|

市場調查報告書

商品編碼

2038353

女性科技市場機會、成長要素、產業趨勢分析及2026-2035年預測。Femtech Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

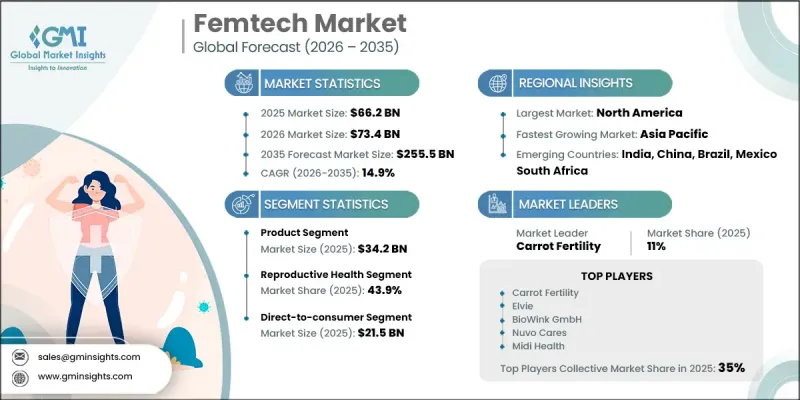

2025 年全球女性科技市場價值 662 億美元,預計到 2035 年將以 14.9% 的複合年成長率成長至 2,555 億美元。

這項市場擴張主要得益於數位科技在女性健康管理中日益普及,尤其是在已開發國家。智慧型手機的高普及率、廣泛的網路連線以及成熟的數位健康基礎設施,使女性能夠在人生的各個階段主動管理自身健康。用於月經行動醫療追蹤、備孕、懷孕監測、更年期支持以及多囊性卵巢症候群(PCOS)和子宮卵巢症等慢性疾病管理的行動健康應用程式、穿戴式裝置和互聯數位平台的應用正在迅速擴展。日益增強的健康意識以及對個人化、數據驅動型醫療保健方法的偏好,進一步加速了已開發國家的市場滲透。這些數位解決方案為使用者提供即時健康追蹤、預測性洞察和循證建議,從而支持早期檢測、預防醫學並提高治療效率。此外,人工智慧、遠端醫療服務和遠距監測系統的整合,在減少對傳統面對面諮詢依賴的同時,也改善了臨床決策。有利的法規環境、對數位健康新創公司投資的增加以及虛擬醫療服務模式的廣泛接受,都在推動整個市場的發展。隨著醫療保健系統越來越重視預防醫學和以病人為中心的照護模式,女性健康科技解決方案正成為現代醫療保健服務的核心要素,這進一步凸顯了數位化創新作為關鍵驅動力的重要性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 662億美元 |

| 預測市場規模 | 2555億美元 |

| 複合年成長率 | 14.9% |

生殖健康領域佔女性健康科技市場的43.9%,預計2025年將達到291億美元。該領域是推動女性健康科技市場成長的主要動力,因為它廣泛涵蓋了女性的基本醫療保健需求,包括月經週期管理、生育支持、懷孕護理、產後監測和更年期相關解決方案。由於這些需求貫穿女性的一生,因此對支持監測、預防和知情決策的數位健康工具的需求持續存在。人們對個人化、預防性生殖健康保健的日益重視進一步推動了該領域的成長。女性健康科技平台被廣泛用於月經週期追蹤、生育最佳化、懷孕監測和產後護理,提供數據驅動的洞察,幫助使用者更積極、更有效地管理自身的生殖健康。

預計到2025年,D2C(直接面對消費者)市場規模將達到215億美元。隨著消費者對個人化醫療保健解決方案的需求日益成長,這一市場持續擴張。女性健康科技供應商正透過D2C管道提供專注於月經健康、生育管理、更年期護理和慢性病監測的客製化數位產品,以滿足這一需求。透過利用使用者產生的健康數據,企業不斷改進解決方案,增強個人化體驗,並提高產品的整體有效性,進而提升消費者滿意度和忠誠度。

預計到2025年,北美女性健康科技市場將佔據32.4%的市場。該地區的成長主要得益於智慧型手機、穿戴式科技和先進數位健康平台的高普及率,這些技術已經徹底改變了女性的健康管理方式。女性健康科技解決方案被廣泛應用於月經週期追蹤、備孕、懷孕監測和更年期管理,從而增強了女性的持續健康意識和健康管理能力。人工智慧(AI)分析、遠端醫療平台和遠端監測工具的整合,有助於提供更個人化的預防性醫療保健服務。這些技術也有助於提高醫療保健系統的效率,促進早期診斷,減少就醫次數,並提高治療方案的依從性。

目錄

第1章:調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策和資料完整性計劃

- 資訊來源一致性協議

- GMI人工智慧政策和資料完整性計劃

- 調查過程和可靠性評分

- 調查過程的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 每種方法中基準年的計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 關於調查透明度的補充信息

