|

市場調查報告書

商品編碼

2027646

飛機點火系統市場機會、成長要素、產業趨勢分析及2026-2035年預測Aircraft Ignition System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

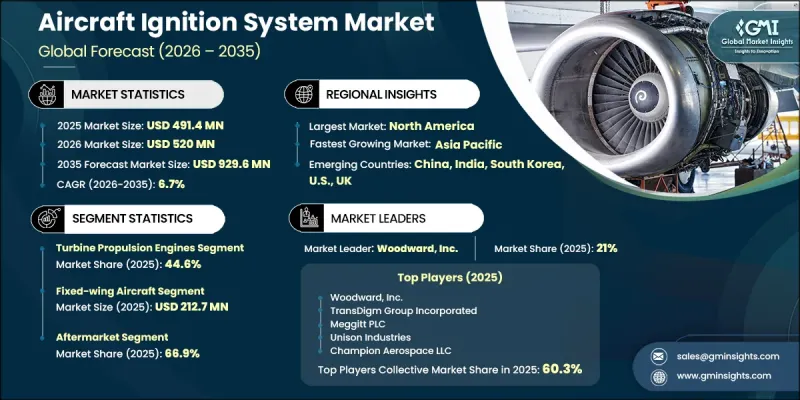

全球飛機點火系統市場預計到 2025 年將達到 4.914 億美元,年複合成長率為 6.7%,到 2035 年將達到 9.296 億美元。

隨著航空業相關人員致力於提升引擎效率、運作可靠性和長期性能,航空市場正經歷穩定成長。窄體飛機產量增加和飛機運轉率上升,為先進點火解決方案創造了穩定的需求。航空公司和營運商優先考慮機隊升級,逐步以更有效率的電子系統取代傳統點火技術。點火系統與數位引擎控制架構的整合,進一步提升了系統的精度和響應速度。此外,飛機電氣化程度的提高,也推動了能夠降低機械複雜性並支援節能運作的點火系統的應用。持續的維護週期和零件更換也促進了售後市場的持續需求。點火系統設計的技術進步,提高了耐久性,減輕了系統重量,並最佳化了燃油效率,這些因素共同增強了飛機點火系統市場的長期前景。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 4.914億美元 |

| 預計金額 | 9.296億美元 |

| 複合年成長率 | 6.7% |

預計到2025年,渦輪推進引擎市場佔有率將達到44.6%,憑藉其在需要高性能點火系統的飛機平台上的廣泛應用,繼續保持主導地位。這些系統設計用於在嚴苛條件下運行,確保引擎點火的穩定性和可靠性。飛機產量和營運週期的不斷成長持續推動著該細分市場的發展,進而帶動了對堅固耐用點火部件的需求。高安全標準和嚴格的性能要求也進一步促進了該細分市場的持續應用。

預計到2025年,固定翼飛機市場規模將達到2.127億美元,主要得益於其在全球機隊中的廣泛應用。該細分市場受益於飛機產量高、交付持續以及頻繁、長時間的運行,這些都對可靠的點火系統提出了更高的要求。此外,對引擎性能穩定性、符合嚴格的航空法規以及與不斷發展的引擎技術相容的需求也進一步推動了市場需求。憑藉其龐大的營運規模和持續的技術升級,該細分市場將繼續在市場成長中發揮核心作用。

預計到2025年,北美飛機點火系統市場佔有率將達到36.3%,這反映出該地區強勁的需求,而不斷變化的法規和技術進步也為其提供了支撐。市場擴張的原因在於,人們越來越關注引擎效率、減少排放氣體和最佳化維護。飛機運營商正在向先進的點火系統過渡,這些系統能夠提供更高的性能、更少的磨損和更高的燃油效率。對航空基礎設施和現代化項目的持續投資也進一步推動了該地區的市場成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球整機製造商窄體飛機產量增加

- 飛機現代化改造,以取代過時的磁電機點火系統

- 廉價航空公司的發展導致航班數量增加。

- 亞太地區區域航空市場擴張

- FADEC技術的普及提高了對先進點火系統的需求。

- 產業潛在風險與挑戰

- 高昂的認證門檻延緩了新產品的核准。

- OEM合約期限的延長限制了供應商的進入。

- 市場機遇

- 固態點火系統取代傳統磁電機系統

- 由於全球飛機機身老化,售後市場需求增加。

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要公司的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與發展(R&D)

