionally, companies are enhancing thermal management systems and hardware efficiency to support high-performance workloads in smaller devices.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Processor Architecture trends

- 2.2.3 Application trends

- 2.2.4 Industry Vertical trends

- 2.2.5 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for compact and energy-efficient computing devices

- 3.2.1.2 Expansion of edge computing and IoT infrastructure

- 3.2.1.3 Growing adoption in commercial applications

- 3.2.1.4 Shift toward hybrid work and cloud-based enterprise environments

- 3.2.1.5 Advancements in processor performance and thermal efficiency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Higher cost compared to traditional desktop PCs

- 3.2.2.2 Thermal management and performance constraints in high workloads

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of mini PCs in edge AI and smart infrastructure

- 3.2.3.2 Rising demand for mini PCs in digital signage and self-service ecosystems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends (Based on paid Database)

- 3.7.1 Historical Price Analysis (2022-2025)

- 3.7.2 Price Trend Drivers

- 3.7.3 Regional Price Variations

- 3.7.4 Price Forecast (2026-2035)

- 3.8 Impact of AI & Generative AI on the Market

- 3.8.1 AI-Driven Disruption of Existing Business Models

- 3.8.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.8.3 Risks, Limitations & Regulatory Considerations

- 3.9 Capacity & Production Landscape (Driven by Primary Research)

- 3.9.1 Installed Capacity by Region & Key Producer

- 3.9.2 Capacity Utilization Rates & Expansion Pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia-Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By Region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million)

- 5.1 Key trends

- 5.2 Fully assembled mini PCs

- 5.3 Barebone mini PCs

- 5.4 Fanless/Rugged mini PCs

Chapter 6 Market Estimates and Forecast, By Component, 2022-2035 (USD Million)

- 6.1 Key trends

- 6.2 Processor

- 6.3 Memory

- 6.4 Storage

- 6.5 GPU

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Processor Architecture, 2022-2035 (USD Million)

- 7.1 Key trends

- 7.2 x86-based Mini PCs

- 7.3 ARM-based Mini PCs

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Million)

- 8.1 Key trends

- 8.2 Personal / home computing

- 8.3 Home entertainment & media

- 8.4 Digital signage & kiosks

- 8.5 Gaming & content creation

- 8.6 Business / office

- 8.7 Industrial & edge computing

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Industry Vertical, 2022-2035 (USD Million)

- 9.1 Key trends

- 9.2 Consumer Electronics

- 9.3 Retail

- 9.4 Manufacturing

- 9.5 Education

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Acer Inc.

- 11.1.2 Apple Inc.

- 11.1.3 ASUSTeK Computer Inc.

- 11.1.4 Dell Technologies Inc.

- 11.1.5 HP Inc.

- 11.1.6 Intel Corporation

- 11.1.7 Lenovo Group Limited

- 11.1.8 GIGA-BYTE Technology Co., Ltd.

- 11.2 Regional key players

- 11.2.1 ASRock Inc.

- 11.2.2 Azulle

- 11.2.3 Beelink

- 11.2.4 Elitegroup Computer Systems Co. Ltd.

- 11.2.5 Hasee

- 11.2.6 Miniforum

- 11.3 Niche Players/Disruptors

- 11.3.1 Thinvent

- 11.3.2 WEY Technology AG

迷你電腦市場-2026-2032年全球市場預測

迷你電腦市場-2026-2032年全球市場預測 工業個人電腦市場-全球產業規模、佔有率、趨勢、機會和預測,依產品類型、應用、最終用戶產業、地區和競爭格局分類,2021-2031年預測

工業個人電腦市場-全球產業規模、佔有率、趨勢、機會和預測,依產品類型、應用、最終用戶產業、地區和競爭格局分類,2021-2031年預測 全球個人電腦市場

全球個人電腦市場 全球個人電腦市場(2024-2028)全球迷你電腦市場

全球個人電腦市場(2024-2028)全球迷你電腦市場