|

市場調查報告書

商品編碼

2027605

保險桿感測器市場機會、成長要素、產業趨勢分析及2026-2035年預測Bumper Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

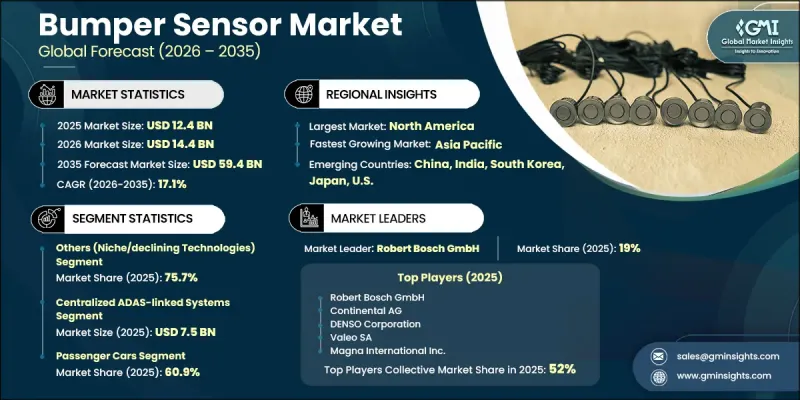

全球保險桿感測器市場預計到 2025 年價值 124 億美元,預計到 2035 年將達到 594 億美元,年複合成長率為 17.1%。

這一市場成長與主要經濟體汽車安全法規的快速收緊以及互聯無線感測系統在現代車輛中日益普及密切相關。日益嚴重的都市區擁塞和停車位短缺也推動了先進泊車輔助技術的應用,這直接支撐了對保險桿感測器的需求。同時,高階駕駛輔助系統(ADAS)的加速部署強化了基於保險桿的感測技術在防撞和即時物體偵測方面的作用。市場也正經歷著向感測器融合的結構性轉變,該技術結合了超音波、雷達和攝影機等多種輸入,以提高檢測精度並減少誤差。消費者對更安全駕駛體驗日益成長的需求,以及汽車製造商(OEM)對自動駕駛汽車平臺的重視,進一步擴大了產品的普及範圍。乘用車產量的增加、OEM和售後市場通路滲透率的提高以及電子控制系統的持續進步,都為該行業在全球汽車生態系統中實現強勁的長期成長奠定了基礎。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 124億美元 |

| 預計金額 | 594億美元 |

| 複合年成長率 | 17.1% |

到2025年,集中式ADAS(高級駕駛輔助系統)市場規模將達75億美元。這些系統整合了來自保險桿感測器、雷達單元和相機模組的輸入,建構統一的處理架構,從而實現協調一致的安全響應。它們廣泛應用於乘用車和商用車,支援碰撞規避、緊急煞車和自動停車輔助等功能。與電控系統(ECU)的整合提高了系統可靠性,並確保符合不斷發展的安全標準,進一步推動了其在現代汽車平台上的普及應用。

預計2026年至2035年間,感測器融合(架構主導整合)細分市場將以16.8%的複合年成長率成長。此細分市場的成長主要得益於整合式高階駕駛輔助系統(ADAS)生態系統的日益普及,這些系統將多種感測技術整合到單一的決策框架中。這種方法能夠提高目標偵測精度、縮短反應時間,並支援車輛的半自動駕駛功能。此外,它還有助於減少誤報訊號,提高系統整體可靠性,這促使汽車製造商在中階和高階車型領域推廣融合感測器架構的標準化應用。

預計到2025年,北美保險桿感測器市場佔有率將達到36.3%,這主要得益於嚴格的車輛安全法規以及對透過先進汽車技術減少交通事故的高度重視。美國法規結構不斷完善,加強對高階駕駛輔助系統(ADAS)的監管,從而促進了車輛安全監控系統的更廣泛應用。政府機構和產業相關人員持續投資於防撞和智慧出行解決方案的調查計畫,也推動了該地區保險桿感測器技術的應用。

保險桿感測器產業涵蓋了採埃孚股份公司 (ZF Friedrichshafen AG)、羅伯特·博世有限公司 (Robert Bosch GmbH)、恩智浦半導體 (NXP Semiconductors)、森斯塔科技 (Sensta Technologies)、法雷奧公司 (Valeo SA)、亞德諾半導體 (Analogces Devi Mobis)、安波福 (Aptiv)、麥格納國際 (Magna International)、村田製作所 (Murata Manufacturing)、日立汽車系統公司 (Hitachi Automotive Systems)、英飛凌科技 (Infineon Technologies) 和瑞達科技 (Redatec) 等公司。這些公司致力於透過整合高級駕駛輔助系統 (ADAS) 和大力投資下一代感測器融合平台來鞏固自身市場地位。每家公司都在產品系列中添加高度整合的超音波、雷達和攝影機感測解決方案,以提高偵測精度並降低系統複雜性。與汽車原始設備製造商 (OEM) 建立策略合作夥伴關係是各公司優先考慮的事項,以確保將早期設計整合到未來的汽車平臺中。此外,各公司也正在投資軟體主導的感測智慧技術,以實現即時數據處理和預測性安全功能。透過半導體技術的進步和小型化感測器設計來最佳化成本也是重點關注領域,這有助於製造商高效地擴大生產規模。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 加強全球NCAP安全標準要求

