|

市場調查報告書

商品編碼

2027621

腳輪市場機會、成長要素、產業趨勢分析及2026-2035年預測。Casters Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

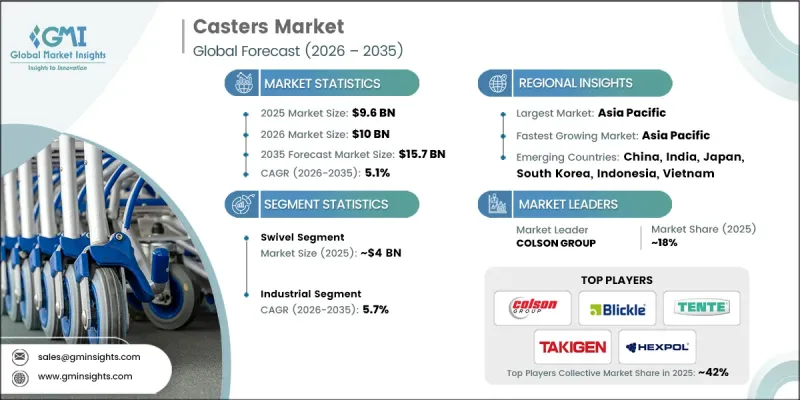

2025年全球腳輪市場價值為96億美元,預計2035年將以5.1%的複合年成長率成長至157億美元。

全球物流網路、物料輸送系統和工業基礎設施的快速擴張推動了市場成長。倉庫、生產設施和配送中心對高效貨物運輸的需求日益成長,顯著促進了基於腳輪的行動解決方案的普及。此外,電子商務的持續發展加速了履約中心的建設,行動裝置在提升營運效率方面發揮著至關重要的作用。企業越來越重視採用能夠承受重載和持續使用的耐用高性能移動組件。同時,製造環境正向靈活模組化的生產系統演進,從而促進了行動工作站和設備的使用。這種轉變推動了堅固耐用的腳輪在工業設備中的應用。此外,減少人工勞動和簡化工作流程的需求不斷成長,進一步推動了市場需求,使腳輪市場成為現代工業和物流生態系統中不可或缺的組成部分。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 96億美元 |

| 預測金額 | 157億美元 |

| 複合年成長率 | 5.1% |

預計到2025年,旋轉腳輪市場規模將達到40億美元,並在2035年之前以5.8%的複合年成長率成長。該細分市場憑藉其高度的柔軟性和在各種應用中易於移動的特點,正在推動腳輪市場的發展。旋轉腳輪可實現全方位旋轉,使設備能夠以最小的力氣在多個方向上平穩運作。其適應性使其適用於各種對精度和操控性要求極高的應用。對符合人體工學的設備和高效搬運解決方案日益成長的需求,持續推動著該細分市場的成長,並進一步鞏固了其強大的市場地位。

預計到2025年,工業領域將佔據41.6%的市場佔有率,並在2026年至2035年間以5.7%的複合年成長率成長。該領域之所以佔據市場主導地位,是因為在嚴苛的作業環境下,對高承載能力的行動解決方案有著迫切的需求。工業腳輪的設計旨在承受巨大的負載,經受惡劣環境的考驗,並長期保持性能穩定。其耐用性、耐磨性和在各種表面上的適用性,使其成為大規模作業中不可或缺的工具。持續的工業化進程、倉儲自動化以及基礎設施的擴張,將繼續推動該領域的強勁需求。

預計到2025年,中國腳輪市場規模將達到12億美元,到2035年將以6.4%的複合年成長率成長,這主要得益於製造業、物流業和大型分銷系統的快速發展。對高效物料輸送方案日益成長的需求,推動了高性能腳輪在工業和商業領域的應用。國內產能也不斷增強,重點在於開發耐用且滿足不斷變化的營運需求的專用產品。有組織的零售業、醫療基礎設施和物流設施的成長,也進一步促進了市場需求的成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 擴大物料輸送和物流運營

- 製造工廠自動化和行動裝置應用的擴展

- 醫療基礎設施擴建及醫療設備利用

- 陷阱與挑戰

- 在惡劣的工業環境中承受巨大的磨損

- 全球及區域製造商之間的競爭異常激烈。

- 機會

- 對符合人體工學、低噪音移動解決方案的需求日益成長

- 開發具有追蹤和負載容量監控功能的智慧腳輪

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析(基於初步研究)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 各地區價格波動

- 貿易數據分析(基於付費資料庫)

- 進出口數量和價值趨勢(基於初步調查)

- 主要貿易路線及關稅的影響(基於初步調查)

- 主要進口國和出口國

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 旋轉

- 剛性/固定

- 滾珠軸承

- 黑幫老大

第6章 市場估計與預測:依材料分類,2022-2035年

- 金屬

- 橡皮

- 塑膠

- 聚氨酯

第7章 市場估計與預測:依負載容量,2022-2035年

- 小型

- 中號

- 大的

第8章 市場估算與預測:依安裝方式分類,2022-2035年

- 盤子

- 幹

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 工業的

- 商業的

- 衛生保健

- 住宅

第10章 市場估價與預測:依最終用途分類,2022-2035年

- 車

- 航太

- 食品工業

- 醫療保健

- 紡織業

- 其他最終用途

第11章 市場估價與預測:依通路分類,2022-2035年

- 直接地

- 間接

第12章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第13章:公司簡介

- Blickle

- Cebora

- COLSON GROUP

- Er Wagner

- Flywheel Metalwork

- Hamilton Caster

- Hexpol

- Payson Casters

- Regal Castors

- RWM Casters

- Takigen

- Tellure

- TENTE

- TrioPines

- ZONWE

The Global Casters Market was valued at USD 9.6 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 15.7 billion by 2035.

