|

市場調查報告書

商品編碼

2038331

防腐蝕包裝市場:商機、成長要素、產業趨勢分析及2026-2035年預測Anti-Corrosion Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

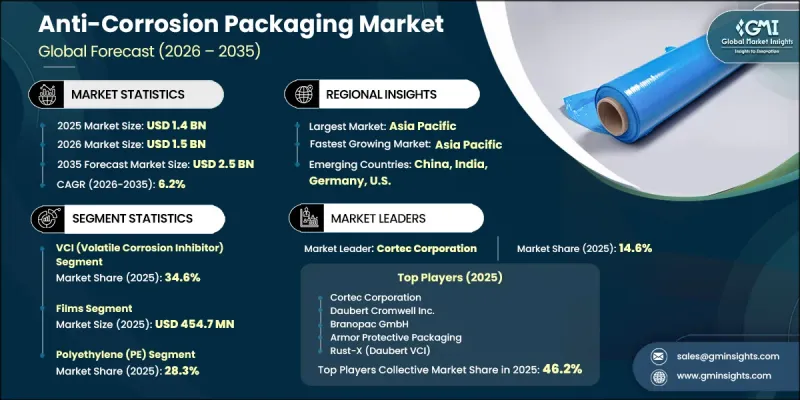

2025 年全球防腐蝕包裝市場價值 14 億美元,預計到 2035 年將以 6.2% 的複合年成長率成長至 25 億美元。

隨著各整體生產規模的成長,對有效防腐蝕解決方案的需求日益成長,以保護金屬零件在儲存和運輸過程中免受腐蝕。隨著全球物流網路的不斷擴展,對能夠保護產品免受潮濕和氧化等環境因素影響的包裝的需求變得愈發重要。各行業越來越重視最大限度地減少產品損壞、降低營運成本並維持產品的耐用性,這加速了先進包裝技術的應用。防護材料和包裝效率的不斷提升進一步增強了產品的可靠性,使防腐蝕解決方案成為現代工業供應鏈中不可或缺的組成部分。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 14億美元 |

| 預計金額 | 25億美元 |

| 複合年成長率 | 6.2% |

金屬零件、機械和電子設備的生產和分銷不斷擴大,這些產品需要強大的防腐蝕劣化市場的發展。隨著全球貿易網路的擴張,貨物擴大暴露於各種環境條件下,增加了運輸和儲存過程中腐蝕的風險。這促使市場對先進包裝解決方案的需求不斷成長,這些解決方案旨在保持產品完整性並延長使用壽命,尤其是在物流要求複雜的行業中。

預計到2035年,混合型和多層包裝系統市場將以7.2%的複合年成長率成長。這些包裝解決方案能夠更好地抵禦環境因素的影響,並適用於嚴苛的物流環境。它們在各種條件下都能保持穩定的性能,因此在對耐用性要求較高的行業中越來越受歡迎,從而推動了其應用範圍的不斷擴大。

預計2026年至2035年,紙張和紙板產業將以8.7%的複合年成長率成長。這一成長主要得益於業界對輕質、可回收和環保包裝解決方案日益成長的需求。紙基防腐蝕材料因其有效的防護性能和符合永續性目標而備受關注。這些材料的廣泛接受反映了在保持性能標準的同時減少環境影響的總體趨勢。

預計到2025年,北美防腐蝕包裝市佔率將達到28.5%。該地區的成長主要得益於強勁的工業活動以及金屬產品在供應鏈中的持續流通,從而不斷提升對防護包裝解決方案的需求。對基礎設施建設、物流能力和先進儲存系統的投資也為市場擴張提供了支持。此外,監管機構對產品品質、減少材料損耗和安全運輸的重視,也推動了全部區域先進包裝技術的應用。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 汽車、金屬和重型機械行業的工業和製造業活動活性化。

- 全球供應鏈的擴張與長途物料運輸

- 電子設備和半導體的出貨量增加,需要採取防腐蝕措施。

- 工業領域對資產保護和降低維護成本的興趣日益濃厚

- 監管機構越來越重視減少材料廢棄物和產品缺陷率。

- 產業潛在風險與挑戰

- 特殊防腐蝕材料高成本

- 對有限的防腐蝕化學品供應商的依賴

- 市場機遇

- 新興市場出口導向製造業的擴張

- 擴大先進VCI化學技術與多層阻隔技術的應用。

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要公司的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興/新創競爭對手的發展趨勢

第5章 市場估計與預測:依技術分類,2022-2035年

- VCI(揮發性防腐劑)

- 非VCI屏障

- 乾燥劑基

- 混合/多層系統

第6章 市場估算與預測:依產品類型分類,2022-2035年

- 電影

- 袋子和小袋

- 挫敗

- 紙張和紙板

- 發送器和裝置

第7章 市場估計與預測:依基材分類,2022-2035年

- 聚乙烯(PE)

- 聚丙烯(PP)

- 鋁箔/金屬箔

- 紙

- 生物基聚合物

第8章 市場估算與預測:依最終用戶應用分類,2022-2035年

- 汽車製造

- 航太/國防

- 電子設備製造

- 重型機械和設備

- 金屬加工和處理

- 建築材料

- 醫療器材與設備

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 全球主要公司

- Cortec Corporation

- Daubert Cromwell Inc.

