|

市場調查報告書

商品編碼

2038337

2026 年至 2035 年 GPS 追蹤設備的市場機會、成長要素、產業趨勢分析與預測。GPS Tracking Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

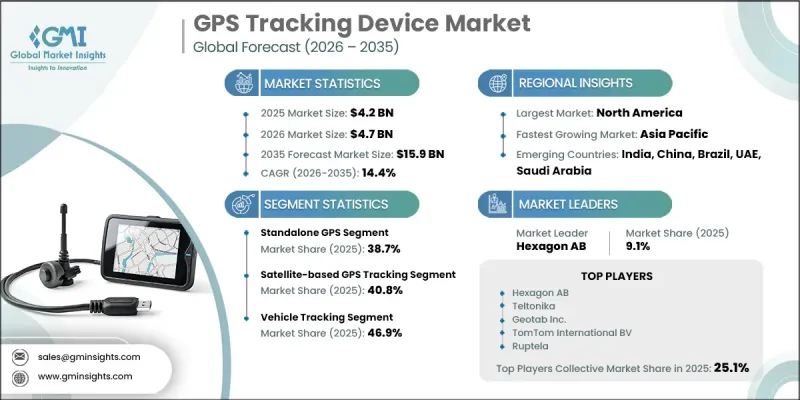

2025 年全球 GPS 追蹤設備市場價值 42 億美元,預計到 2035 年將達到 159 億美元,年複合成長率為 14.4%。

在物流、運輸、零售和醫療產業,對即時定位追蹤的日益依賴正在推動市場成長。受電子商務對快速配送服務需求不斷成長的推動,企業正在採用先進的車輛追蹤解決方案來提高營運效率和客戶體驗。 GPS追蹤系統擴大用於路線最佳化、降低運輸成本和改善配送計劃。在醫療保健領域,追蹤技術在醫療物流、急救運輸和資產監控方面的廣泛應用也進一步促進了市場成長。對昂貴醫療用品被盜和遺失的擔憂也加速了具備即時監控功能的防盜追蹤系統的普及。此外,運輸和物流運營商正擴大整合基於GPS的系統,以實現車輛可視性、路線最佳化和性能監控。隨著向互聯出行和物聯網基礎設施的轉型不斷推進,企業在其價值鍊和服務網路中優先考慮營運透明度和數據驅動的決策,因此相關技術的普及速度正在進一步加快。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 42億美元 |

| 預測金額 | 159億美元 |

| 複合年成長率 | 14.4% |

到2025年,獨立式GPS市佔率將達到38.7%,這主要得益於其在導航、野外作業和基礎資產監控等領域的廣泛應用。其易用性、高可靠性以及無需持續網路依賴即可運作的特性,支撐了這一強勁的市場需求。這些特性使其適用於通訊基礎設施薄弱的偏遠地區,在這些地區,持續的定位精度至關重要。

基於衛星的GPS追蹤技術,即使在偏遠、離岸和地理環境複雜的地區也能提供精準且不間斷的追蹤,預計到2025年將佔據40.8%的市場佔有率。這項技術廣泛應用於需要全球覆蓋和高可靠性的應用領域,例如海事作業、航空和國防。其在遠距離和難以到達的區域提供持續監控的有效性,推動了市場需求的穩定成長。

預計到2025年,北美GPS追蹤設備市佔率將達到36.1%。該地區憑藉其先進的數位基礎設施、物聯網解決方案的高滲透率以及物流和運輸行業追蹤系統的廣泛部署,仍然是GPS技術應用的重要中心。對互聯行動技術的持續投資以及成熟技術供應商的存在,正進一步推動全部區域的市場發展。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 物聯網技術的應用日益廣泛

- 車隊管理解決方案和營運效率提升的需求日益成長

- 我們將專注於安全和監控。

- 電子商務與物流的擴張

- 企業越來越重視提高營運效率和最佳化成本。

- 產業潛在風險與挑戰

- 隱私問題和資料安全

- 初始投資成本高

- 市場機遇

- GPS追蹤技術在保險遠端資訊處理和基於使用量的保險中的廣泛應用。

- 智慧城市概念及互聯基礎建設的擴展

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 貿易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響(基於初步研究)

