|

市場調查報告書

商品編碼

2027673

2026 年至 2035 年非處方藥市場的商業機會、成長要素、產業趨勢分析與預測。Over the Counter (OTC) Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

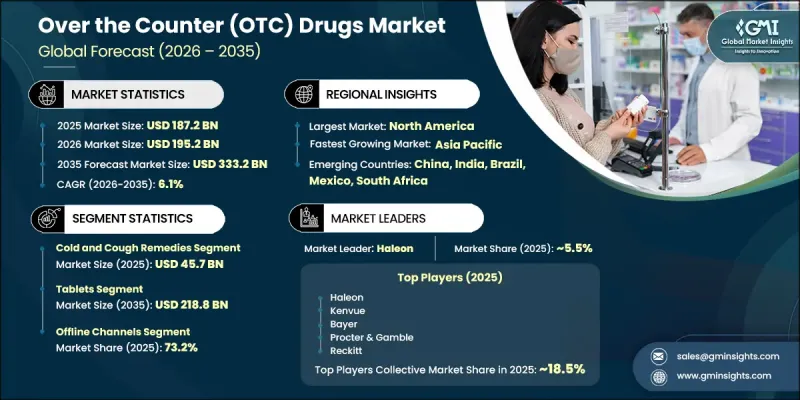

預計到 2025 年,全球非處方藥 (OTC) 市場價值將達到 1,872 億美元,並有望以 6.1% 的複合年成長率成長,到 2035 年達到 3,332 億美元。

這一成長軌跡主要受自我護理轉變的影響,消費者越來越依賴非處方藥 (OTC) 來應對日常健康問題。醫療保健成本的上漲和健康資訊獲取管道的增加,促使人們在無需臨床干預的情況下自行處理輕微症狀。預防醫學和整體健康維護意識的提高,以及人口結構的變化擴大了消費者群體,進一步強化了市場需求。數位和零售平台上的產品供應日益豐富,提高了終端用戶的便利性和可近性,也持續推動市場發展。此外,有利於處方藥向非處方藥過渡的監管支持擴大了產品供應,而競爭性定價策略和學名藥的出現則降低了藥品的價格。安全性和有效性受到監管的非處方藥仍然是自我護理的核心要素,支撐著市場的穩定成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 1872億美元 |

| 預測金額 | 3332億美元 |

| 複合年成長率 | 6.1% |

預計到2025年,感冒咳嗽治療市場規模將達到457億美元,繼續保持主導地位。呼吸道疾病發病率的上升推動了市場需求,因為人們需要快速且方便地緩解症狀。消費者仍傾向於選擇速效的非處方藥,這也促進了該細分市場的持續成長。

預計到2025年,錠劑市場規模將達到1,198億美元,到2035年將達到2,188億美元,進一步鞏固其在劑型領域的領先地位。片劑因其服用方便、劑量精準、易於儲存等優點而廣受歡迎,成為患者自行用藥的理想選擇。新產品的不斷推出和監管部門的持續核准,進一步提升了片劑在各個治療領域的普及率和應用率。

預計到2025年,北美非處方藥(OTC)市佔率將達到31.9%,這反映了其在全球市場的強勢地位。該地區受益於完善的醫療保健體系、較高的自我護理意識以及廣泛的非處方藥供應管道。慢性病和文明病的日益普遍持續支撐著穩定的需求,而先進的零售和數位化分銷管道則正在擴大產品覆蓋範圍並提升消費者參與度。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 消費者對自我治療和疾病管理的意識日益增強

- 處方藥高成本,導致人們轉向使用非處方藥。

- 有利於成藥核准的監管支持

- 產品供應範圍擴大

- 產業潛在風險與挑戰

- 對濫用和藥物濫用的擔憂

- 潛在的副作用和藥物交互作用

- 市場機遇

- 拓展新興市場

- 線上藥局和線上平台的普及和擴張

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 北美洲

- 科技與創新趨勢

- 用於非處方藥的新型藥物遞送系統

- 智慧包裝與病患用藥依從性技術

- 可從處方藥轉換為非處方藥的藥物清單

- 專利趨勢(基於初步調查)

- 自我護理和消費者健康行為趨勢

- 未來市場趨勢(基於初步研究)

