|

市場調查報告書

商品編碼

2027645

暖通空調閥門市場機會、成長要素、產業趨勢分析及2026-2035年預測HVAC Valve Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

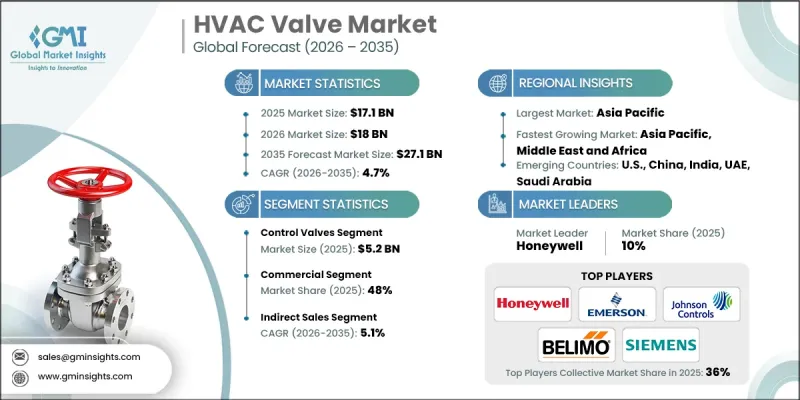

全球暖通空調閥門市場預計到 2025 年價值 171 億美元,預計到 2035 年將達到 271 億美元,年複合成長率為 4.7%。

市場擴張的驅動力主要來自節能型暖通空調系統的日益普及以及住宅和商業領域建設活動的成長。人們對降低能源消耗和排放的日益關注,加速了對需要高性能閥門的先進暖通空調系統的需求。技術進步,特別是物聯網和人工智慧在暖通空調系統中的應用,也促進了市場成長,實現了即時監控和控制,從而降低了營運成本。此外,政府為促進節能而推出的優惠政策、獎勵和法規,也推動了最新暖通空調解決方案的廣泛應用。都市化、可支配收入的成長以及對更智慧的大樓自動化系統的需求,進一步推動了暖通空調閥門市場的發展,預計該市場在預測期內將保持強勁成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 171億美元 |

| 預測金額 | 271億美元 |

| 複合年成長率 | 4.7% |

預計到 2025 年,控制閥市場規模將達到 52 億美元,到 2035 年將以 5.2% 的複合年成長率成長。控制閥在現代 HVAC 系統中發揮著至關重要的作用,它們能夠精確調節溫度和壓力,從而提高系統的整體性能和能源效率。

預計到2025年,商業領域將佔據48%的市場佔有率,並預計在2026年至2035年間以5%的複合年成長率成長。辦公大樓、零售商店和醫療機構等商業空間的擴張正在推動對節能型暖通空調系統的需求。都市化、可支配收入的成長以及智慧建築系統的普及正在推動該領域的持續成長,而家庭自動化趨勢也帶動了住宅對先進暖通空調閥門的需求持續成長。

預計到2025年,美國暖通空調閥門市場將佔據80%的市場佔有率,市場規模將達到38億美元。這一快速成長主要得益於對節能型暖通空調系統、先進建築自動化技術以及有利氣候條件(尤其是在南部各州)的需求。德克薩斯州和佛羅裡達州等州的快速都市化和不斷成長的建築需求也顯著推動了美國市場的發展。暖通空調閥門產業的主要參與者包括KITZ Corporation、Flowserve、Schneider Electric、Verimo、 Honeywell、江森自控、Obentrop、西門子建築科技、Taco Comfort Solutions、艾默生(Fischer)、KSB、Neway Valve、Samson和Watts Water Technologies。暖通空調閥門市場的企業正在採取多種策略來鞏固其市場地位。他們專注於開發可與物聯網和人工智慧系統整合的節能型智慧閥門解決方案。拓展分銷網路、與暖通空調系統整合商合作以及與建設公司合作,有助於他們進入更廣泛的市場。投資研發高性能、低維護、永續的閥門產品有助於滿足不斷變化的能源效率標準。企業重視售後服務、技術支援和客製化解決方案,以提升客戶滿意度。此外,併購和地理擴張是確保長期市場地位和競爭力的關鍵策略。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 監理情勢

- 能源效率標準(ASHRAE 90.1,歐盟 ErP 指令)

- 建築標準法與安全條例

- 符合環境法規(RoHS、REACH)

