|

市場調查報告書

商品編碼

2038351

防彈背心市場商機、成長要素、產業趨勢分析及2026-2035年預測。Body Armor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

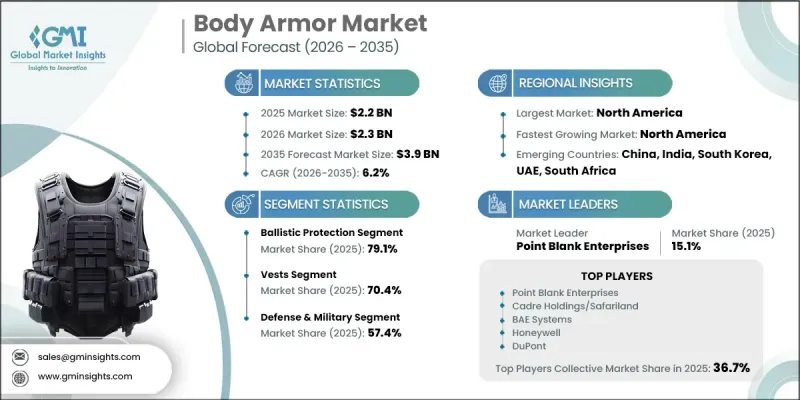

全球防彈背心市場預計到 2025 年將價值 22 億美元,預計到 2035 年將以 6.2% 的複合年成長率成長至 39 億美元。

在全球國防和安全部隊日益重視人員安全和作戰效率的推動下,市場持續擴張。軍事組織的現代化建設推動了先進防護裝備的普及,這些裝備在提供更高彈道防護的同時,保持輕量化結構,從而增強了機動性和耐用性。日益嚴峻的全球安全情勢,包括恐怖主義和犯罪活動的增加,進一步刺激了對個人防護裝備的需求。執法機關擴大為其人員配備先進的防護解決方案,以保護他們免受槍支和刀具等武器的威脅。同時,公眾個人安全意識的提高也促進了高風險環境中防護裝備的廣泛應用。暴力事件和安全威脅日益頻繁的凸顯了可靠防護系統的重要性。材料科學的持續創新使得更輕、更堅固、更舒適的防護解決方案得以開發,從而提高了易用性和普及性。合適的尺寸、符合人體工學的設計以及全身防護仍然是影響產品有效性和市場接受度的關鍵因素,促使製造商專注於在所有應用場景中實現客製化和提升用戶舒適度。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 22億美元 |

| 預測金額 | 39億美元 |

| 複合年成長率 | 6.2% |

到2025年,防彈裝備將佔據79.1%的市場。該領域需求強勁,因為它在抵禦子彈和高衝擊力彈丸方面發揮著至關重要的作用。防彈裝備廣泛應用於軍事和執法機關,這些領域經常出現高風險情況。推動該領域成長的因素包括輕質複合材料的進步、結構強度的提高以及穿著舒適度的提升,這些進步使得長時間佩戴也不會影響行動能力。

2025年,最暢銷的細分市場佔據了70.4%的市場。這主要歸功於其在保護上身關鍵部位方面的廣泛應用以及對各種作戰環境的適應性。這些防護系統被國防和保全人員廣泛使用。模組化配置、符合人體工學的設計以及先進彈道材料的不斷改進,提升了防護性能、舒適度和整體易用性,從而支撐了整個終端用戶群的持續需求。

預計到2025年,北美防彈背心市佔率將達到35%。這主要得益於巨額國防費用、先進的製造能力以及新一代防護技術的持續應用。持續增加對提升士兵和執法人員安全的投入,以及防護裝備技術的進步,預計將進一步加速該地區市場的成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球軍費開支增加

- 恐怖主義和犯罪活動的威脅日益加劇

- 材料科學的技術進步

- 對客製化和性別特定盔甲的需求日益成長。

- 民用個人防護工具市場的擴張

- 產業潛在風險與挑戰

- 與高生產成本和可負擔性相關的挑戰

- 與正文全面性相關的問題

- 市場機遇

- 下一代輕型裝甲材料的研發

- 執法機關和國防安全保障機構擴大採用範圍

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 國防預算分析

- 全球國防費用趨勢

- 區域國防預算分配

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 貿易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響(基於初步研究)

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 生產能力和生產趨勢(基於初步調查)

- 各地區及主要生產商的產能

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按銷售額、地區和創新能力分類的層級定位矩陣。

第5章 市場估計與預測:依保護等級分類,2022-2035年

- 防彈保護

- 二級A

- 二級

- 三級A

- 三級

- 四級

- 防止刺傷和尖銳物體傷害

- 防穿刺防彈裝甲

- 穿刺防護盔甲

- 綜合威脅防護(防彈、防穿刺和防利器防護的組合)

第6章 市場估算與預測:依產品類型分類,2022-2035年

- 最好的

- 隱藏式背心

- 開放式戰術背心

- 防彈衣

- 模組化保護系統

- 頭盔

- 戰鬥頭盔

- 防暴頭盔

- 防彈面罩

- 盾

- 攜帶式防彈盾

- 入口護盾

- 配件和附件

- 護襠

- 護頸

- 肩部和三角肌保護器

- 防彈插板和軟防彈衣插板

第7章 市場估計與預測:依最終用戶分類,2022-2035年

- 國防/軍事

- 軍隊

- 海軍

- 空軍

- 陸戰隊

- 特種作戰部隊

- 執法與安保

- 警察局

- 獄警

- 私人保全公司

- 邊防安全和海關

- 私人的

- 個人防護

- 射擊運動訓練

- 記者和非政府相關人員

- 高風險職業勞動者

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- 世界公司

- Point Blank Enterprises

- BAE Systems

- Safariland LLC

- Honeywell International Inc.

