|

市場調查報告書

商品編碼

2027648

生義式麵食及義大利麵市場機會、成長要素、產業趨勢分析及2026-2035年預測Uncooked Pasta and Noodles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

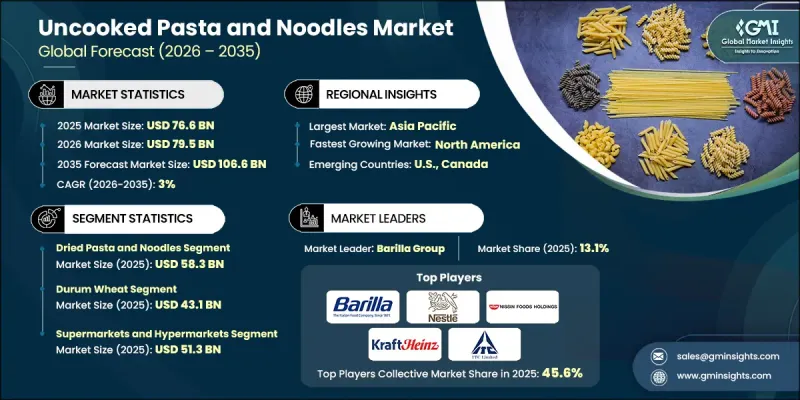

2025 年全球未煮熟的義式麵食和麵條市場價值為 766 億美元,預計到 2035 年將以 3% 的複合年成長率成長至 1066 億美元。

義式麵食和義大利麵是麵團類食品,由小麥粉或其他穀物粉與水混合製成,有時會添加雞蛋和鹽。之後,它們被塑形並乾燥以備儲存,或新鮮包裝後直接烹飪。這些產品在世界各地的飲食文化中廣泛食用;義式麵食與歐洲飲食文化緊密相連,而麵條則深深植根於亞洲飲食文化。乾燥的麵條和義大利麵適合長期儲存且易於烹飪,因為它在煮熟前保持一定的嚼勁,煮熟後則會變軟。硬質小麥粗麵粉因其高蛋白含量而被廣泛用於義式麵食的生產,這有助於麵條在烹飪後保持其嚼勁和彈性。麵條的生產原料種類繁多,包括米粉和蕎麥粉,取決於地區的偏好和烹飪方法。乾燥過程在降低水分含量、延長保存期限和防止微生物滋生方面起著至關重要的作用,同時也有助於高效的運輸和全球分銷。生產技術的不斷進步正在進一步提高整個產業的品質一致性、加工效率和產品多樣性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 766億美元 |

| 預測金額 | 1066億美元 |

| 複合年成長率 | 3% |

預計到2025年,乾義式麵食和麵條市場規模將達到583億美元。與其他形式的食品相比,乾意麵和麵條保存期限更長、價格更實惠、易於儲存,因此持續佔據市場主導地位。其便利性和多功能性使其成為家庭烹飪和餐飲服務業的必備食材,支撐著住宅和商用消費管道的穩定需求。

預計2025年,硬質小麥市場規模將達431億美元。由於其高蛋白含量和優異的成面能力,硬質小麥被廣泛用於義式麵食生產,從而賦予義大利麵理想的口感和烹飪性能。將硬質小麥粗麵粉粗磨後,可以生產出結構緊實、烹飪過程中不易變形的義式麵食,確保其具有傳統義式麵食麵特有的嚼勁和口感。

生義式麵食市場的主要企業包括日清食品控股、卡夫亨氏、百味來集團、東洋水產、雀巢、ITC、聯合利華、金寶湯、Ebro Foods、Treehouse Foods、De Cecco 和 Jovial Foods。這些企業的主要策略在於透過配方創新(例如義式麵食、無麩質和營養強化)來拓展產品系列,以滿足不斷變化的消費者偏好。製造商正加大對先進生產技術的投資,以改善產品的質地一致性、保存期限和烹飪性能。透過零售和線上通路策略性地拓展分銷網路,可以增強全球覆蓋範圍並提高產品供應。此外,企業也專注於品牌建立和優質化策略,以在競爭激烈的市場中脫穎而出。與餐飲服務商和零售連鎖店的合作有助於提升銷售量和市場滲透率。同時,企業也致力於永續的穀物採購,並努力改進包裝解決方案,以在滿足環保要求的同時延長保存期限。持續加大研發投入,使得更多針對特定地區的產品變體得以開發,以滿足世界各地不同的飲食文化和消費者偏好。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 對價格實惠的主食需求不斷成長,正在推動市場擴張。

