|

市場調查報告書

商品編碼

2038393

一次性輸尿管鏡市場機會、成長要素、產業趨勢分析及2026-2035年預測。Disposable Ureteroscope Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

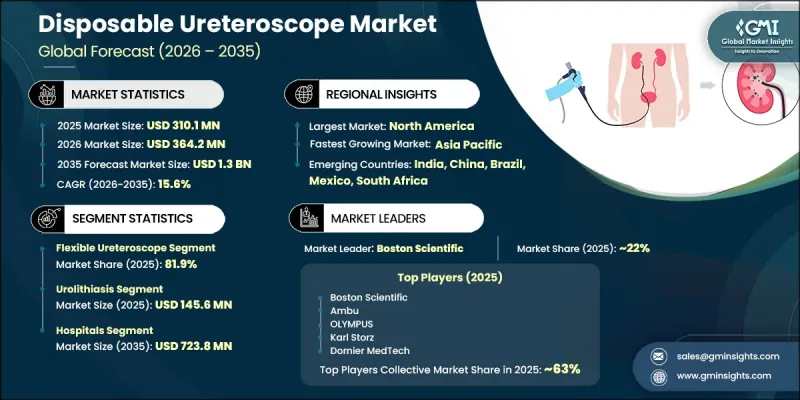

全球一次性輸尿管鏡市場預計到 2025 年將達到 3.101 億美元,年複合成長率為 15.6%,到 2035 年將達到 13 億美元。

尿道結石發生率的上升、影像和內視鏡技術的不斷進步以及微創泌尿系統手術日益普及,共同推動了市場擴張。隨著醫療專業人員優先考慮快速診斷和降低感染風險,門診手術中心對一次性輸尿管鏡的採用率不斷提高,也促進了市場需求。一次性輸尿管鏡是專為輸尿管和腎臟疾病的可視化和治療而設計的單次使用內視鏡器械,提供軟性或半剛性配置,並整合成像系統。這些器械有助於準確診斷和治療腎結石、輸尿管狹窄和泌尿道腫瘤,同時顯著降低交叉感染的風險,無需再進行處理或消毒。其高效的操作和穩定的性能使其在現代泌尿系統實踐中越來越受歡迎。此外,醫療成本的上升以及新興地區獲得先進外科手術服務的機會增加,也推動了其應用。向價值導向型醫療模式的轉變也促進了經濟高效的一次性器械的使用,有助於其長期市場滲透。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 3.101億美元 |

| 預測金額 | 13億美元 |

| 複合年成長率 | 15.6% |

預計到2025年,軟性輸尿管鏡市場佔有率將達到81.9%,這主要得益於其較高的臨床應用率以及在微創泌尿系統手術中卓越的操作性能。該細分市場的主導地位源於其在複雜腎臟結構中出色的導航和視覺化能力,使其成為輸尿管鏡檢查和逆行性腎內手術等手術的理想選擇。此外,對感染控制、手術流程一致性和操作效率的日益重視,也進一步推動了醫院和門診手術機構對一次性軟性輸尿管鏡的需求。

預計到2025年,尿道結石市場規模將達到1.456億美元。尿道結石,俗稱腎結石,影響全球眾多人群,並且仍然是泌尿系統手術的主要原因之一。由於肥胖和糖尿病盛行率的上升,以及生活方式相關的飲食改變導致結石形成,疾病的發生率正在增加。日益加重的疾病負擔加速了對有效診斷和治療方案的需求。一次性輸尿管鏡因其高清成像功能能夠準確檢測和治療泌尿系統結石,從而改善臨床療效,因此在該領域得到廣泛應用。

到2025年,北美一次性輸尿管鏡市佔率將達到38.7%。該地區的領先地位得益於腎結石、尿道感染、輸尿管狹窄和腎癌等泌尿系統疾病的高發生率。隨著醫療系統不斷依賴先進的內視鏡解決方案來提供高效且微創的治療,醫院和門診手術中心開展的手術數量不斷增加,進一步推動了市場需求。