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 已開發國家在婦女健康管理中使用數位技術

- 改善偏遠地區婦女獲得醫療保健服務的機會

- 開發中國家對女性健康和福祉的認知不斷提高

- 女性族群慢性疾病及感染疾病負擔加重

- 產業潛在風險與挑戰

- 擴大對女性科技業的投資

- 對女性科技產品及其應用的認知度較低

- 市場機遇

- 企業健康和雇主主導的項目

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 技術趨勢(基於初步調查)

- 當前技術趨勢

- 穿戴式和基於感測器的女性健康科技設備

- 先進的影像技術和微創女性健康技術

- 新興技術

- 下一代人工智慧和機器學習

- 數位雙胞胎科技在女性健康領域的應用

- 當前技術趨勢

- 未來市場趨勢(基於初步研究)

- 人工智慧和生成式人工智慧對市場的影響(基於初步研究)

- 2025年價格分析(基於初步調查)

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 產品

- 軟體

- 服務

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 生殖健康

- 月經週期與生育能力

- 停經

- 孕期護理

- 孕產婦、產後及母乳哺育護理

- 身心健康與整體福祉

- 其他用途

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 面向一般消費者

- 醫院

- 不孕症治療診所

- 外科中心

- 診斷中心

- 其他最終用戶

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Amara Therapeutics

- Athena Feminine Technologies

- Baby Billy

- BioWink GmbH

- Carrot Fertility

- Cofertility

- Conceivable, Inc.

- Elvie

- HeraMED

- iSono Health

- Midi Health

- Minerva Surgical

- Nuvo Cares

- Sera Prognostics

- Trellis Health

- Univfy

The Global Femtech Market was valued at USD 66.2 billion in 2025 and is estimated to grow at a CAGR of 14.9% to reach USD 255.5 billion by 2035.

The expansion of the market is strongly influenced by the increasing integration of digital technologies into women's healthcare management, particularly across developed economies. High smartphone usage, widespread internet connectivity, and a mature digital health infrastructure are enabling women to actively engage in managing their health across different stages of life. The adoption of mobile health applications, wearable devices, and connected digital platforms is growing rapidly for menstrual tracking, fertility planning, pregnancy monitoring, menopause support, and management of chronic conditions such as PCOS and endometriosis. Rising health awareness and a growing preference for personalized and data-driven healthcare approaches are further accelerating market penetration in advanced economies. These digital solutions are empowering users with real-time health tracking, predictive insights, and evidence-based recommendations that enhance early detection, preventive care, and treatment efficiency. The integration of artificial intelligence, telehealth services, and remote monitoring systems is also improving clinical decision-making while reducing dependence on traditional in-person consultations. Supportive regulatory environments, increasing investment in digital health startups, and broader acceptance of virtual healthcare delivery models are strengthening overall market development. As healthcare systems increasingly prioritize preventive and patient-centric care models, femtech solutions are becoming a core component of modern healthcare delivery, reinforcing the importance of digital innovation as a key growth driver.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $66.2 Billion |

| Forecast Value | $255.5 Billion |

| CAGR | 14.9% |

The reproductive health segment held a 43.9%, reaching USD 29.1 billion in 2025. This segment leads the femtech market due to its wide-ranging coverage of essential healthcare needs, including menstruation management, fertility support, pregnancy care, postpartum monitoring, and menopause-related solutions. These needs occur repeatedly throughout a woman's life, ensuring sustained demand for digital health tools that support monitoring, prevention, and informed decision-making. Increasing preference for personalized and preventive reproductive healthcare is further strengthening segment growth. Femtech platforms are widely used for cycle tracking, fertility optimization, prenatal monitoring, and postnatal care, delivering data-backed insights that help users manage their reproductive health more proactively and efficiently.

The direct-to-consumer segment generated USD 21.5 billion in 2025. The segment continues to expand as consumers increasingly demand healthcare solutions tailored to individual needs and preferences. Femtech providers are meeting this demand by offering customized digital products focused on menstrual health, fertility management, menopause care, and chronic condition monitoring through direct-to-consumer channels. By utilizing user-generated health data, companies are continuously refining their solutions, improving personalization, and enhancing overall product effectiveness, which contributes to stronger consumer satisfaction and loyalty.

North America Femtech Market accounted for 32.4% share in 2025. The region's growth is supported by high adoption of smartphones, wearable technologies, and advanced digital health platforms that have transformed women's healthcare management. Femtech solutions are widely applied for menstrual tracking, fertility planning, pregnancy monitoring, and menopause management, enabling continuous engagement and improved health awareness. The integration of artificial intelligence-driven analytics, telehealth platforms, and remote monitoring tools supports more personalized and preventive care delivery. These technologies also facilitate early diagnosis, reduce the need for frequent hospital visits, and improve adherence to treatment plans, contributing to greater efficiency in healthcare systems.