- 人工智慧和生成式人工智慧對市場的影響

- 波特的分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依藥品類別分類,2022-2035年

- 感冒咳嗽藥

- 維生素和補充劑

- 消化和腸道藥物

- 皮膚護理

- 止痛藥

- 助眠劑

- 其他藥品類別

第6章 市場估算與預測:依製劑類型分類,2022-2035年

- 藥片

- 液體

- 軟膏

- 噴

第7章 市場估價與預測:依通路分類,2022-2035年

- 線上管道

- 離線頻道

- 醫院藥房

- 零售藥房

- 其他線下通路

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Abbott Laboratories

- Alinamin Pharmaceutical(The Blackstone Group)

- Alkem Laboratories

- Bayer

- Cipla

- Dr. Reddy's Laboratories

- Glenmark Pharmaceuticals

- Haleon

- Himalaya Wellness Company

- Kenvue

- Perrigo Company

- Piramal Pharma

- Procter &Gamble Company

- Reckitt

- Sanofi

- Stada Arzneimittel

- Sun Pharma

- Taisho Pharmaceutical

- Teva Pharmaceutical

The Global Over the Counter Drugs Market was valued at USD 187.2 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 333.2 billion by 2035.

The growth trajectory is shaped by a clear shift toward self-directed healthcare, where consumers increasingly rely on non-prescription medications to address routine health concerns. Rising healthcare costs and broader access to medical information have encouraged individuals to manage minor conditions without clinical intervention. Demand has also strengthened due to heightened awareness around preventive care and general wellness, alongside demographic shifts that expand the consumer base. The market continues to benefit from the growing availability of products across digital and retail platforms, improving accessibility and convenience for end users. In addition, favorable regulatory support enabling prescription-to-non-prescription transitions has widened product availability, while competitive pricing strategies and generic alternatives have improved affordability. Over the counter drugs, regulated for safety and effectiveness, remain a core component of self-care practices, supporting consistent market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $187.2 Billion |

| Forecast Value | $333.2 Billion |

| CAGR | 6.1% |

The cold and cough remedies segment accounted for USD 45.7 billion in 2025, maintaining a leading position within the overall market. Demand is driven by the frequent occurrence of respiratory-related conditions that require quick and accessible symptom management. Consumers continue to prefer readily available non-prescription solutions that provide immediate relief, contributing to sustained segment growth.

The tablets segment generated USD 119.8 billion in 2025 and is projected to reach USD 218.8 billion by 2035, reinforcing its dominance in the dosage form category. Tablets are widely preferred due to their convenience, precise dosage, and ease of storage, making them a practical choice for self-administered treatment. Continuous product introductions and regulatory approvals have further strengthened their availability and adoption across various therapeutic categories.

North America Over the Counter Drugs Market held a share of 31.9% in 2025, reflecting its strong position in the global landscape. The region benefits from well-established healthcare systems, high awareness of self-care practices, and widespread access to a diverse range of non-prescription medications. The increasing prevalence of chronic and lifestyle-related conditions continues to support consistent demand, while advanced retail and digital distribution channels enhance product reach and consumer engagement.

Key companies operating in the Over The Counter Drugs Market include Abbott Laboratories, Bayer, Cipla, Haleon, Kenvue, Reckitt, Sanofi, Perrigo Company, Procter & Gamble Company, Teva Pharmaceutical, Dr. Reddy's Laboratories, Sun Pharma, Glenmark Pharmaceuticals, Himalaya Wellness Company, Piramal Pharma, Alkem Laboratories, Taisho Pharmaceutical, Stada Arzneimittel, and Alinamin Pharmaceutical (The Blackstone Group). Companies in the Over the Counter Drugs Market are strengthening their competitive position through continuous product innovation, portfolio expansion, and strategic regulatory approvals. They are investing in research and development to introduce advanced formulations that enhance efficacy, safety, and convenience for consumers. Expanding digital presence through e-commerce platforms and pharmacy applications is improving product accessibility and customer engagement. Firms are also leveraging branding, targeted marketing, and consumer education initiatives to build trust and increase awareness. Strategic partnerships, mergers, and acquisitions enable companies to broaden their geographic footprint and distribution networks. Additionally, a strong focus on cost optimization, private-label offerings, and sustainable packaging solutions is helping organizations align with evolving consumer preferences and regulatory expectations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 Regional trends

- 2.2.3 Drug category trends

- 2.2.4 Formulation type trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing consumer awareness for self-medication and disease management

- 3.2.1.2 High cost of prescription drugs leading to shift towards OTC drugs

- 3.2.1.3 Favorable regulatory support for OTC drug approvals

- 3.2.1.4 Expanding product accessibility

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Concerns regarding misuse or drug abuse

