|

市場調查報告書

商品編碼

2038309

氮化鋁半導體市場機會、成長要素、產業趨勢分析及2026-2035年預測。Aluminum Nitride (AlN) Semiconductor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

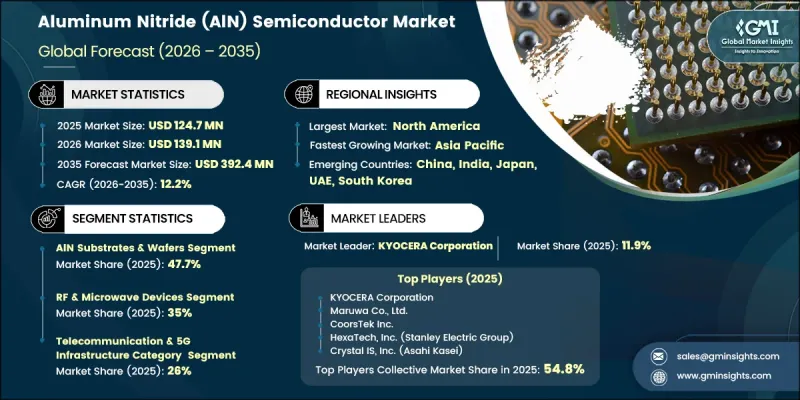

全球氮化鋁半導體市場預計到 2025 年將價值 1.247 億美元,預計到 2035 年將達到 3.924 億美元,年複合成長率為 12.2%。

市場擴張的主要驅動力來自電力電子領域對先進溫度控管材料日益成長的需求、電動車和5G基礎設施中寬能隙半導體技術的廣泛應用,以及高性能射頻和光電裝置整合度的不斷提高。晶圓製造製程和晶體生長製程的持續改進也整體半導體應用領域的市場成長和性能提升起到了至關重要的作用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 1.247億美元 |

| 預計金額 | 3.924億美元 |

| 複合年成長率 | 12.2% |

氮化鋁半導體市場的成長主要受高功率電子系統對高效散熱解決方案日益成長的需求所驅動。一個關鍵趨勢是,高導熱性氮化鋁基基板和陶瓷材料的應用日益廣泛,這主要得益於功率半導體裝置對更高熱控制性能的需求。另一個重要趨勢是單晶氮化鋁晶片在下一代射頻和光電子元件製造中的應用不斷擴大。近年來,隨著製造商致力於提升晶體品質和性能,這一趨勢發展迅速。

由於氮化鋁基基板和晶圓在高功率、高頻電子系統中扮演著至關重要的基礎材料角色,預計到2025年,氮化鋁基板和晶圓市場佔有率將達到47.7%。這些材料因其優異的導熱性、高電絕緣性和晶格相容性而被廣泛應用於射頻技術、電力電子和紫外光電子領域。單晶晶圓製造技術的不斷進步進一步增強了半導體價值鏈的需求,從而推動了其在先進電子系統中的更廣泛應用。

預計2025年,射頻和微波元件領域將佔據35%的市場佔有率,這主要得益於市場對高頻、高功率通訊技術的強勁需求。氮化鋁材料因其高熱穩定性、高介電擊穿電壓以及在嚴苛條件下優異的訊號性能,被廣泛應用於射頻放大器、基地台基礎設施和衛星通訊系統。先進通訊網路的快速部署以及國防通訊系統需求的不斷成長,進一步推動了該領域的成長,並加速了其在高效能電子平台上的應用。

預計到2025年,北美氮化鋁半導體市佔率將達到31.1%。該地區市場成長的主要驅動力是電力電子、5G基礎設施和電動車(EV)應用領域對高效溫度控管材料日益成長的需求。射頻元件、氮化鎵(GaN)基功率系統和先進電子裝置的廣泛應用,顯著推動了美國和加拿大高頻高功率應用中氮化鋁基基板和晶圓的普及。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 電力電子領域對高性能溫度控管的需求日益成長

- 擴大氮化鎵基元件在電動車和5G基礎設施的應用

- 氮化鋁基基板在射頻和高頻應用的廣泛應用

- 增加對先進半導體製造生態系的投資

- 對小型化、高功率密度電子設備的需求日益成長

- 產業潛在風險與挑戰

- 新興國家缺乏工業堆肥基礎設施

- 防潮和防氧性能方面的局限性

- 市場機遇

- 在高功率半導體模組中採用基於氮化鋁的先進封裝技術

- 將氮化鋁整合到下一代寬能隙半導體生態系統中

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢(基於付費資料庫)