- ADAS在中檔車輛的廣泛應用

- 都市區停車位日益短缺,推動了感測器的引入。

- 超音波感測器作為OEM設備的標準化

- 擴展自動駕駛功能管道

- 產業潛在風險與挑戰

- 極端天氣條件下感測器性能下降

- 與多感測器ADAS架構整合的複雜性

- 市場機遇

- 向軟體定義車輛感測器生態系統過渡

- 發展中地區對售後改裝的需求不斷成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要公司的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與發展(R&D)

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興/新創競爭對手的發展趨勢

第5章 市場估計與預測:依技術分類,2022-2035年

- 超音波感測器

- 雷達感測器(短程)

- 感測器融合(架構主導的整合)

- 其他(小眾/衰退技術)

第6章 市場估算與預測:依系統結構,2022-2035年

- 獨立式感測器

- 保險桿整合式感測器系統

- 集中式ADAS整合系統

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 停車輔助系統(PAS)

- 盲點偵測(BSD)

- 後側路口交通警報(RCTA)

- 低速碰撞避免

- 其他

第8章 市場估價與預測:依車輛類型分類,2022-2035年

- 搭乘用車

- 商用車輛

第9章 市場估價與預測:依銷售管道分類,2022-2035年

- OEM(原始設備製造商)

- 售後市場

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 全球主要公司

- Robert Bosch GmbH

- Continental AG

- DENSO Corporation

- Valeo SA

- Magna International Inc.

- 按地區分類的主要公司

- 北美洲

- Aptiv PLC

- LeddarTech Inc.

- Sensata Technologies

- 亞太地區

- Hyundai Mobis

- Hitachi Automotive Systems

- Murata Manufacturing Co., Ltd.

- NXP Semiconductors

- 歐洲

- ZF Friedrichshafen AG

- Infineon Technologies AG

- 北美洲

- 特殊玩家/干擾者

- Analog Devices, Inc.

The Global Bumper Sensor Market was valued at USD 12.4 billion in 2025, and it is estimated to grow at a CAGR of 17.1% to reach USD 59.4 billion by 2035.

The market growth is linked to the rapid strengthening of vehicle safety regulations across major economies, alongside the rising integration of connected and wireless sensing systems in modern vehicles. Increasing urban congestion and limited parking space availability are also pushing the adoption of advanced parking assistance technologies, which directly support bumper sensor demand. At the same time, the accelerated deployment of Advanced Driver Assistance Systems (ADAS) is reinforcing the role of bumper-based sensing in collision prevention and real-time object detection. The market is also witnessing a structural shift toward sensor fusion, where ultrasonic, radar, and camera-based inputs are combined to improve detection accuracy and reduce errors in judgment. Growing consumer preference for safer driving experiences, combined with OEM focus on automation-ready vehicle platforms, is further strengthening product adoption. Expanding passenger vehicle production, increasing penetration in both OEM and aftermarket channels, and continuous advancements in electronic control systems are collectively shaping a strong long-term growth trajectory for the industry across global automotive ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.4 Billion |

| Forecast Value | $59.4 Billion |

| CAGR | 17.1% |

The centralized ADAS-linked systems segment reached USD 7.5 billion in 2025. These systems consolidate inputs from bumper sensors, radar units, and camera modules into a unified processing architecture that enables coordinated safety responses. They are widely implemented across passenger and commercial vehicles to support collision avoidance, emergency braking functions, and automated parking assistance. Their integration into electronic control units improves system reliability and ensures compliance with evolving safety standards, which continues to drive their widespread adoption across modern automotive platforms.

The sensor fusion (architecture-driven integration) segment is projected to grow at a CAGR of 16.8% during 2026-2035. Growth in this segment is driven by increasing deployment of integrated ADAS ecosystems that combine multiple sensing technologies into a single decision-making framework. This approach enhances object detection accuracy, strengthens response time, and supports semi-automated driving capabilities in vehicles. It also helps reduce false detection signals and improves overall system reliability, which is encouraging automotive manufacturers to standardize fused sensor architectures across both mid-range and premium vehicle categories.

North America Bumper Sensor Market accounted for 36.3% share in 2025, supported by strict vehicle safety enforcement and a strong emphasis on reducing road accidents through advanced automotive technologies. Regulatory frameworks in the United States continue to evolve toward enhanced oversight of driver assistance technologies, encouraging wider deployment of safety monitoring systems in vehicles. Continuous investment from government bodies and industry participants in research programs focused on crash prevention and intelligent mobility solutions is also strengthening the regional adoption of bumper sensor technologies.