- DuPont de Nemours Inc.

- 3M Company

- Teijin Limited

- 該地區頂尖公司

- US Armor Corporation

- Armor Express

- AR500 Armor

- Vestguard(UK)

- 丹麥保育組織(歐洲)

- Indian Armour Systems

- 新興企業

- Safe Life Defense

- BulletSafe

- Spartan Armor Systems

- Hoplite Armor

- RMA Armament

- DFNDR Armor

The Global Body Armor Market was valued at USD 2.2 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 3.9 billion by 2035.

The market is experiencing expansion driven by increasing emphasis on personnel safety and operational effectiveness across defense and security forces worldwide. Growing modernization initiatives within military organizations are encouraging the adoption of advanced protective gear that delivers higher ballistic resistance while maintaining reduced weight for improved mobility and endurance. Rising global security concerns, including terrorism risks and increasing criminal activities, are further intensifying demand for personal protection equipment. Law enforcement agencies are increasingly equipping personnel with advanced protective solutions to safeguard against firearm and edged-weapon threats. At the same time, awareness among civilians regarding personal safety has contributed to growing adoption in high-risk environments. The rising frequency of violent incidents and security threats has reinforced the importance of reliable protective systems. Continuous innovation in materials science has enabled the development of lighter, stronger, and more comfortable protective solutions, improving usability and adoption rates. Proper fit, ergonomic design, and full-body coverage remain critical factors influencing product effectiveness and market acceptance, prompting manufacturers to focus on customization and improved user comfort across applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.2 Billion |

| Forecast Value | $3.9 Billion |

| CAGR | 6.2% |

The ballistic protection segment accounted for 79.1% share in 2025. This segment maintains strong demand due to its essential role in protecting against bullets and high-impact projectiles. It is widely deployed across military and law enforcement applications where high-risk exposure is common. Growth in this segment is supported by advancements in lightweight composites, improved structural strength, and enhanced wearer comfort that allow extended use without compromising mobility.

The vest segment represented 70.4% share in 2025, attributed to widespread use in protecting critical upper-body regions and its adaptability across multiple operational environments. These protective systems are extensively utilized by defense and security personnel. Continuous improvements in modular configurations, ergonomic design, and advanced ballistic materials are enhancing performance, comfort, and overall usability, supporting sustained demand across end-user groups.

North America Body Armor Market accounted for 35% share in 2025 supported by substantial defense spending, advanced manufacturing capabilities, and ongoing integration of next-generation protective technologies. Continuous investments in improving soldier and law enforcement safety, along with technological advancements in protective equipment, are expected to further strengthen regional market expansion.

Key companies operating in the Global Body Armor Industry include DuPont de Nemours Inc., Safariland LLC, BAE Systems, Teijin Limited, Honeywell International Inc., 3M Company, and Point Blank Enterprises. Companies in the Body Armor Market are focusing on advanced material innovation to improve protection levels while reducing weight and enhancing flexibility. Strong investments in research and development are enabling the creation of next-generation composites with superior ballistic resistance and durability. Manufacturers are increasingly forming strategic partnerships with defense agencies and law enforcement organizations to ensure product customization and long-term supply contracts. Expansion of production capacities and adoption of automated manufacturing processes are helping improve efficiency and scalability. Firms are also prioritizing ergonomic improvements and modular armor designs to enhance user comfort and adaptability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Protection level trends

- 2.2.2 Product type trends

- 2.2.3 End-user trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing global military expenditure

- 3.2.1.2 Rising threats of terrorism and criminal activities

- 3.2.1.3 Technological advancements in material science

- 3.2.1.4 Increased demand for customized and gender-specific armor

- 3.2.1.5 Expansion of the civilian market for personal protection

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs and affordability issues

- 3.2.2.2 Body coverage issues

- 3.2.3 Market opportunities

- 3.2.3.1 Development of next-generation lightweight armor materials

- 3.2.3.2 Increasing adoption by law enforcement and homeland security agencies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Defense budget analysis

- 3.9 Global defense spending trends

- 3.10 Regional defense budget allocation

- 3.10.1 North America

- 3.10.2 Europe

- 3.10.3 Asia Pacific

- 3.10.4 Middle East and Africa

- 3.10.5 Latin America

- 3.11 Pricing Analysis (Driven by Primary Research)