- 歷史價格分析(2022-2025)

- 影響價格趨勢的因素

- 區域價格波動

- 價格預測(2026-2035)

- 貿易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 細分市場生成式人工智慧用例和實施藍圖

- 風險、限制和監管考量

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的設備產能

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按收入、地區和創新能力分類的層級定位矩陣。

第5章 市場估算與預測:依產品類型分類,2022-2035年

- AlN基板和晶片

- AlN外延薄膜和層

- 基於氮化鋁的半導體裝置

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 電力電子

- 射頻和微波設備

- 深紫外光電子學

- 壓電和聲波元件

- 其他

第7章 市場估計與預測:依最終用途產業分類,2022-2035年

- 通訊和5G基礎設施

- 汽車和電動車

- 醫療保健和生命科學

- 工業和能源

- 家用電子電器/IT

- 國防/航太

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- 全球主要公司

- KYOCERA Corporation

- Tokuyama Corporation

- CoorsTek Inc.

- CeramTec GmbH

- Morgan Advanced Materials

- Maruwa Co., Ltd.

- 當地公司

- HexaTech, Inc.(Stanley Electric Group)

- Crystal IS, Inc.(Asahi Kasei Corporation)

- Kyma Technologies, Inc.

- Nishimura Advanced Ceramics Co., Ltd.

- Surmet Corporation

- Fraunhofer IISB

- Local Players

- Xiamen Innovacera Advanced Materials Co., Ltd.

- Stanford Advanced Materials

- American Elements

- XI'AN FUNCTION MATERIAL GROUP CO., LTD.

The Global Aluminum Nitride Semiconductor Market was valued at USD 124.7 million in 2025 and is estimated to grow at a CAGR of 12.2% to reach USD 392.4 million by 2035.

Market expansion is driven by rising demand for advanced thermal management materials in power electronics, increasing deployment of wide bandgap semiconductor technologies in electric vehicles and 5G infrastructure, and growing integration of high-performance RF and optoelectronic devices. Continuous improvements in wafer fabrication methods and crystal growth processes are also playing a critical role in supporting market advancement and performance enhancement across semiconductor applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $124.7 Million |

| Forecast Value | $392.4 Million |

| CAGR | 12.2% |

The growth of the aluminum nitride semiconductor market is strongly influenced by the rising need for efficient heat dissipation solutions in high-power electronic systems. Increasing adoption of high thermal conductivity aluminum nitride substrates and ceramic materials is a key trend, driven by the requirement for improved thermal control in power semiconductor devices. Another important development is the rising use of single-crystal aluminum nitride wafers in next-generation RF and optoelectronic component manufacturing, which gained momentum in recent years as manufacturers focused on enhancing crystal quality and performance characteristics.

The aluminum nitride substrates and wafers segment held a 47.7% share in 2025, due to its critical role as a base material in high-power and high-frequency electronic systems. These materials are widely utilized in RF technologies, power electronics, and ultraviolet optoelectronic applications because of their superior thermal conductivity, strong electrical insulation, and lattice compatibility properties. Ongoing advancements in single-crystal wafer production techniques are further strengthening demand across the semiconductor value chain, supporting broader adoption in advanced electronic systems.

The RF and microwave devices segment held a 35% share in 2025, due to strong demand for high-frequency and high-power communication technologies. Aluminum nitride materials are extensively used in RF amplifiers, base station infrastructure, and satellite communication systems because of their high thermal stability, strong breakdown voltage, and excellent signal performance under extreme conditions. The rapid rollout of advanced communication networks and increasing demand for defense communication systems are further supporting segment growth and accelerating adoption across high-performance electronic platforms.

North America Aluminum Nitride Semiconductor Market accounted for 31.1% share in 2025. Regional growth is supported by increasing demand for highly efficient thermal management materials across power electronics, 5G infrastructure, and electric vehicle applications. Expanding use of RF components, gallium nitride-based power systems, and advanced electronic devices is significantly driving the adoption of aluminum nitride substrates and wafers in high-frequency and high-power applications across the United States and Canada.

