|

市場調查報告書

商品編碼

2027619

行式印表機市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。Line Printer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

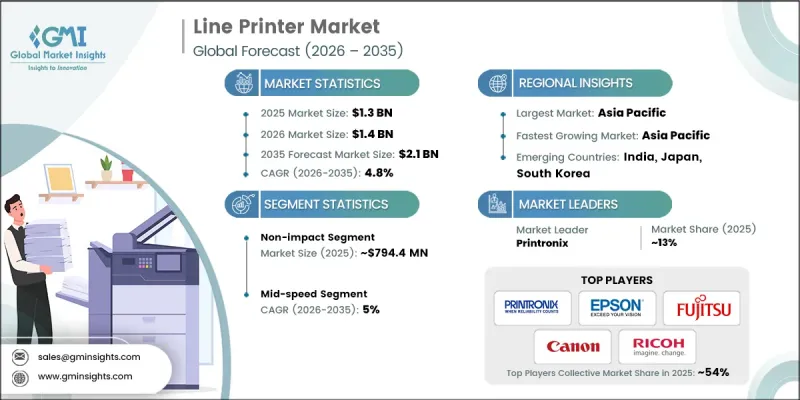

全球行式印表機市場預計到 2025 年將價值 13 億美元,預計到 2035 年將以 4.8% 的複合年成長率成長至 21 億美元。

市場成長的驅動力在於大規模資料處理環境中對高速列印解決方案日益成長的需求。處理海量交易資料的組織需要可靠的系統,以提供持續穩定的輸出。兼具耐用性和持續性能的強大列印設備對於企業系統和資料密集型環境中的大批量處理至關重要。行式印表機因其能夠以最小的停機時間處理大量工作負載而日益受到青睞,成為維持營運效率不可或缺的工具。其長使用壽命和堅固的結構進一步提升了其在嚴苛應用中的價值。企業優先考慮能夠實現無縫資料處理和報告且最大限度減少營運中斷的解決方案。隨著企業對高速列印技術在管理大批量工作負載方面的依賴性不斷增強,整體生產力不斷提高,行式印表機市場正逐漸成為企業基礎設施中穩定且不可或缺的組成部分。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 13億美元 |

| 預測金額 | 21億美元 |

| 複合年成長率 | 4.8% |

金融機構和公共部門組織對行式印表機的日益普及,為行式印表機產業帶來了進一步的成長機會。這些組織需要處理大量交易文檔,因此必須確保可靠且持續的產出。為了支援日常工作流程,不間斷列印的需求推動了對高效能系統的需求。在高容量文件處理環境中,可靠的列印基礎架構對於維持效率至關重要。

預計到2025年,非衝擊式列印市場規模將達到7.944億美元,並在2035年之前以4.6%的複合年成長率成長。與傳統的衝擊式列印相比,非衝擊式列印具有更高的效率、更穩定的輸出品質和更低的運作噪音,因此正推動著行式印表機市場的發展。非衝擊式列印技術在列印過程中無需直接物理接觸,從而確保了性能穩定,並減少了磨損和維護需求。其適用於大量列印應用的特性也持續推動此技術的廣泛應用。

預計到2025年,中速印表機市場佔有率將達到45.3%,並在2026年至2035年間以5%的複合年成長率成長。該細分市場之所以佔據主導地位,是因為其在性能、價格和運行可靠性方面實現了平衡。中速印表機能夠提供足夠的輸出能力,滿足大多數產業和企業的需求,同時又避免了高速系統帶來的複雜性和高成本。其高效性和成本效益使其成為尋求可靠性能的企業的理想選擇。

預計到2025年,中國行式印表機市場規模將達到1.26億美元,2035年之前的複合年成長率(CAGR)為5.9%。市場成長的主要驅動力是工業和商業領域對高速、大批量列印解決方案日益成長的需求。物流、零售和金融服務等行業的業務擴張也推動了對耐用高效列印系統的需求。製造商正致力於提高產品可靠性、降低維護成本並加強與企業系統的整合,以滿足不斷變化的業務需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 大規模資料處理環境對高速列印的持續需求。

- 銀行、金融服務機構和政府機構的實施情況

- 衝擊式印刷技術的耐用性和長運作

- 陷阱與挑戰

- 由於數位化文件和無紙化工作流程,需求下降

- 與最新雷射印表機和高速噴墨印表機競爭。

- 機會

- 對傳統企業系統和大型主機環境的持續需求

- 開發一種緊湊節能的行式印表機模型

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 價格分析(基於初步調查)

- 過去價格趨勢分析(基於初步調查)(2019-2024 年)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 貿易數據分析(基於付費資料庫)

- 按HS編碼分類的進出口量和進口額趨勢(基於付費資料庫)

- 主要貿易路線和關稅影響分析(基於付費資料庫)