- 關鍵市場趨勢與轉型

- 科技與創新趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析(基於初步研究)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 貿易數據分析(基於付費資料庫)

- 進出口數量和價值的變化趨勢(基於初步調查)

- 主要貿易走廊及關稅影響(基於初步調查)

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依閥門類型分類,2022-2035年

- 球閥

- 球閥

- 蝶閥

- 單向閥

- 閘閥

- 安全閥

- 控制閥

- 電磁閥

- 其他(例如:碟閥等)

第6章 市場估計與預測:依營運方式分類,2022-2035年

- 手動的

- 氣動

- 油壓

- 電的

- 智慧/互聯

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 暖氣系統

- 冷卻系統

- 通風系統

- 區域供冷

- 冷凍

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 住宅

- 商業的

- 辦公大樓

- 零售

- 飯店業

- 衛生保健

- 其他(教育機構等)

- 工業的

- 石油和天然氣

- 製造業

- 食品/飲料

- 其他(藥品等)

第9章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- Belimo

- Caleffi

- Emerson(Fisher)

- Flowserve

- Honeywell

- Johnson Controls

- KITZ Corporation

- KSB

- Neway Valve

- Oventrop

- Samson

- Schneider Electric

- Siemens Building Technologies

- Taco Comfort Solutions

- Watts Water Technologies

The Global HVAC Valve Market was valued at USD 17.1 billion in 2025 and is estimated to grow at a CAGR of 4.7% to reach USD 27.1 billion by 2035.

The market is expanding due to the rising adoption of energy-efficient HVAC systems and increasing construction activities across residential and commercial sectors. Growing emphasis on reducing energy consumption and emissions has accelerated the demand for advanced HVAC systems, which require high-performance valves. Technological advancements, particularly the integration of IoT and AI in HVAC systems, have also fueled market growth, enabling real-time monitoring and control, which reduces operational costs. Additionally, favorable government policies, incentives, and regulations promoting energy efficiency are encouraging widespread adoption of modern HVAC solutions. The combination of urbanization, rising disposable incomes, and demand for smarter building automation systems is further driving the HVAC valve market forward, positioning it in a strong growth phase over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.1 Billion |

| Forecast Value | $27.1 Billion |

| CAGR | 4.7% |

In 2025, the control valves segment generated USD 5.2 billion and is projected to grow at a CAGR of 5.2% through 2035. Control valves are critical in modern HVAC systems because they allow precise regulation of temperature and pressure, enhancing overall system performance and energy efficiency.

The commercial segment held a 48% share in 2025 and is expected to grow at a CAGR of 5% from 2026 to 2035. Expansion in commercial spaces, including offices, retail environments, and healthcare facilities, is fueling the demand for energy-efficient HVAC systems. Urbanization, higher disposable income, and technological adoption in smart building systems are driving sustained growth in this segment, while residential demand for advanced HVAC valves continues to rise alongside home automation trends.

United States HVAC Valve Market held an 80% share in 2025, generating USD 3.8 billion. Rapid expansion is driven by demand for energy-saving HVAC systems, advanced building automation technologies, and favorable climate conditions, particularly in southern states. Rapid urbanization and construction growth in states like Texas and Florida are significant contributors to the U.S. market's development. Key players in the HVAC Valve Industry include KITZ Corporation, Flowserve, Schneider Electric, Belimo, Caleffi, Honeywell, Johnson Controls, Oventrop, Siemens Building Technologies, Taco Comfort Solutions, Emerson (Fisher), KSB, Neway Valve, Samson, and Watts Water Technologies. Companies in the HVAC Valve Market are implementing multiple strategies to strengthen their presence and market position. They focus on developing energy-efficient and smart valve solutions that integrate with IoT and AI systems. Expansion of distribution networks, partnerships with HVAC system integrators, and collaborations with construction firms allow broader market access. Investment in R&D for high-performance, low-maintenance, and sustainable valve products helps meet evolving energy efficiency standards. Firms emphasize after-sales services, technical support, and customized solutions to enhance customer satisfaction. Additionally, mergers, acquisitions, and geographic expansion are key strategies used to secure a long-term market foothold and competitiveness.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Valve type trends

- 2.2.3 Operation type trends

- 2.2.4 Application trends

- 2.2.5 End user trends

- 2.2.6 Distribution channel trends

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Energy Efficiency Standards (ASHRAE 90.1, EU ErP Directive)