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按收入、地區和創新能力分類的層級定位矩陣。

第5章 市場估計與預測:依類型分類,2022-2035年

- 獨立式GPS

- 進階追蹤器

- OBD設備

第6章 市場估計與預測:依技術分類,2022-2035年

- 基於衛星的GPS追蹤

- 利用行動電話通訊進行追蹤

- 混合追蹤

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 車輛追蹤

- 車隊管理

- 汽車租賃服務

- 找回被竊車輛

- 資產追蹤

- 設備和機械

- 貨物/運輸

- 個人追蹤

- 老年人和病人的安全

- 健身與運動

- 寵物追蹤

第8章 市場估算與預測:依最終用途產業分類,2022-2035年

- 運輸/物流

- 石油和天然氣

- 建築和重型機械

- 零售與電子商務

- 衛生保健

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- 世界公司

- Hexagon AB

- Teltonika

- Geotab Inc.

- TomTom International BV

- CalAmp Corporation

- Queclink Wireless Solutions Co., Ltd.

- 區域冠軍

- Ruptela

- ATrack Technology Inc.

- Navtelecom LLC

- Meitrack Group

- Shenzhen Jimi IoT Co., Ltd

- SEEWORLD Technology

- 新興企業

- Arusnavi

- WanWayTech

- Trackimo Inc.

- Gosafe Company

- Micodus

- Eelink Communication Technology

The Global GPS Tracking Device Market was valued at USD 4.2 billion in 2025 and is estimated to grow at a CAGR of 14.4% to reach USD 15.9 billion by 2035.

The market is witnessing growth driven by increasing dependence on real-time location tracking across logistics, transportation, retail, and healthcare industries. Rising demand for faster delivery services in e-commerce is encouraging companies to adopt advanced fleet tracking solutions to improve operational efficiency and customer experience. GPS tracking systems are increasingly being used to optimize routing, reduce transportation costs, and improve delivery timelines. In the healthcare sector, growing utilization of tracking technologies for medical logistics, emergency transport, and asset monitoring is further supporting market expansion. Concerns related to theft and loss of high-value medical goods are also accelerating the deployment of anti-theft tracking systems with real-time monitoring capabilities. Additionally, transportation and logistics operators are increasingly integrating GPS-based systems for fleet visibility, route optimization, and performance monitoring. The growing shift toward connected mobility and IoT-enabled infrastructure is further strengthening adoption, as businesses prioritize operational transparency and data-driven decision-making across their supply chain and service networks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.2 Billion |

| Forecast Value | $15.9 Billion |

| CAGR | 14.4% |

The standalone GPS segment accounted for 38.7% share in 2025 owing to its widespread usability in navigation, outdoor operations, and basic asset monitoring applications. Its strong demand is driven by ease of use, high reliability, and the ability to function without continuous network dependency. These characteristics make it suitable for use in remote and low-connectivity environments where consistent positioning accuracy is required.

The satellite-based GPS tracking segment held a 40.8% share in 2025, supported by its ability to deliver accurate and uninterrupted tracking in remote, offshore, and geographically challenging locations. This technology is widely adopted in sectors requiring global coverage and high reliability, including maritime operations, aviation, and defense-related applications. Its effectiveness in providing continuous monitoring across long distances and inaccessible regions is driving steady demand.

North America GPS Tracking Device Market accounted for 36.1% share in 2025. The region remains a leading hub for GPS technology adoption due to its advanced digital infrastructure, strong penetration of IoT solutions, and widespread integration of tracking systems across logistics and transportation industries. Continuous investment in connected mobility technologies and the presence of established technology providers are further supporting market development across the region.

Key companies operating in the GPS Tracking Device Market include Geotab Inc., Hexagon AB, TomTom International BV, Calamp Corporation, Teltonika, Ruptela, SEEWORLD Technology, Arusnavi, and WanWayTech. Companies in the GPS Tracking Device Market are focusing on strengthening their competitive position through continuous innovation in location-based technologies and connectivity solutions. Many players are investing in advanced IoT-enabled tracking systems that offer real-time monitoring, predictive analytics, and enhanced data accuracy. Expansion of cloud-based fleet management platforms is enabling better scalability and remote accessibility for end users. Strategic partnerships with logistics, transportation, and healthcare service providers are helping companies expand their application base. Firms are also focusing on integrating AI and machine learning capabilities to improve route optimization, operational efficiency, and asset utilization. In addition, the development of energy-efficient and compact devices is supporting broader adoption across multiple industries.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Caliber trends

- 2.2.2 Product type trends

- 2.2.3 Guidance mechanism trends

- 2.2.4 End-user application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of IoT technologies.