Market growth is fueled by the rapid expansion of logistics networks, material handling systems, and industrial infrastructure across global economies. Increasing demand for efficient movement of goods within warehouses, production facilities, and distribution hubs is significantly boosting the adoption of caster-based mobility solutions. The continued rise of e-commerce is accelerating the development of fulfillment centers, where mobile equipment plays a crucial role in operational efficiency. Businesses are increasingly prioritizing durable and high-performance mobility components that can handle heavy loads and continuous usage. At the same time, manufacturing environments are evolving toward flexible and modular production systems, driving the use of mobile workstations and equipment. This shift is encouraging the integration of robust and long-lasting casters into industrial setups. Additionally, the growing emphasis on reducing manual labor and improving workflow efficiency is further strengthening demand, positioning the casters market as a vital component of modern industrial and logistics ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.6 Billion |

| Forecast Value | $15.7 Billion |

| CAGR | 5.1% |

The swivel segment generated USD 4 billion in 2025 and is expected to grow at a CAGR of 5.8% through 2035. This segment leads the casters market due to its high level of flexibility and ease of movement across diverse applications. Swivel casters enable full rotational movement, allowing equipment to be maneuvered smoothly in multiple directions with minimal effort. Their adaptability makes them suitable for a wide range of uses where precision and mobility are essential. Increasing demand for ergonomic equipment and efficient handling solutions continues to support segment growth, reinforcing its strong market position.

The industrial segment accounted for 41.6% share in 2025 and is projected to grow at a CAGR of 5.7% between 2026 and 2035. This segment dominates due to the need for heavy-duty mobility solutions in demanding operational environments. Industrial casters are engineered to support substantial loads, endure harsh conditions, and maintain performance over extended periods. Their durability, resistance to wear, and ability to function across different surfaces make them essential in large-scale operations. Ongoing industrialization, warehouse automation, and infrastructure expansion continue to drive strong demand in this segment.

China Casters Market captured USD 1.2 billion in 2025 and is anticipated to grow at a CAGR of 6.4% through 2035, supported by rapid growth in manufacturing, logistics, and large-scale distribution systems. Increasing reliance on efficient material handling solutions is encouraging widespread adoption of high-performance casters across industrial and commercial environments. Domestic production capabilities are also strengthening, with a focus on developing durable and application-specific products that meet evolving operational requirements. Growth in organized retail, healthcare infrastructure, and logistics facilities further contributes to rising demand.

Key companies operating in the Global Casters Market include Blickle, Colson Group, TENTE, Hamilton Caster, RWM Casters, Takigen, Tellure, Regal Castors, Payson Casters, TrioPines, ZONWE, Er Wagner, Hexpol, Flywheel Metalwork, and Cebora. Companies in the casters market are focusing on innovation, durability, and customization to strengthen their competitive position. Manufacturers are investing in advanced materials and engineering techniques to improve load capacity, wear resistance, and overall product lifespan. Expanding product portfolios to cater to specialized industrial requirements is also a key priority. Strategic partnerships and distribution expansion are helping companies enhance market reach and customer accessibility. Firms are increasingly emphasizing ergonomic design and safety features to align with workplace efficiency standards. Additionally, integration with automated systems and smart manufacturing environments is becoming a focal point, enabling companies to stay competitive in a rapidly evolving industrial landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Material

- 2.2.4 Load capacity

- 2.2.5 Mounting

- 2.2.6 Application

- 2.2.7 End use

- 2.2.8 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of material handling and logistics operations

- 3.2.1.2 Rising adoption of automation and mobile equipment in manufacturing facilities

- 3.2.1.3 Growth of healthcare infrastructure and medical equipment usage

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High wear and tear in heavy-duty industrial environments

- 3.2.2.2 Intense price competition among global and regional manufacturers

- 3.2.3 Opportunities

- 3.2.3.1 Growing demand for ergonomic and low-noise mobility solutions

- 3.2.3.2 Development of smart casters with tracking and load monitoring capabilities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.9.3 Regional price variations

- 3.10 Trade data analysis (driven by paid database)

- 3.10.1 Import/export volume & value trends (driven by primary research)

- 3.10.2 Key trade corridors & tariff impact (driven by primary research)

- 3.10.3 Major importing & exporting countries

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Swivel

- 5.3 Rigid/ Fixed

- 5.4 Ball bearing

- 5.5 Kingpin

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Metal

- 6.3 Rubber

- 6.4 Plastic

- 6.5 Polyurethane

Chapter 7 Market Estimates & Forecast, By Load Capacity, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Light-duty

- 7.3 Medium-duty

- 7.4 Heavy-duty

Chapter 8 Market Estimates & Forecast, By Mounting, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Plate

- 8.3 Stem

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Industrial

- 9.3 Commercial

- 9.4 Healthcare

- 9.5 Residential

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Automotive

- 10.3 Aerospace

- 10.4 Food Industry

- 10.5 Medical

- 10.6 Textile industry

- 10.7 Other end-users

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Direct

- 11.3 Indirect

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 Saudi Arabia

- 12.6.2 UAE

- 12.6.3 South Africa

Chapter 13 Company Profiles

- 13.1 Blickle

- 13.2 Cebora

- 13.3 COLSON GROUP

- 13.4 Er Wagner

- 13.5 Flywheel Metalwork

- 13.6 Hamilton Caster

- 13.7 Hexpol

- 13.8 Payson Casters

- 13.9 Regal Castors

- 13.10 RWM Casters

- 13.11 Takigen

- 13.12 Tellure

- 13.13 TENTE

- 13.14 TrioPines

- 13.15 ZONWE