目錄

第1章:調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策和資料完整性計劃

- 資訊來源一致性協議

- GMI人工智慧政策和資料完整性計劃

- 調查過程和可靠性評分

- 調查過程的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 每種方法中基準年的計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 關於調查透明度的補充信息

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 全球尿道結石和腎結石的發生率不斷上升。

- 一次內視鏡的技術進步

- 人們越來越傾向選擇微創泌尿系統手術

- 產業潛在風險與挑戰

- 輸尿管鏡手術費用高昂

- 新興市場保險覆蓋範圍和報銷方面面臨的挑戰

- 市場機遇

- 進入泌尿系統基礎設施正在發展的新興市場。

- 適用於兒童和複雜解剖結構的微型化應用

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 科技趨勢

- 當前技術趨勢

- 新興技術

- 未來市場趨勢

- 專利趨勢(基於初步調查)

- 投資與資金籌措分析

- 成本效益分析:拋棄式輸尿管鏡與可重複使用輸尿管鏡

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 波特五力分析

- PESTEL 分析

- 客戶洞察(基於初步研究)

- 創業場景

- 價值鏈分析

- 差距分析

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析(基於初步研究)

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要市場公司的競爭分析

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 軟性輸尿管鏡

- 硬式輸尿管鏡

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 尿道結石

- 尿道狹窄

- 腎癌

- 其他用途

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院

- 門診手術中心

- 其他最終用戶

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Ambu

- Becton, Dickinson and Company

- Boston Scientific

- Coloplast

- Cook Medical

- Dornier MedTech

- Karl Storz

- NeoScope

- OLYMPUS

- OPCOM Medical

- OTU Medical

- Richard Wolf

- STERIS

- Zhuhai Pusen Medical Technology

The Global Disposable Ureteroscope Market was valued at USD 310.1 million in 2025 and is estimated to grow at a CAGR of 15.6% to reach USD 1.3 billion in 2035.

The market expansion is influenced by the rising incidence of urolithiasis, continuous advancements in imaging and endoscopic technologies, and growing preference for minimally invasive urological procedures. Increasing adoption across ambulatory surgical centers is also reinforcing demand, as healthcare providers prioritize faster turnaround times and reduced infection risks. Disposable ureteroscopes are single-use endoscopic instruments designed for visualization and treatment of ureter and kidney conditions, offering flexible or semi-rigid configurations with integrated imaging systems. These devices support accurate diagnosis and management of kidney stones, ureteral strictures, and urinary tract tumors while significantly reducing cross-contamination risks and eliminating the need for reprocessing and sterilization. Their operational efficiency and consistent performance are making them increasingly preferred in modern urology practices. In addition, rising healthcare expenditure and expanding access to advanced surgical care in emerging regions are further supporting adoption. The growing shift toward value-based healthcare models is also encouraging the use of cost-efficient single-use devices, contributing to long-term market penetration.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $310.1 Million |

| Forecast Value | $1.3 Billion |

| CAGR | 15.6% |

The flexible ureteroscope segment held a share of 81.9% in 2025, supported by strong clinical adoption and superior maneuverability in minimally invasive urological procedures. This segment's leadership is attributed to its ability to provide enhanced navigation and visualization within complex renal structures, making it highly suitable for procedures such as ureteroscopy and retrograde intrarenal surgery. Increasing emphasis on infection control, procedural consistency, and operational efficiency is further driving preference for single-use flexible ureteroscopes across hospitals and ambulatory surgical environments.

The urolithiasis segment reached USD 145.6 million in 2025. Urolithiasis, commonly known as kidney stone disease, affects a significant global population and remains a leading cause of urological interventions. The condition continues to rise due to increasing prevalence of obesity, diabetes, and lifestyle-related dietary changes, which collectively contribute to higher stone formation rates. This growing disease burden is accelerating demand for effective diagnostic and therapeutic solutions. Disposable ureteroscopes are widely utilized in this segment due to their high-definition imaging capabilities, enabling precise detection and treatment of stones within the urinary tract and improving clinical outcomes.

North America Disposable Ureteroscope Market captured 38.7% share in 2025. The region's dominance is supported by a high prevalence of urological conditions such as kidney stones, urinary tract infections, ureteral strictures, and renal cancers. Increasing procedural volumes across hospitals and ambulatory surgical centers are further strengthening demand, as healthcare systems continue to rely on advanced endoscopic solutions for efficient and minimally invasive treatment delivery.

