|

市場調查報告書

商品編碼

2027655

食品級親水膠體市場機會、成長要素、產業趨勢分析及2026-2035年預測Food Hydrocolloids Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

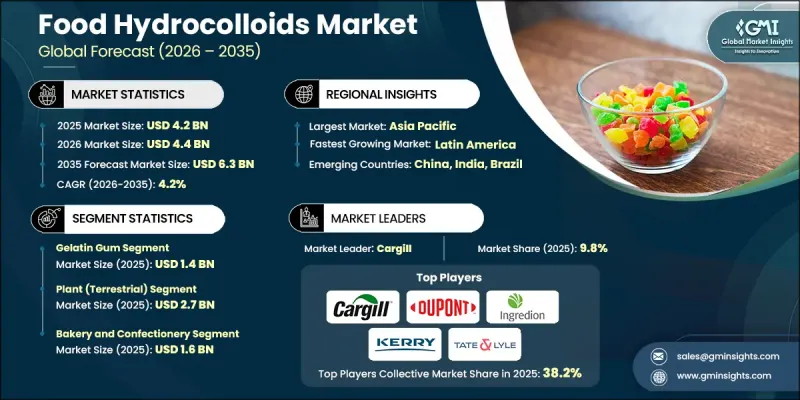

全球食品親水膠體市場預計到 2025 年將價值 42 億美元,預計到 2035 年將以 4.2% 的複合年成長率成長至 63 億美元。

隨著加工食品對能夠改善質地、穩定性和延長保存期限的功能性配料的需求不斷成長,全球食品親水膠體行業正經歷著穩步成長。食品親水膠體整體用作膠凝劑、增稠劑和穩定劑,來源包括植物、動物、微生物和海藻。這些配料在改善食品系統的黏度和結構穩定性方面發揮著至關重要的作用,是烘焙產品、糖果甜點、乳製品和飲料等應用領域不可或缺的成分。它們能夠在各種溫度條件、pH值和機械應力下保持性能,這進一步拓展了它們在室溫和冷藏食品中的應用。此外,消費者對「潔淨標示」配料的日益偏好也推動了市場需求,因為親水膠體無需使用合成添加劑即可提供天然功能。萃取和純化技術的進步進一步提高了產品質量,使得對分子結構和性能特徵的控制更加精確。酶處理和可控水解技術的結合使生產商能夠調節凝膠強度和黏度等功能特性,從而拓展了其在現代食品配方中的潛在應用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 42億美元 |

| 預測金額 | 63億美元 |

| 複合年成長率 | 4.2% |

由於其優異的凝膠性能和廣泛的應用範圍,預計到2025年,明膠市場規模將達到14億美元。該細分市場因其熱可逆性而備受青睞,使其適用於糖果甜點、乳製品和製藥等領域。加工技術的不斷改進使製造商能夠開發出具有客製化凝膠強度的明膠,以滿足不同的配方需求。同時,果膠等植物來源親水膠體因其在低糖和水果基應用中的適用性而日益受到關注,尤其是在潔淨標示產品的開發方面。

預計到2025年,植物來源食品市場規模將達到27億美元,這主要得益於消費者對純素食產品和天然成分的需求不斷成長。隨著食品生產商順應潔淨標示趨勢和消費者對植物來源配方的偏好,該品類將持續成長。雖然動物源性親水膠體在某些應用中仍然很重要,但植物來源替代品正在多個食品類別中擴大其市場佔有率。海藻源性親水膠體也迅速普及,尤其是在乳製品和肉品配方中用於穩定劑和凝膠形成方面。

北美食品親水膠體市場預計將從2025年的12億美元成長到2035年的18億美元,主要成長動力來自消費者對潔淨標示成分的日益青睞以及對天然食品配方策略的關注度不斷提高。食品製造商正在加速向植物來源成分和透明的成分體系轉型,以滿足消費者的期望。植物來源食品的成長,以及乳製品替代品、烘焙產品和機能飲料中對天然穩定劑需求的不斷增加,進一步推動了全部區域市場的發展。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 明膠

- 果膠

- 黃原膠

- 瓜爾膠

- 鹿角菜膠

- 其他

第6章 市場估計與預測:依來源分類,2022-2035年

- 植物(陸生)

- 動物

- 海藻/海洋

- 合成/改性

- 微生物來源

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 麵包糖果甜點

- 乳製品和冷凍食品

- 飲料

- 肉類和水產品

- 其他用途

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Ashland Global Holdings Inc.

- Cargill, Incorporated

- CP Kelco

- DuPont de Nemours, Inc.

- FMC Corporation

- Gum Technology Corporation

- Ingredion Incorporated

- Kerry Group plc

- Koninklijke DSM NV

- Lonza Group AG

- Tate & Lyle PLC

- TIC Gums, Inc.