- 3.2.1.2 Increasing demand for fleet management solutions and operational efficiency.

- 3.2.1.3 Focus on security and surveillance.

- 3.2.1.4 Expansion of e-commerce and logistics.

- 3.2.1.5 Rising focus on operational efficiency and cost optimization in enterprises

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Privacy concerns and data security

- 3.2.2.2 High initial investment cost

- 3.2.3 Market opportunities

- 3.2.3.1 Growing adoption of GPS tracking in insurance telematics and usage-based policies

- 3.2.3.2 Expansion of smart city initiatives and connected infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing Analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Trade Data Analysis (Based on Paid Database)

- 3.9.1 Import/Export Volume & Value Trends

- 3.9.2 Key Trade Corridors & Tariff Impact

- 3.10 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.10.3 Risks, Limitations & Regulatory Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia-Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By Region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Standalone GPS

- 5.3 Advance tracker

- 5.4 OBD device

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Satellite-based GPS tracking

- 6.3 Cellular-based tracking

- 6.4 Hybrid tracking

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Vehicle tracking

- 7.2.1 Fleet management

- 7.2.2 Car rental services

- 7.2.3 Stolen vehicle recovery

- 7.3 Asset tracking

- 7.3.1 Equipment & machinery

- 7.3.2 Cargo & freight

- 7.4 Personal tracking

- 7.4.1 Elderly & patient safety

- 7.4.2 Fitness & sports

- 7.4.3 Pet tracking

Chapter 8 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Transportation & logistics

- 8.3 Oil & gas

- 8.4 Construction & heavy equipment

- 8.5 Retail & e-commerce

- 8.6 Healthcare

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Hexagon AB

- 10.1.2 Teltonika

- 10.1.3 Geotab Inc.

- 10.1.4 TomTom International BV

- 10.1.5 CalAmp Corporation

- 10.1.6 Queclink Wireless Solutions Co., Ltd.

- 10.2 Regional Champions

- 10.2.1 Ruptela

- 10.2.2 ATrack Technology Inc.

- 10.2.3 Navtelecom LLC

- 10.2.4 Meitrack Group

- 10.2.5 Shenzhen Jimi IoT Co., Ltd

- 10.2.6 SEEWORLD Technology

- 10.3 Emerging Players

- 10.3.1 Arusnavi

- 10.3.2 WanWayTech

- 10.3.3 Trackimo Inc.

- 10.3.4 Gosafe Company

- 10.3.5 Micodus

- 10.3.6 Eelink Communication Technology

GPS追蹤設備市場:全球市場預測,2026-2032年

GPS追蹤設備市場:全球市場預測,2026-2032年 GPS追蹤市場報告:趨勢、預測與競爭分析(至2035年)GPS追蹤設備市場:按設備類型、應用、組件、產業垂直領域、國家和地區分類-產業分析、市場規模、市場佔有率和預測(2026-2033年)

GPS追蹤市場報告:趨勢、預測與競爭分析(至2035年)GPS追蹤設備市場:按設備類型、應用、組件、產業垂直領域、國家和地區分類-產業分析、市場規模、市場佔有率和預測(2026-2033年) GPS追蹤器市場:按產品類型、應用程式、最終用戶和地區分類

GPS追蹤器市場:按產品類型、應用程式、最終用戶和地區分類 寵物GPS追蹤設備市場預測-全球分析(依產品類型、寵物種類、連接方式、訂閱模式、價格範圍、技術、應用、通路和地區分類)-2034年

寵物GPS追蹤設備市場預測-全球分析(依產品類型、寵物種類、連接方式、訂閱模式、價格範圍、技術、應用、通路和地區分類)-2034年 GPS追蹤設備市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、部署、最終用戶、功能、安裝類型

GPS追蹤設備市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、部署、最終用戶、功能、安裝類型 2026年全球GPS追蹤設備市場報告

2026年全球GPS追蹤設備市場報告 2026-2034年全球寵物GPS追蹤器市場規模、佔有率、趨勢和成長分析報告全球GPS追蹤設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026-2034年全球寵物GPS追蹤器市場規模、佔有率、趨勢和成長分析報告全球GPS追蹤設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年) GPS追蹤器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、組件、部署類型、垂直產業、地區和競爭格局分類,2021-2031年)

GPS追蹤器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、組件、部署類型、垂直產業、地區和競爭格局分類,2021-2031年)