- Branopac GmbH

- Armor Protective Packaging

- Rust-X(Daubert VCI)

- 按地區分類的主要公司

- 北美洲

- NTIC(Northern Technologies International Corporation)

- Zerust(NTIC brand)

- Transilwrap Company Inc.

- Protective Packaging Corporation

- 3M Company

- 亞太地區

- Aicello Corporation

- Oji F-Tex Co. Ltd.

- Green Packaging Inc.

- 歐洲

- MetPro Group

- Haver Plastics

- 北美洲

The Global Anti-Corrosion Packaging Market was valued at USD 1.4 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 2.5 billion by 2035.

Rising production volumes across manufacturing sectors are driving demand for effective corrosion prevention solutions that protect metal components during storage and transit. As global logistics networks continue to expand, the need for packaging that safeguards against environmental exposure, including moisture and oxidation, is becoming increasingly critical. Industries are placing greater emphasis on minimizing product damage, lowering operational costs, and maintaining durability standards, which is accelerating the adoption of advanced packaging technologies. Continuous improvements in protective materials and packaging efficiency are further enhancing product reliability, making anti-corrosion solutions an essential component of modern industrial supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.5 Billion |

| CAGR | 6.2% |

The anti-corrosion packaging market is further supported by the growing production and distribution of metal components, machinery, and electronic equipment that require reliable protection against degradation. The expansion of global trade networks has increased the exposure of goods to varying environmental conditions, raising the risk of corrosion during transit and storage. This has led to higher demand for advanced protective packaging solutions designed to maintain product integrity and extend lifespan, particularly across industries with complex logistics requirements.

The hybrid and multi-layer systems segment is expected to register a CAGR of 7.2% through 2035. These packaging solutions offer enhanced protection against environmental factors and are well-suited for demanding logistics conditions. Their ability to provide consistent performance under varying conditions has made them increasingly preferred across industries requiring high durability standards, supporting their growing adoption.

The papers and paperboards segment is projected to grow at a CAGR of 8.7% during 2026-2035. This growth is driven by increasing industry focus on lightweight, recyclable, and environmentally responsible packaging solutions. Paper-based anti-corrosion materials are gaining traction due to their effective protection capabilities and alignment with sustainability goals. Their growing acceptance reflects a broader shift toward reducing environmental impact while maintaining performance standards.

North America Anti-Corrosion Packaging Market accounted for 28.5% share in 2025. Growth in the region is driven by strong industrial activity and the continuous movement of metal goods across supply chains, which increases the demand for protective packaging solutions. Investments in infrastructure development, logistics capabilities, and advanced storage systems are supporting market expansion. Additionally, regulatory emphasis on product quality, reduced material loss, and safe transportation is reinforcing the adoption of advanced anti-corrosion packaging technologies across the region.

Key companies operating in the Anti-Corrosion Packaging Market include Cortec Corporation, 3M Company, NTIC (Northern Technologies International Corporation), Zerust (NTIC brand), Daubert Cromwell Inc., Rust-X (Daubert VCI), Branopac GmbH, Armor Protective Packaging, MetPro Group, Aicello Corporation, Oji F-Tex Co. Ltd., Transilwrap Company Inc., Protective Packaging Corporation, Haver Plastics, and Green Packaging Inc. Companies in the Anti-Corrosion Packaging Market are strengthening their competitive position by focusing on innovation in material technology and product performance. They are investing in advanced barrier solutions and multi-layer packaging systems to enhance durability and protection efficiency. Sustainability is becoming a key priority, with increased development of recyclable and environmentally friendly materials. Strategic partnerships and global distribution expansion are helping companies improve market reach and customer accessibility. Businesses are also emphasizing customization to meet specific industry requirements, enabling tailored solutions for different applications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Technology trends

- 2.2.2 Product format trends

- 2.2.3 Base material trends

- 2.2.4 End-user application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising industrial and manufacturing activity across automotive, metals, and heavy machinery