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的運作能力(基於初步調查)

- 運轉率和擴張計劃(基於初步調查)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 衝擊式行印表機

- 鼓式印表機

- 鍊式印表機

- 帶狀印表機

- 點陣印表機

- 非擊打式行式印表機

- 熱敏行式印表機

- 靜電印表機

第6章 市場估算與預測:依列印速度分類,2022-2035年

- 慢速

- 中等的

- 高的

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 列印交易明細

- 列印報告

- 條碼和標籤列印

- 文件列印

- 其他

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 製造業和工業部門

- 零售和物流

- 銀行和金融服務

- 衛生保健

- 政府/公共部門

- 通訊/IT

- 其他

第9章 市場估價與預測:依通路分類,2022-2035年

- 直接地

- 間接

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第11章:公司簡介

- Bixolon Co., Ltd.

- Canon Inc.

- Citizen Systems Japan Co., Ltd.

- DASCOM

- Epson

- Fujitsu Limited

- Hewlett-Packard Development Company(HP)

- Jolimark Holdings Limited

- Microplex GmbH

- OKI Data Corporation

- Printronix

- Ricoh Company, Ltd.

- Star Micronics Co., Ltd.

- Toshiba Tec Corporation

- Xerox Corporation

The Global Line Printer Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 2.1 billion by 2035.

Market growth is driven by the rising need for high-speed printing solutions across large-scale data processing environments. Organizations handling extensive transactional data require dependable systems capable of delivering consistent and uninterrupted output. High-volume operations across enterprise systems and data-intensive environments demand robust printing equipment designed for durability and continuous performance. Line printers are increasingly preferred due to their ability to handle substantial workloads with minimal downtime, making them essential for maintaining operational efficiency. Their long service life and heavy-duty construction further enhance their value in demanding applications. Businesses are prioritizing solutions that enable seamless data processing and reporting while minimizing disruptions. The growing reliance on high-speed printing technologies to manage bulk workloads is strengthening overall productivity, positioning the line printer market as a stable and essential component within enterprise infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.1 Billion |

| CAGR | 4.8% |

Rising adoption across financial institutions and public sector organizations is creating additional growth opportunities for the line printer industry. These entities manage large volumes of transactional documentation that require reliable and continuous output. The need for uninterrupted printing to support daily operational workflows is reinforcing demand for high-performance systems. Reliable print infrastructure remains critical for maintaining efficiency in documentation-heavy environments.

The non-impact segment generated USD 794.4 million in 2025 and is expected to grow at a CAGR of 4.6% through 2035. This segment leads the line printer market due to its efficiency, consistent output quality, and lower operational noise compared to traditional impact systems. Non-impact technologies operate without direct physical contact during printing, which reduces wear and maintenance requirements while ensuring stable performance. Their suitability for high-volume applications continues to support widespread adoption.

The mid-speed segment accounted for 45.3% share in 2025 and is projected to grow at a CAGR of 5% from 2026 to 2035. This segment dominates due to its balanced offering of performance, affordability, and operational reliability. Mid-speed printers provide sufficient output capacity for most industrial and enterprise requirements without the complexity or cost associated with higher-speed systems. Their efficiency and cost-effectiveness make them a preferred choice for organizations seeking dependable performance.

China Line Printer Market captured USD 126 million in 2025 with an anticipated CAGR of 5.9% through 2035. Market growth is supported by increasing demand from industrial and commercial sectors that rely on high-speed, large-volume printing solutions. Expanding operations in logistics, retail, and financial services are driving the adoption of durable and efficient printing systems. Manufacturers are focusing on enhancing product reliability, reducing maintenance needs, and improving integration with enterprise systems to meet evolving business requirements.

Key companies operating in the Global Line Printer Market include Canon Inc., Epson, Fujitsu Limited, Hewlett-Packard Development Company (HP), Ricoh Company, Ltd., Xerox Corporation, Toshiba Tec Corporation, OKI Data Corporation, Printronix, Bixolon Co., Ltd., Citizen Systems Japan Co., Ltd., DASCOM, Jolimark Holdings Limited, Microplex GmbH, and Star Micronics Co., Ltd. Companies in the Line Printer Market are strengthening their market presence through continuous product innovation and performance optimization. Manufacturers are investing in advanced technologies to enhance printing speed, durability, and operational efficiency. Expanding product portfolios to address diverse industrial requirements is a key focus area. Strategic collaborations and distribution network expansion are enabling broader market reach. Companies are also prioritizing energy efficiency and reduced maintenance to improve overall value for customers. Additionally, integration with modern enterprise systems and improved connectivity features are helping businesses streamline operations, while after-sales support and service capabilities are enhancing long-term customer relationships.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Print speed