- 3.4.2 Building Codes & Safety Regulations

- 3.4.3 Environmental Compliance (RoHS, REACH)

- 3.5 Major market trends and disruptions

- 3.6 Technological and innovation landscape

- 3.6.1 Emerging technologies

- 3.7 Pricing analysis (Driven by Primary Research)

- 3.7.1 Historical price trend analysis (Driven by Primary Research)

- 3.7.2 Pricing strategy by player type (Premium / Value / Cost-plus) (Driven by Primary Research)

- 3.8 Trade data analysis (Driven by Paid Data Base)

- 3.8.1 Import/export volume & value trends (Driven by Primary Research)

- 3.8.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 GenAI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Valve Type, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Ball valves

- 5.3 Globe valves

- 5.4 Butterfly valves

- 5.5 Check valves

- 5.6 Gate valves

- 5.7 Pressure relief valves

- 5.8 Control valves

- 5.9 Solenoid valves

- 5.10 Others (disc valves etc.)

Chapter 6 Market Estimates & Forecast, By Operation Type, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Pneumatic

- 6.4 Hydraulic

- 6.5 Electric

- 6.6 Smart/connected

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Heating systems

- 7.3 Cooling systems

- 7.4 Ventilation systems

- 7.5 District cooling

- 7.6 Refrigeration

Chapter 8 Market Estimates & Forecast, By End User, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Office buildings

- 8.3.2 Retail

- 8.3.3 Hospitality

- 8.3.4 Healthcare

- 8.3.5 Others (educational institute etc.)

- 8.4 Industrial

- 8.4.1 Oil and gas

- 8.4.2 Manufacturing

- 8.4.3 Food and beverages

- 8.4.4 Others (pharmaceuticals etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Belimo

- 11.2 Caleffi

- 11.3 Emerson (Fisher)

- 11.4 Flowserve

- 11.5 Honeywell

- 11.6 Johnson Controls

- 11.7 KITZ Corporation

- 11.8 KSB

- 11.9 Neway Valve

- 11.10 Oventrop

- 11.11 Samson

- 11.12 Schneider Electric

- 11.13 Siemens Building Technologies

- 11.14 Taco Comfort Solutions

- 11.15 Watts Water Technologies

2026年全球牛心包瓣膜市場報告

2026年全球牛心包瓣膜市場報告 2026-2030年全球閥門市場

2026-2030年全球閥門市場 低溫控制閥市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年石油和天然氣閥門市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、閥體材料、尺寸、地區和競爭格局分類,2021-2031年輪胎氣門銷市場 - 全球產業規模、佔有率、趨勢、機會與預測:按車輛類型、需求類別、地區和競爭格局分類,2021-2031年

低溫控制閥市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年石油和天然氣閥門市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、閥體材料、尺寸、地區和競爭格局分類,2021-2031年輪胎氣門銷市場 - 全球產業規模、佔有率、趨勢、機會與預測:按車輛類型、需求類別、地區和競爭格局分類,2021-2031年 醫用歧管市場:按產品類型、材質、應用、最終用戶和地區分類閥門市場:按閥門類型、材料類型、驅動方式、分銷管道、最終用戶和地區分類

醫用歧管市場:按產品類型、材質、應用、最終用戶和地區分類閥門市場:按閥門類型、材料類型、驅動方式、分銷管道、最終用戶和地區分類 分流閥市場:按類型、操作方式、材質、壓力等級、連接方式、尺寸和應用分類-2026-2032年全球市場預測旋轉閥市場:2026-2032年全球市場預測(依產品類型、閥門類型、材質、類別、工作模式、壓力等級、尺寸、應用、最終用戶產業和銷售管道)閥襯市場:2026-2032年全球市場預測(按閥門類型、襯裡材料、連接方式、壓力等級、應用和最終用途行業分類)

分流閥市場:按類型、操作方式、材質、壓力等級、連接方式、尺寸和應用分類-2026-2032年全球市場預測旋轉閥市場:2026-2032年全球市場預測(依產品類型、閥門類型、材質、類別、工作模式、壓力等級、尺寸、應用、最終用戶產業和銷售管道)閥襯市場:2026-2032年全球市場預測(按閥門類型、襯裡材料、連接方式、壓力等級、應用和最終用途行業分類)