Key players operating in the Global Disposable Ureteroscope Market include Ambu, Becton, Dickinson and Company, Boston Scientific, Coloplast, Cook Medical, Dornier MedTech, Karl Storz, NeoScope, OLYMPUS, OPCOM Medical, OTU Medical, Richard Wolf, STERIS, and Zhuhai Pusen Medical Technology. Companies in the disposable ureteroscope market are actively focusing on product innovation to enhance imaging quality, flexibility, and ergonomic design for improved procedural efficiency. Many manufacturers are investing in advanced digital visualization technologies and integrated imaging systems to support more accurate diagnosis and treatment outcomes. Strategic collaborations with hospitals and ambulatory surgical centers are being used to expand product adoption and strengthen distribution networks. Firms are also prioritizing cost optimization strategies to make single-use devices more accessible across diverse healthcare settings. Expansion into emerging healthcare markets is supporting revenue diversification and broader geographic reach.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of urolithiasis & kidney stone disease globally

- 3.2.1.2 Technological advancements in disposable endoscopes

- 3.2.1.3 Increasing preference for minimally invasive urological procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of ureteroscopy procedures

- 3.2.2.2 Insurance coverage and reimbursement challenges in emerging markets

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with growing urology infrastructure

- 3.2.3.2 Miniaturization for pediatric and complex anatomical applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Patent landscape (Driven by primary research)

- 3.8 Investment and funding analysis

- 3.9 Cost-effectiveness analysis: disposable vs. reusable ureteroscopes

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 GenAI use cases and adoption roadmap by segment

- 3.10.3 Risks, Limitations and regulatory considerations

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Customer insights (Driven by primary research)

- 3.14 Start-up scenarios

- 3.15 Value chain analysis

- 3.16 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Flexible ureteroscope

- 5.3 Rigid ureteroscope

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Urolithiasis

- 6.3 Urethral stricture

- 6.4 Kidney cancer

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Ambu

- 9.2 Becton, Dickinson and Company

- 9.3 Boston Scientific

- 9.4 Coloplast

- 9.5 Cook Medical

- 9.6 Dornier MedTech

- 9.7 Karl Storz

- 9.8 NeoScope

- 9.9 OLYMPUS

- 9.10 OPCOM Medical

- 9.11 OTU Medical

- 9.12 Richard Wolf

- 9.13 STERIS

- 9.14 Zhuhai Pusen Medical Technology

一次性輸尿管鏡市場規模、佔有率和成長分析:按產品類型、應用、最終用戶和地區分類-2026-2033年產業預測

一次性輸尿管鏡市場規模、佔有率和成長分析:按產品類型、應用、最終用戶和地區分類-2026-2033年產業預測 一次性輸尿管鏡市場分析及預測(至2035年):依類型、產品類型、技術、應用、最終用戶、材質、設備、製程、安裝類型及模式分類

一次性輸尿管鏡市場分析及預測(至2035年):依類型、產品類型、技術、應用、最終用戶、材質、設備、製程、安裝類型及模式分類 一次性輸尿管鏡市場按產品類型、技術、應用、最終用戶和分銷管道分類—2025-2030 年全球預測

一次性輸尿管鏡市場按產品類型、技術、應用、最終用戶和分銷管道分類—2025-2030 年全球預測 一次性輸尿管鏡市場-全球產業規模、佔有率、趨勢、機會和預測,按產品類型、應用、最終用戶、地區和競爭細分,2020-2030 年

一次性輸尿管鏡市場-全球產業規模、佔有率、趨勢、機會和預測,按產品類型、應用、最終用戶、地區和競爭細分,2020-2030 年 一次性輸尿管鏡市場規模、佔有率、趨勢分析報告:按產品、應用、最終用途、地區和細分市場預測,2025-2030 年

一次性輸尿管鏡市場規模、佔有率、趨勢分析報告:按產品、應用、最終用途、地區和細分市場預測,2025-2030 年