- 2.2.4 Application

- 2.2.5 End use

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Continued demand for high-speed printing in large-scale data processing environments

- 3.2.1.2 Adoption in banking, financial services, and government institutions

- 3.2.1.3 Durability and long operational life of impact printing technologies

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Declining demand due to digital documentation and paperless workflows

- 3.2.2.2 Competition from modern laser and high-speed inkjet printers

- 3.2.3 Opportunities

- 3.2.3.1 Sustained demand in legacy enterprise systems and mainframe environments

- 3.2.3.2 Development of compact and energy-efficient line printer models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research) (2019-2024)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.10 Trade data analysis (driven by paid data base)

- 3.10.1 Import/export volume & value trends by HS code (driven by paid data base)

- 3.10.2 Key trade corridors & tariff impact analysis (driven by paid data base)

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Capacity & production landscape (driven by primary research)

- 3.12.1 Installed capacity by region & key producer (driven by primary research)

- 3.12.2 Capacity utilization rates & expansion pipelines (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Impact line printers

- 5.2.1 Drum printers

- 5.2.2 Chain printers

- 5.2.3 Band printers

- 5.2.4 Dot matrix printers

- 5.3 Non-impact line printers

- 5.3.1 Thermal line printers

- 5.3.2 Electrostatic printers

Chapter 6 Market Estimates & Forecast, By Print Speed, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Low

- 6.3 Mid

- 6.4 High

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Transaction printouts

- 7.3 Report printing

- 7.4 Barcode and label printing

- 7.5 Document printing

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By End-use, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Manufacturing and industrial sector

- 8.3 Retail and logistics

- 8.4 Banking and financial services

- 8.5 Healthcare

- 8.6 Government and public sector

- 8.7 Telecommunication and IT

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Bixolon Co., Ltd.

- 11.2 Canon Inc.

- 11.3 Citizen Systems Japan Co., Ltd.

- 11.4 DASCOM

- 11.5 Epson

- 11.6 Fujitsu Limited

- 11.7 Hewlett-Packard Development Company (HP)

- 11.8 Jolimark Holdings Limited

- 11.9 Microplex GmbH

- 11.10 OKI Data Corporation

- 11.11 Printronix

- 11.12 Ricoh Company, Ltd.

- 11.13 Star Micronics Co., Ltd.

- 11.14 Toshiba Tec Corporation

- 11.15 Xerox Corporation

3D相機市場規模、佔有率和成長分析:按技術、相機類型、手持式、桌上型電腦、嵌入式、行動、商用級、類別、解析度和地區分類-2026-2033年產業預測

3D相機市場規模、佔有率和成長分析:按技術、相機類型、手持式、桌上型電腦、嵌入式、行動、商用級、類別、解析度和地區分類-2026-2033年產業預測 3D相機市場:2026-2032年全球市場預測(依產品類型、影像感測技術、部署模式、應用、終端用戶產業及通路分類)

3D相機市場:2026-2032年全球市場預測(依產品類型、影像感測技術、部署模式、應用、終端用戶產業及通路分類) 3D相機市場分析及預測(至2035年):類型、產品、技術、組件、應用、外形、設備、最終用戶、功能、安裝方式結構光雷射二極體模組市場(按雷射類型、光源、輸出功率、圖案類型、應用、分銷管道和終端用戶行業分類)—全球預測,2026-2032年英格斯相機市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、功能、安裝類型及模式分類

3D相機市場分析及預測(至2035年):類型、產品、技術、組件、應用、外形、設備、最終用戶、功能、安裝方式結構光雷射二極體模組市場(按雷射類型、光源、輸出功率、圖案類型、應用、分銷管道和終端用戶行業分類)—全球預測,2026-2032年英格斯相機市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、功能、安裝類型及模式分類 2026年全球3D相機市場報告微米級3D工業相機市場:依產品類型、技術、終端用戶產業和應用分類-2026-2032年全球預測結構光雷射市場:按組件類型、波長、輸出功率、應用和最終用戶產業分類 - 全球預測(2026-2032 年)結構光雷射模組市場(依產品類型、應用、最終用戶和通路分類)-2026-2032年全球預測雷射振鏡相機市場按產品類型、雷射功率、雷射波長、振鏡轉速、控制類型、應用和最終用戶分類-2026-2032年全球預測

2026年全球3D相機市場報告微米級3D工業相機市場:依產品類型、技術、終端用戶產業和應用分類-2026-2032年全球預測結構光雷射市場:按組件類型、波長、輸出功率、應用和最終用戶產業分類 - 全球預測(2026-2032 年)結構光雷射模組市場(依產品類型、應用、最終用戶和通路分類)-2026-2032年全球預測雷射振鏡相機市場按產品類型、雷射功率、雷射波長、振鏡轉速、控制類型、應用和最終用戶分類-2026-2032年全球預測