- 3.2.2.2 Potential side effects and drug interactions

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging markets expansion

- 3.2.3.2 Increasing penetration and adoption of e-pharmacies and online platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology/innovation landscape

- 3.5.1 Novel drug delivery systems for OTC products

- 3.5.2 Smart packaging & patient adherence technologies

- 3.6 Prescription to nonprescription switch list

- 3.7 Patent landscape (Driven by Primary Research)

- 3.8 Self-care & consumer health behavior trends

- 3.9 Future market trends (Driven by Primary Research)

- 3.10 Impact of AI and generative AI on the market

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Category, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Cold and cough remedies

- 5.3 Vitamins and supplements

- 5.4 Digestive and intestinal remedies

- 5.5 Skin treatment

- 5.6 Analgesics

- 5.7 Sleeping aids

- 5.8 Other drug categories

Chapter 6 Market Estimates and Forecast, By Formulation Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Tablets

- 6.3 Liquids

- 6.4 Ointments

- 6.5 Sprays

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Online channels

- 7.3 Offline channels

- 7.3.1 Hospital pharmacies

- 7.3.2 Retail pharmacies

- 7.3.3 Other offline channels

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Alinamin Pharmaceutical (The Blackstone Group)

- 9.3 Alkem Laboratories

- 9.4 Bayer

- 9.5 Cipla

- 9.6 Dr. Reddy’s Laboratories

- 9.7 Glenmark Pharmaceuticals

- 9.8 Haleon

- 9.9 Himalaya Wellness Company

- 9.10 Kenvue

- 9.11 Perrigo Company

- 9.12 Piramal Pharma

- 9.13 Procter & Gamble Company

- 9.14 Reckitt

- 9.15 Sanofi

- 9.16 Stada Arzneimittel

- 9.17 Sun Pharma

- 9.18 Taisho Pharmaceutical

- 9.19 Teva Pharmaceutical

寵物藥局和藥品傳遞平台市場預測至2034年-按產品類型、輸送平台、服務模式、最終用戶和地區分類的全球分析寵物護膚及皮膚科產品市場預測至2034年-按產品類型、寵物品種、分銷管道、應用、最終用戶和地區分類的全球分析

寵物藥局和藥品傳遞平台市場預測至2034年-按產品類型、輸送平台、服務模式、最終用戶和地區分類的全球分析寵物護膚及皮膚科產品市場預測至2034年-按產品類型、寵物品種、分銷管道、應用、最終用戶和地區分類的全球分析 維生素B2市場-全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局(2021-2031年)2034年非處方藥市場預測-按產品、劑型、給藥途徑、通路、最終用戶和地區分類的全球分析非處方藥市場-全球產業規模、佔有率、趨勢、機會與預測:按產品、劑型、地區和競爭格局分類,2021-2031年

維生素B2市場-全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局(2021-2031年)2034年非處方藥市場預測-按產品、劑型、給藥途徑、通路、最終用戶和地區分類的全球分析非處方藥市場-全球產業規模、佔有率、趨勢、機會與預測:按產品、劑型、地區和競爭格局分類,2021-2031年 非處方藥市場:2026 年至 2032 年全球市場預測,依產品、產品類型、劑型、包裝、使用頻率、通路和疾病細分。非處方藥市場:2026-2032 年全球市場以藥物類型、劑型、通路、年齡層和最終用戶預測。

非處方藥市場:2026 年至 2032 年全球市場預測,依產品、產品類型、劑型、包裝、使用頻率、通路和疾病細分。非處方藥市場:2026-2032 年全球市場以藥物類型、劑型、通路、年齡層和最終用戶預測。 非處方胃腸道藥物市場:按藥物類別、適應症、最終用戶和地區分類(2026-2034 年)非處方藥市場規模、佔有率、趨勢和預測:按產品類型、給藥途徑、劑型、分銷管道和地區分類,2026-2034 年。

非處方胃腸道藥物市場:按藥物類別、適應症、最終用戶和地區分類(2026-2034 年)非處方藥市場規模、佔有率、趨勢和預測:按產品類型、給藥途徑、劑型、分銷管道和地區分類,2026-2034 年。 非處方外用抗真菌藥物市場:按產品類型、活性成分、應用、使用者、分銷管道和地區分類

非處方外用抗真菌藥物市場:按產品類型、活性成分、應用、使用者、分銷管道和地區分類