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興/新創競爭對手的發展趨勢

第5章 市場估計與預測:依系統類型分類,2022-2035年

- 電子點火系統

- 磁電機點火系統

- 等離子點火系統

- 混合型/其他

第6章 市場估計與預測:依組件分類,2022-2035年

- 興奮劑

- 點火控制單元

- 渦輪點火系統

- 活塞火星塞

- 點火導線/電纜

- 其他

第7章 市場估算與預測:依引擎類型分類,2022-2035年

- 渦輪推進引擎

- 往復式推進引擎

- 輔助電源系統

第8章 市場估算與預測:依平台分類,2022-2035年

- 固定翼飛機

- 旋翼飛機

- 動力無人機(UAV)

第9章 市場估計與預測:依技術成熟度分類,2022-2035年

- 傳統點火系統

- 先進點火系統

第10章 市場估價與預測:依應用領域分類,2022-2035年

- OEM

- 售後市場

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 全球主要公司

- Honeywell International Inc.

- Woodward, Inc.

- TransDigm Group Incorporated

- Meggitt PLC

- Unison Industries

- Champion Aerospace LLC

- 按地區分類的主要公司

- 北美洲

- Electroair

- Hartzell Engine Technologies

- Kelly Aerospace, Inc.

- G3i Ignition

- 亞太地區

- Sky Dynamics Corporation

- 歐洲

- Continental Aerospace Technologies

- 北美洲

- 特殊玩家/干擾者

- Tempest Aero Group

- SureFly Partners Ltd.

- Aero Accessories, Inc.

The Global Aircraft Ignition System Market was valued at USD 491.4 million in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 929.6 million by 2035.

The market is witnessing steady expansion as aviation stakeholders focus on improving engine efficiency, operational reliability, and long-term performance. Increasing production of narrow-body aircraft, combined with rising aircraft utilization rates, is creating consistent demand for advanced ignition solutions. Airlines and operators are prioritizing fleet upgrades, leading to the gradual replacement of conventional ignition technologies with more efficient electronic systems. The integration of ignition systems with digital engine control architectures is further enhancing system precision and responsiveness. Additionally, the transition toward more electric aircraft is encouraging the adoption of ignition systems that reduce mechanical complexity and support energy-efficient operations. Continuous maintenance cycles and component replacements are also contributing to sustained aftermarket demand. Technological advancements in ignition design are improving durability, reducing system weight, and enabling better fuel optimization, which collectively strengthen the long-term outlook of the aircraft ignition system market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $491.4 Million |

| Forecast Value | $929.6 Million |

| CAGR | 6.7% |

The turbine propulsion engines segment held a share of 44.6% in 2025, maintaining its leading position due to its widespread deployment across aviation platforms requiring high-performance ignition systems. These systems are designed to operate under demanding conditions, ensuring consistent and reliable engine ignition. The segment continues to benefit from ongoing aircraft production and increasing operational cycles, which drive the need for robust and durable ignition components. High safety standards and stringent performance requirements further support continuous adoption within this segment.

The fixed-wing aircraft segment generated USD 212.7 million in 2025, driven by its extensive presence across global aviation fleets. The segment benefits from high aircraft volumes, continuous deliveries, and frequent long-duration operations that necessitate dependable ignition systems. Demand is reinforced by the need for consistent engine performance, compliance with strict aviation regulations, and compatibility with evolving engine technologies. The segment remains central to market growth due to its operational scale and continuous technological upgrades.

North America Aircraft Ignition System Market accounted for 36.3% share in 2025, reflecting strong regional demand supported by regulatory advancements and technological adoption. The market in this region is expanding due to increasing focus on engine efficiency, emissions reduction, and maintenance optimization. Operators are transitioning toward advanced ignition systems that deliver improved performance, reduced wear, and enhanced fuel efficiency. Continued investments in aviation infrastructure and modernization programs further strengthen regional market growth.