Key players operating in the Global Femtech Industry include Athena Feminine Technologies, Amara Therapeutics, Baby Billy, BioWink GmbH, Carrot Fertility, Cofertility, Conceivable, Inc., Elvie, HeraMED, iSono Health, Midi Health, Minerva Surgical, Nuvo Cares, Sera Prognostics, Trellis Health, and Univfy. Companies in the global femtech market are focusing on expanding digital ecosystems through partnerships with healthcare providers, insurers, and technology firms to enhance service integration. They are investing heavily in artificial intelligence, predictive analytics, and data-driven platforms to improve personalization and clinical accuracy. Product diversification across menstrual health, fertility, pregnancy, and menopause care is being prioritized to address a broader user base. Many players are strengthening their direct-to-consumer models by enhancing mobile app experiences and improving user engagement through personalized recommendations. Strategic funding in digital health startups is supporting innovation and faster market expansion.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Application trends

- 2.2.3 End Use trends

- 2.2.4 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Usage of digital technology to manage women health in developed countries

- 3.2.1.2 Improving access to women care in remote areas

- 3.2.1.3 Growing awareness regarding women health and wellness in developing countries

- 3.2.1.4 Increasing burden of chronic and infectious diseases among the female population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Growing investments in femtech industry

- 3.2.2.2 Lack of awareness about femtech products and applications

- 3.2.3 Market opportunities

- 3.2.3.1 Corporate wellness and employer-sponsored programs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape (Driven by primary research)

- 3.5.1 Current technological trends

- 3.5.1.1 Wearable and sensor based femtech devices

- 3.5.1.2 Advanced imaging & minimally invasive women’s health technologies

- 3.5.2 Emerging technologies

- 3.5.2.1 Next-generation AI & machine learning

- 3.5.2.2 Digital twin technology for women's health

- 3.5.1 Current technological trends

- 3.6 Future market trends (Driven by primary research)

- 3.7 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.8 Pricing analysis, 2025 (Driven by primary research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Products

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Reproductive health

- 6.2.1 Menstrual cycle and fertility

- 6.2.2 Menopause

- 6.3 Pregnancy care

- 6.4 Maternal/post-partum and nursing care

- 6.5 Integrative physical and mental health & overall well-being

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Direct-to-consumer

- 7.3 Hospitals

- 7.4 Fertility clinics

- 7.5 Surgical centers

- 7.6 Diagnostic centers

- 7.7 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amara Therapeutics

- 9.2 Athena Feminine Technologies

- 9.3 Baby Billy

- 9.4 BioWink GmbH

- 9.5 Carrot Fertility

- 9.6 Cofertility

- 9.7 Conceivable, Inc.

- 9.8 Elvie

- 9.9 HeraMED

- 9.10 iSono Health

- 9.11 Midi Health

- 9.12 Minerva Surgical

- 9.13 Nuvo Cares

- 9.14 Sera Prognostics

- 9.15 Trellis Health

- 9.16 Univfy

女性科技市場:全球市場按產品類型、技術、應用、最終用戶和分銷管道分類的預測,2026-2032年

女性科技市場:全球市場按產品類型、技術、應用、最終用戶和分銷管道分類的預測,2026-2032年 2026年全球女性科技市場報告

2026年全球女性科技市場報告 女性健康科技市場分析及至2035年預測:按類型、產品類型、服務、技術、組件、應用、設備、最終用戶和解決方案分類

女性健康科技市場分析及至2035年預測:按類型、產品類型、服務、技術、組件、應用、設備、最終用戶和解決方案分類 全球女性健康科技市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球女性健康科技市場規模、佔有率、趨勢及成長分析報告(2026-2034) 2026-2030年全球女性健康科技設備市場女性科技市場-2026-2031年預測

2026-2030年全球女性健康科技設備市場女性科技市場-2026-2031年預測 全球智慧電網市場:按技術、應用和地區分析-市場規模、產業趨勢、機會分析和預測(2026-2035)

全球智慧電網市場:按技術、應用和地區分析-市場規模、產業趨勢、機會分析和預測(2026-2035) 女性健康科技市場規模、佔有率及成長分析(按產品、服務、應用、最終用戶和地區分類)-2026-2033年產業預測

女性健康科技市場規模、佔有率及成長分析(按產品、服務、應用、最終用戶和地區分類)-2026-2033年產業預測 女性科技市場-全球產業規模、佔有率、趨勢、機會和預測(按產品、應用、最終用途、地區和競爭細分,2020-2030 年)

女性科技市場-全球產業規模、佔有率、趨勢、機會和預測(按產品、應用、最終用途、地區和競爭細分,2020-2030 年) 2032 年女性科技市場預測:按類型、功能、應用、最終用戶和地區進行的全球分析

2032 年女性科技市場預測:按類型、功能、應用、最終用戶和地區進行的全球分析