The Global Food Hydrocolloids Market was valued at USD 4.2 billion in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 6.3 billion by 2035.

The global food hydrocolloids industry is witnessing steady growth as demand increases for functional ingredients that enhance texture, stability, and shelf life across processed food products. Food hydrocolloids are widely used as gelling, thickening, and stabilizing agents derived from plant, animal, microbial, and seaweed sources. These ingredients play a vital role in improving viscosity and structural integrity in food systems, making them essential across bakery, confectionery, dairy, and beverage applications. Their ability to maintain performance under varying thermal conditions, pH levels, and mechanical stress further strengthens their use in both ambient and chilled food products. Increasing consumer preference for clean-label ingredients is also driving demand, as hydrocolloids provide natural functionality without synthetic additives. Advancements in extraction and purification technologies are further enhancing product quality, enabling better control over molecular structure and performance characteristics. The integration of enzymatic processing and controlled hydrolysis techniques is allowing manufacturers to tailor functional properties such as gel strength and viscosity, thereby expanding application potential across modern food formulations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.2 Billion |

| Forecast Value | $6.3 Billion |

| CAGR | 4.2% |

The gelatin gum segment accounted for USD 1.4 billion in 2025 owing to its strong gelling performance and wide applicability. This segment is highly valued for its thermoreversible properties, making it suitable for confectionery, dairy, and pharmaceutical uses. Ongoing improvements in processing techniques have enabled manufacturers to develop gelatin with customized bloom strength levels to meet diverse formulation requirements. At the same time, plant-based hydrocolloids such as pectin are gaining traction due to their suitability in low-sugar and fruit-based applications, particularly within clean-label product development.

The plant-derived segment captured USD 2.7 billion in 2025, supported by increasing demand for vegan-friendly and naturally sourced ingredients. This category continues to grow as food manufacturers align with clean-label trends and consumer preference for plant-based formulations. While animal-derived hydrocolloids remain important in certain applications, plant-based alternatives are expanding their presence across multiple food categories. Seaweed-based hydrocolloids are also witnessing strong adoption, particularly in stabilization and gel formation applications across dairy and meat product formulations.

North America Food Hydrocolloids Market is projected to grow from USD 1.2 billion in 2025 to USD 1.8 billion by 2035 driven by the rising adoption of clean-label ingredients and increased focus on natural food formulation strategies. Food manufacturers are increasingly shifting toward plant-based and transparent ingredient systems to align with consumer expectations. The growth of plant-based food products, combined with rising demand for natural stabilizers in dairy alternatives, bakery goods, and functional beverages, is further supporting market development across the region.

Key companies operating in the Global Food Hydrocolloids Market include Ingredion Incorporated, Kerry Group plc, Tate & Lyle PLC, Cargill, FMC Corporation, DuPont de Nemours, Inc., CP Kelco, Koninklijke DSM N.V., Lonza Group AG, Ashland Global Holdings Inc., Gum Technology Corporation, and TIC Gums, Inc. Companies in the Food Hydrocolloids Market are focusing on strategic initiatives to strengthen their market position and expand global reach. A key focus is investment in research and development to enhance functional performance, improve stability, and expand application versatility across food systems. Manufacturers are developing advanced extraction and modification technologies to achieve precise control over viscosity, gel strength, and texture properties. Strategic collaborations with food and beverage producers are helping companies tailor solutions to evolving formulation needs. Expansion of production capacities and modernization of processing facilities are supporting rising demand for clean-label ingredients. Companies are also prioritizing sustainability by sourcing raw materials responsibly and reducing environmental impact in production processes. Product innovation in plant-based and seaweed-derived hydrocolloids is further strengthening portfolio diversification. In addition, mergers, acquisitions, and global expansion strategies are enabling firms to improve market access, strengthen distribution networks, and enhance competitive positioning across regional markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Form

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Gelatin Gum

- 5.3 Pectin

- 5.4 Xanthan Gum

- 5.5 Guar Gum

- 5.6 Carrageenan

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Plant (Terrestrial)

- 6.3 Animal

- 6.4 Seaweed/Marine

- 6.5 Synthetic/Modified

- 6.6 Microbial

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bakery and Confectionery

- 7.3 Dairy and Frozen Products

- 7.4 Beverages

- 7.5 Meat and Seafood Products

- 7.6 Other Applications

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Ashland Global Holdings Inc.

- 9.2 Cargill, Incorporated

- 9.3 CP Kelco

- 9.4 DuPont de Nemours, Inc.

- 9.5 FMC Corporation

- 9.6 Gum Technology Corporation

- 9.7 Ingredion Incorporated

- 9.8 Kerry Group plc

- 9.9 Koninklijke DSM N.V.

- 9.10 Lonza Group AG

- 9.11 Tate & Lyle PLC

- 9.12 TIC Gums, Inc.