- 3.2.1.2 Expansion of global supply chains and long-distance material movement

- 3.2.1.3 Growth in electronics and semiconductor shipments requiring corrosion-safe handling

- 3.2.1.4 Rising focus on asset protection and reduction of maintenance costs in industrial sectors

- 3.2.1.5 Increasing regulatory emphasis on reducing material waste and product rejection rates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of specialized anti-corrosion materials

- 3.2.2.2 Dependence on limited suppliers of corrosion-inhibiting chemicals

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of export-oriented manufacturing in emerging markets

- 3.2.3.2 Growing adoption of advanced VCI chemistries and multi-layer barrier technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 VCI (volatile corrosion inhibitor)

- 5.3 Non-VCI barrier

- 5.4 Desiccant-based

- 5.5 Hybrid / multi-layer systems

Chapter 6 Market Estimates and Forecast, By Product Format, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Films

- 6.3 Bags & pouches

- 6.4 Foils

- 6.5 Papers & paperboards

- 6.6 Emitters & devices

Chapter 7 Market Estimates and Forecast, By Base Material, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Polyethylene (PE)

- 7.3 Polypropylene (PP)

- 7.4 Aluminum / metal foil

- 7.5 Paper

- 7.6 Bio-based polymers

Chapter 8 Market Estimates and Forecast, By End-User Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Automotive manufacturing

- 8.3 Aerospace & defense

- 8.4 Electronics manufacturing

- 8.5 Heavy machinery & equipment

- 8.6 Metal fabrication & processing

- 8.7 Construction materials

- 8.8 Medical devices & instruments

- 8.9 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Cortec Corporation

- 10.1.2 Daubert Cromwell Inc.

- 10.1.3 Branopac GmbH

- 10.1.4 Armor Protective Packaging

- 10.1.5 Rust-X (Daubert VCI)

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 NTIC (Northern Technologies International Corporation)

- 10.2.1.2 Zerust (NTIC brand)

- 10.2.1.3 Transilwrap Company Inc.

- 10.2.1.4 Protective Packaging Corporation

- 10.2.1.5 3M Company

- 10.2.2 Asia Pacific

- 10.2.2.1 Aicello Corporation

- 10.2.2.2 Oji F-Tex Co. Ltd.

- 10.2.2.3 Green Packaging Inc.

- 10.2.3 Europe

- 10.2.3.1 MetPro Group

- 10.2.3.2 Haver Plastics

- 10.2.1 North America

全球防腐蝕塗料市場:機會與策略展望(至2035年)

全球防腐蝕塗料市場:機會與策略展望(至2035年) 防腐蝕塗料市場-2026-2032年全球市場預測

防腐蝕塗料市場-2026-2032年全球市場預測 防腐蝕塗料市場:預測至2034年-按塗料類型、技術、應用和地區分類的全球分析防腐蝕塗料市場:按類型、樹脂化學性質、技術、基材、產品形式、應用、最終用途產業和銷售管道分類-2026-2032年全球市場預測

防腐蝕塗料市場:預測至2034年-按塗料類型、技術、應用和地區分類的全球分析防腐蝕塗料市場:按類型、樹脂化學性質、技術、基材、產品形式、應用、最終用途產業和銷售管道分類-2026-2032年全球市場預測 全球耐腐蝕橡膠產品市場展望、詳細分析及至 2032 年的預測。奈米工程塗層市場預測至2034年-全球分析(按塗層類型、奈米材料類型、技術、基材類型、應用、最終用戶和地區分類)

全球耐腐蝕橡膠產品市場展望、詳細分析及至 2032 年的預測。奈米工程塗層市場預測至2034年-全球分析(按塗層類型、奈米材料類型、技術、基材類型、應用、最終用戶和地區分類) 防腐蝕塗料市場規模、佔有率和成長分析:按塗料類型、技術、應用、終端用戶產業、基材類型、功能和地區分類-2026-2033年產業預測

防腐蝕塗料市場規模、佔有率和成長分析:按塗料類型、技術、應用、終端用戶產業、基材類型、功能和地區分類-2026-2033年產業預測 全球防腐蝕塗料市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球高性能防腐蝕塗料市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球防腐蝕塗料市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球高性能防腐蝕塗料市場規模、佔有率、趨勢和成長分析報告(2026-2034) 腐蝕防護奈米工程半導體塗層市場分析及預測(至2035年):依類型、產品、服務、技術、應用、材質、製程、最終用戶及功能分類

腐蝕防護奈米工程半導體塗層市場分析及預測(至2035年):依類型、產品、服務、技術、應用、材質、製程、最終用戶及功能分類