- 餐飲業和快餐店的成長正在推動大眾消費。

- 都市區成長帶動了加工食品銷售的成長。

- 陷阱與挑戰

- 小麥價格波動給製造商的利潤率帶來了壓力。

- 供應鏈中斷會影響原料的穩定供應。

- 機會

- 由於可以長期儲存,因此易於大規模。

- 客製化產品以迎合當地口味有可能擴大基本客群。

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按形式

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 乾義大利義式麵食和麵條

- 室溫罐裝義大利義式麵食和麵條

- 冷藏冷凍的義式麵食和麵條

第6章 市場估算與預測:依原料分類,2022-2035年

- 粗粒小麥粉

- 麵粉

- 硬粒小麥

- 其他

第7章 市場估價與預測:依通路分類,2022-2035年

- 超級市場和大賣場

- 便利商店

- 線上零售

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Barilla Group

- Nestle

- ITC

- Kraft Heinz Company

- Unilever

- Toyo Suisan Kaisha

- Nissin Foods Holdings

- Campbell Soup Company

- TreeHouse Foods

- Ebro Foods

- De Cecco

- Jovial Foods

The Global Uncooked Pasta and Noodles Market was valued at USD 76.6 billion in 2025 and is estimated to grow at a CAGR of 3% to reach USD 106.6 billion by 2035.

Uncooked pasta and noodles are dough-based food products prepared from wheat flour or other grain flours blended with water, and in some cases eggs or salt, which are then shaped and preserved through drying or packaged in fresh form for later cooking. These products are widely consumed across global cuisines, with pasta strongly linked to European dietary traditions and noodles deeply rooted in Asian food cultures. The dry form retains a firm structure that softens only after boiling, making it suitable for long-term storage and easy preparation. Durum wheat semolina is widely used in pasta production due to its high protein content, which helps maintain firmness and elasticity after cooking. Noodles are produced using a broader range of raw materials, including rice-based and buckwheat-based flours, depending on regional preferences and culinary practices. The drying process plays a vital role in reducing moisture content, extending shelf life, and preventing microbial growth, while also supporting efficient transportation and global distribution. Ongoing advancements in production technologies are further improving quality consistency, processing efficiency, and product variety across the industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $76.6 Billion |

| Forecast Value | $106.6 Billion |

| CAGR | 3% |

The dried pasta and noodles segment reached USD 58.3 billion in 2025. This category continues to dominate the market due to its long shelf stability, cost-effectiveness, and ease of storage compared to alternative forms. Its convenience and versatility have made it a staple in household cooking as well as foodservice operations, supporting consistent demand across both residential and commercial consumption channels.

The durum wheat segment reached USD 43.1 billion in 2025. This raw material is widely used in pasta manufacturing due to its high protein content and strong gluten-forming properties, which contribute to desirable texture and cooking performance. The coarse milling of durum wheat semolina enables the production of pasta with a firm structure that holds its shape during cooking, ensuring the characteristic bite and texture associated with traditional pasta products.

The key companies operating in the Uncooked Pasta and Noodles Market include Nissin Foods Holdings, Kraft Heinz Company, Barilla Group, Toyo Suisan Kaisha, Nestle, ITC, Unilever, Campbell Soup Company, Ebro Foods, TreeHouse Foods, De Cecco, and Jovial Foods. Key strategies adopted by companies in the Uncooked Pasta and Noodles Market focus on expanding product portfolios through innovation in ingredient composition, including high-protein, gluten-free, and enriched formulations to meet evolving dietary preferences. Manufacturers are increasingly investing in advanced production technologies to enhance texture consistency, shelf life, and cooking performance. Strategic expansion of distribution networks across retail and online channels is strengthening global reach and improving product accessibility. Companies are also emphasizing branding and premiumization strategies to differentiate offerings in a competitive market. Partnerships with foodservice providers and retail chains are helping to increase volume sales and market penetration. Additionally, firms are focusing on sustainable sourcing of grains and improving packaging solutions to extend shelf stability while aligning with environmental expectations. Continuous investment in R&D is further enabling the development of region-specific product variations to cater to diverse culinary traditions and consumer preferences worldwide.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Form

- 2.2.2 Raw Material

- 2.2.3 Distribution Channel

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for affordable staple foods drives market expansion

- 3.2.1.2 Growth in food service and quick-service restaurants boosts bulk consumption

- 3.2.1.3 Rising urban populations support higher packaged food sales

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 Volatile wheat prices pressure manufacturer margins

- 3.2.2.2 Supply chain disruptions affect raw material stability

- 3.2.3 Opportunities

- 3.2.3.1 Long shelf life supports large-scale distribution and exports

- 3.2.3.2 Regional flavor customization can expand consumer base

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By form

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Dried pasta and noodles

- 5.3 Ambient/canned pasta and noodles

- 5.4 Chilled/frozen pasta and noodles

Chapter 6 Market Estimates and Forecast, By Raw Material, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Semolina

- 6.3 Flour

- 6.4 Durum wheat

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Supermarkets and hypermarkets

- 7.3 Convenience stores

- 7.4 Online retail

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Barilla Group

- 9.2 Nestle

- 9.3 ITC

- 9.4 Kraft Heinz Company

- 9.5 Unilever

- 9.6 Toyo Suisan Kaisha

- 9.7 Nissin Foods Holdings

- 9.8 Campbell Soup Company

- 9.9 TreeHouse Foods

- 9.10 Ebro Foods

- 9.11 De Cecco

- 9.12 Jovial Foods