- 3.11.1 Historical Price Trend Analysis

- 3.11.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.12 Trade Data Analysis (Based on Paid Database)

- 3.12.1 Import/Export Volume & Value Trends

- 3.12.2 Key Trade Corridors & Tariff Impact

- 3.13 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.13.1 AI-Driven Disruption of Existing Business Models

- 3.13.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.13.3 Risks, Limitations & Regulatory Considerations

- 3.14 Capacity & Production Landscape (Driven by Primary Research)

- 3.14.1 Production Capacity by Region & Key Producer

- 3.14.2 Capacity Utilization Rates & Expansion Pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia-Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By Region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Protection Level, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Ballistic protection

- 5.2.1 Level IIA

- 5.2.2 Level II

- 5.2.3 Level IIIA

- 5.2.4 Level III

- 5.2.5 Level IV

- 5.3 Stab & spike protection

- 5.3.1 Stab-resistant armor

- 5.3.2 Spike-resistant armor

- 5.3.3 Multi-threat protection (combined ballistic/stab/spike)

Chapter 6 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Vests

- 6.2.1 Covert/concealable vests

- 6.2.2 Overt/tactical vests

- 6.2.3 Plate carriers

- 6.2.4 Modular armor systems

- 6.3 Helmets

- 6.3.1 Combat helmets

- 6.3.2 Riot helmets

- 6.3.3 Ballistic face shields

- 6.4 Shields

- 6.4.1 Handheld ballistic shields

- 6.4.2 Breaching shields

- 6.5 Accessories & attachments

- 6.5.1 Groin protectors

- 6.5.2 Neck guards

- 6.5.3 Shoulder & deltoid protection

- 6.5.4 Ballistic inserts & soft armor panels

Chapter 7 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Defense & military

- 7.2.1 Army

- 7.2.2 Navy

- 7.2.3 Air force

- 7.2.4 Marines

- 7.2.5 Special operations forces

- 7.3 Law enforcement & security

- 7.3.1 Police departments

- 7.3.2 Correctional officers

- 7.3.3 Private security firms

- 7.3.4 Border patrol & customs

- 7.4 Civilian

- 7.4.1 Personal protection

- 7.4.2 Shooting sports & training

- 7.4.3 Journalists & NGO workers

- 7.4.4 High-risk professionals

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of MEA

Chapter 9 Company Profiles

- 9.1 Global Players

- 9.1.1 Point Blank Enterprises

- 9.1.2 BAE Systems

- 9.1.3 Safariland LLC

- 9.1.4 Honeywell International Inc.

- 9.1.5 DuPont de Nemours Inc.

- 9.1.6 3M Company

- 9.1.7 Teijin Limited

- 9.2 Regional Champions

- 9.2.1 U.S. Armor Corporation

- 9.2.2 Armor Express

- 9.2.3 AR500 Armor

- 9.2.4 Vestguard (UK)

- 9.2.5 Protection Group Danmark (Europe)

- 9.2.6 Indian Armour Systems

- 9.3 Emerging Players

- 9.3.1 Safe Life Defense

- 9.3.2 BulletSafe

- 9.3.3 Spartan Armor Systems

- 9.3.4 Hoplite Armor

- 9.3.5 RMA Armament

- 9.3.6 DFNDR Armor

2026-2030年全球人體防護裝備市場

2026-2030年全球人體防護裝備市場 防彈背心市場報告:趨勢、預測與競爭分析(至2035年)

防彈背心市場報告:趨勢、預測與競爭分析(至2035年) 車輛裝甲市場商機、成長要素、產業趨勢分析及2026-2035年預測。

車輛裝甲市場商機、成長要素、產業趨勢分析及2026-2035年預測。 防彈板市場:按級別、應用、材料和地區分類

防彈板市場:按級別、應用、材料和地區分類 防彈背心市場規模、佔有率和趨勢分析報告:按防護等級、最終用戶、產品類型、產品款式、地區和細分市場預測(2026-2033 年)

防彈背心市場規模、佔有率和趨勢分析報告:按防護等級、最終用戶、產品類型、產品款式、地區和細分市場預測(2026-2033 年) 防彈背心市場:2026-2032年全球市場預測(依產品類型、材料、防護等級、最終用戶、應用和銷售管道)

防彈背心市場:2026-2032年全球市場預測(依產品類型、材料、防護等級、最終用戶、應用和銷售管道) 2026年全球車輛裝甲市場報告2026年全球防彈輪胎市場報告彈道防護裝備市場:依產品類型、防護等級、材料、最終用戶、應用和通路分類-2026-2032年全球預測高性能囊式幫浦市場:依幫浦類型、材料、流量範圍、壓力範圍、密封類型、應用、通路分類,全球預測(2026-2032)

2026年全球車輛裝甲市場報告2026年全球防彈輪胎市場報告彈道防護裝備市場:依產品類型、防護等級、材料、最終用戶、應用和通路分類-2026-2032年全球預測高性能囊式幫浦市場:依幫浦類型、材料、流量範圍、壓力範圍、密封類型、應用、通路分類,全球預測(2026-2032)