Key companies operating in the Aircraft Ignition System Industry include Honeywell International Inc., TransDigm Group Incorporated, Woodward, Inc., Unison Industries, Meggitt PLC, Champion Aerospace LLC, Hartzell Engine Technologies, Kelly Aerospace, Inc., Aero Accessories, Inc., Continental Aerospace Technologies, Electroair, Tempest Aero Group, G3i Ignition, Sky Dynamics Corporation, and SureFly Partners Ltd. Companies in the Aircraft Ignition System Market are focusing on innovation, strategic partnerships, and product advancement to strengthen their competitive position. Many players are investing in the development of lightweight, high-efficiency ignition systems that integrate seamlessly with digital engine platforms. Expanding aftermarket services and maintenance solutions is another key strategy to ensure recurring revenue streams. Companies are also forming collaborations with aircraft manufacturers and engine developers to secure long-term supply agreements. Geographic expansion into emerging aviation markets is helping firms capture new growth opportunities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 System type trends

- 2.2.2 Component trends

- 2.2.3 Engine type trends

- 2.2.4 Platform trends

- 2.2.5 Technology maturity trends

- 2.2.6 End-use trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising narrow-body aircraft production across global OEMs

- 3.2.1.2 Fleet modernization replacing legacy magneto ignition systems

- 3.2.1.3 Growth in low-cost carriers boosting flight frequencies

- 3.2.1.4 Expansion of regional aviation in Asia-Pacific markets

- 3.2.1.5 FADEC integration increasing demand for advanced ignition systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High certification barriers delaying new product approvals

- 3.2.2.2 Long OEM contract cycles limiting supplier entry

- 3.2.3 Market opportunities

- 3.2.3.1 Solid-state ignition systems replacing traditional magneto systems

- 3.2.3.2 Aftermarket demand from aging global aircraft fleet

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By System Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Electronic ignition system

- 5.3 Magneto ignition system

- 5.4 Plasma ignition system

- 5.5 Hybrid / others

Chapter 6 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Exciters

- 6.3 Ignition control units

- 6.4 Turbine igniters

- 6.5 Piston spark plugs

- 6.6 Ignition leads / cables

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Engine Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Turbine propulsion engines

- 7.3 Reciprocating propulsion engines

- 7.4 Auxiliary power systems

Chapter 8 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Fixed-wing aircraft

- 8.3 Rotary-wing aircraft

- 8.4 Unmanned aerial vehicles (UAVs) - engine-based

Chapter 9 Market Estimates and Forecast, By Technology Maturity, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Conventional ignition systems

- 9.3 Advanced ignition systems

Chapter 10 Market Estimates and Forecast, By End-use, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 Original equipment manufacturer (OEM)

- 10.3 Aftermarket

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Honeywell International Inc.

- 12.1.2 Woodward, Inc.

- 12.1.3 TransDigm Group Incorporated

- 12.1.4 Meggitt PLC

- 12.1.5 Unison Industries

- 12.1.6 Champion Aerospace LLC

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 Electroair

- 12.2.1.2 Hartzell Engine Technologies

- 12.2.1.3 Kelly Aerospace, Inc.

- 12.2.1.4 G3i Ignition

- 12.2.2 Asia Pacific

- 12.2.2.1 Sky Dynamics Corporation

- 12.2.3 Europe

- 12.2.3.1 Continental Aerospace Technologies

- 12.2.1 North America

- 12.3 Niche Players/Disruptors

- 12.3.1 Tempest Aero Group

- 12.3.2 SureFly Partners Ltd.

- 12.3.3 Aero Accessories, Inc.

飛機點火系統市場-2026-2032年全球市場預測

飛機點火系統市場-2026-2032年全球市場預測 飛機點火系統市場分析及預測(至2035年):類型、產品、技術、組件、應用、最終用戶、功能、安裝方式、設備

飛機點火系統市場分析及預測(至2035年):類型、產品、技術、組件、應用、最終用戶、功能、安裝方式、設備 無人機點火系統市場報告:趨勢、預測與競爭分析(至2035年)

無人機點火系統市場報告:趨勢、預測與競爭分析(至2035年) 2026年全球航太及工業點火系統及飛機點火系統市場報告2026年全球航空點火系統市場報告

2026年全球航太及工業點火系統及飛機點火系統市場報告2026年全球航空點火系統市場報告 飛機點火系統市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測全球飛機點火系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

飛機點火系統市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測全球飛機點火系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 飛機點火系統市場規模、佔有率和成長分析(按類型、組件、引擎類型、平台、最終用戶和地區分類)—產業預測(2026-2033 年)

飛機點火系統市場規模、佔有率和成長分析(按類型、組件、引擎類型、平台、最終用戶和地區分類)—產業預測(2026-2033 年) 飛機點火系統市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、組件、引擎類型、地區和競爭格局分類,2020-2030年預測

飛機點火系統市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、組件、引擎類型、地區和競爭格局分類,2020-2030年預測