Major players operating in the Global Aluminum Nitride Semiconductor Industry include KYOCERA Corporation, CeramTec GmbH, CoorsTek Inc., Morgan Advanced Materials, Maruwa Co., Ltd., Tokuyama Corporation, Surmet Corporation, HexaTech, Inc. (Stanley Electric Group), Crystal IS, Inc. (Asahi Kasei Corporation), American Elements, Fraunhofer IISB, Stanford Advanced Materials, Kyma Technologies, Inc., Xiamen Innovacera Advanced Materials Co., Ltd., XI'AN FUNCTION MATERIAL GROUP CO., LTD., and Nishimura Advanced Ceramics Co., Ltd. Key strategies adopted by companies in the Aluminum Nitride Semiconductor Market focus on strengthening crystal growth technologies, expanding high-quality wafer production capacity, and improving thermal conductivity performance for advanced electronic applications. Firms are heavily investing in R&D to enhance single-crystal fabrication techniques and reduce production defects. Strategic collaborations with semiconductor manufacturers and electronics OEMs are helping accelerate commercialization of AlN-based solutions. Companies are also expanding global supply chains to ensure material availability and cost efficiency.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Application trends

- 2.2.3 End-use Industry trends

- 2.2.4 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for high-performance thermal management in power electronics

- 3.2.1.2 Increasing adoption of GaN-based devices in EV and 5G infrastructure

- 3.2.1.3 Expanding use of AlN substrates in RF and high-frequency applications

- 3.2.1.4 Growing investments in advanced semiconductor manufacturing ecosystems

- 3.2.1.5 Rising demand for miniaturized, high-power density electronic devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited industrial composting infrastructure in emerging economies

- 3.2.2.2 Performance limitations in moisture and oxygen barrier properties

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of AlN-based advanced packaging in high-power semiconductor modules

- 3.2.3.2 Integration of AlN in next-generation wide bandgap semiconductor ecosystems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends (Based on paid Database)

- 3.7.1 Historical Price Analysis (2022-2025)

- 3.7.2 Price Trend Drivers

- 3.7.3 Regional Price Variations

- 3.7.4 Price Forecast (2026-2035)

- 3.8 Trade Data Analysis (Based on Paid Database)

- 3.8.1 Import/Export Volume & Value Trends

- 3.8.2 Key Trade Corridors & Tariff Impact

- 3.9 Impact of AI & Generative AI on the Market

- 3.9.1 AI-Driven Disruption of Existing Business Models

- 3.9.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.9.3 Risks, Limitations & Regulatory Considerations

- 3.10 Capacity & Production Landscape (Driven by Primary Research)

- 3.10.1 Installed Capacity by Region & Key Producer

- 3.10.2 Capacity Utilization Rates & Expansion Pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers and acquisitions

- 4.5.2 Partnerships and collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 AlN substrates & wafers

- 5.3 AlN epitaxial films & layers

- 5.4 AlN-based semiconductor devices

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Power electronics

- 6.3 RF & microwave devices

- 6.4 Deep UV optoelectronics

- 6.5 Piezoelectric & acoustic wave devices

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Telecommunications & 5G infrastructure

- 7.3 Automotive & electric vehicles

- 7.4 Healthcare & life sciences

- 7.5 Industrial & energy

- 7.6 Consumer electronics & IT

- 7.7 Defense & aerospace

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 KYOCERA Corporation

- 9.1.2 Tokuyama Corporation

- 9.1.3 CoorsTek Inc.

- 9.1.4 CeramTec GmbH

- 9.1.5 Morgan Advanced Materials

- 9.1.6 Maruwa Co., Ltd.

- 9.2 Regional Players

- 9.2.1 HexaTech, Inc. (Stanley Electric Group)

- 9.2.2 Crystal IS, Inc. (Asahi Kasei Corporation)

- 9.2.3 Kyma Technologies, Inc.

- 9.2.4 Nishimura Advanced Ceramics Co., Ltd.

- 9.2.5 Surmet Corporation

- 9.2.6 Fraunhofer IISB

- 9.3 Local Players

- 9.3.1 Xiamen Innovacera Advanced Materials Co., Ltd.

- 9.3.2 Stanford Advanced Materials

- 9.3.3 American Elements

- 9.3.4 XI'AN FUNCTION MATERIAL GROUP CO., LTD.