The Bumper Sensor Industry includes several key players such as ZF Friedrichshafen AG, Robert Bosch GmbH, NXP Semiconductors, Sensata Technologies, Valeo SA, Analog Devices, Inc., Continental AG, DENSO Corporation, Hyundai Mobis, Aptiv PLC, Magna International Inc., Murata Manufacturing Co., Ltd., Hitachi Automotive Systems, Infineon Technologies AG, and LeddarTech Inc. Companies operating in the Bumper Sensor Market are focusing on strengthening their position through aggressive investment in ADAS integration and next-generation sensor fusion platforms. They are expanding product portfolios to include highly integrated ultrasonic, radar, and camera-based sensing solutions that improve detection accuracy and reduce system complexity. Strategic partnerships with automotive OEMs are being prioritized to secure early design integration in upcoming vehicle platforms. Firms are also investing in software-driven sensing intelligence, enabling real-time data processing and predictive safety functions. Cost optimization through semiconductor advancements and miniaturized sensor designs is another key focus area, helping manufacturers scale production efficiently.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Technology trends

- 2.2.2 System architecture trends

- 2.2.3 Application trends

- 2.2.4 Vehicle type trends

- 2.2.5 Sales channel trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global NCAP safety compliance requirements

- 3.2.1.2 Increasing ADAS penetration in mid-range vehicles

- 3.2.1.3 Growing urban parking constraints boosting sensor adoption

- 3.2.1.4 OEM integration of ultrasonic sensors as standard features

- 3.2.1.5 Expansion of autonomous driving feature pipelines

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Sensor performance degradation in extreme weather conditions

- 3.2.2.2 Integration complexity with multi-sensor ADAS architectures

- 3.2.3 Market opportunities

- 3.2.3.1 Transition toward software-defined vehicle sensor ecosystems

- 3.2.3.2 Increasing aftermarket retrofitting demand in developing regions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Ultrasonic sensors

- 5.3 Radar sensors (short-range)

- 5.4 Sensor fusion (architecture-driven integration)

- 5.5 Others (niche/declining technologies)

Chapter 6 Market Estimates and Forecast, By System Architecture, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Standalone sensors

- 6.3 Integrated bumper sensor systems

- 6.4 Centralized ADAS-linked systems

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Parking assistance systems (PAS)

- 7.3 Blind spot detection (BSD)

- 7.4 Rear cross traffic alert (RCTA)

- 7.5 Low-speed collision avoidance

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.3 Commercial vehicles

Chapter 9 Market Estimates and Forecast, By Sales Channel, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 OEM (original equipment manufacturer)

- 9.3 Aftermarket

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Robert Bosch GmbH

- 11.1.2 Continental AG

- 11.1.3 DENSO Corporation

- 11.1.4 Valeo SA

- 11.1.5 Magna International Inc.

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Aptiv PLC

- 11.2.1.2 LeddarTech Inc.

- 11.2.1.3 Sensata Technologies

- 11.2.2 Asia Pacific

- 11.2.2.1 Hyundai Mobis

- 11.2.2.2 Hitachi Automotive Systems

- 11.2.2.3 Murata Manufacturing Co., Ltd.

- 11.2.2.4 NXP Semiconductors

- 11.2.3 Europe

- 11.2.3.1 ZF Friedrichshafen AG

- 11.2.3.2 Infineon Technologies AG

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 Analog Devices, Inc.

汽車保險桿市場:按材料、安裝方式、車輛類型、銷售管道和應用分類-2026-2032年全球市場預測汽車原廠配件保險桿罩市場:依技術、表面處理類型、安裝位置、材質、車輛類型和銷售管道分類-2026-2032年全球市場預測

汽車保險桿市場:按材料、安裝方式、車輛類型、銷售管道和應用分類-2026-2032年全球市場預測汽車原廠配件保險桿罩市場:依技術、表面處理類型、安裝位置、材質、車輛類型和銷售管道分類-2026-2032年全球市場預測 2026年全球智慧保險桿市場報告

2026年全球智慧保險桿市場報告 全球保險桿感測器市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球汽車原廠保險桿罩市場規模、佔有率、趨勢和成長分析報告:2026-2034年

全球保險桿感測器市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球汽車原廠保險桿罩市場規模、佔有率、趨勢和成長分析報告:2026-2034年 保險桿橫樑市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、銷售管道、車輛類型、地區和競爭格局分類,2021-2031年汽車保險桿市場 - 全球產業規模、佔有率、趨勢、機會、預測:按材料類型、位置類型、銷售管道類型、地區和競爭格局分類,2021-2031年智慧B柱市場按技術類型、車輛類型、材質和應用分類-2026-2032年全球預測

保險桿橫樑市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、銷售管道、車輛類型、地區和競爭格局分類,2021-2031年汽車保險桿市場 - 全球產業規模、佔有率、趨勢、機會、預測:按材料類型、位置類型、銷售管道類型、地區和競爭格局分類,2021-2031年智慧B柱市場按技術類型、車輛類型、材質和應用分類-2026-2032年全球預測 汽車保險桿市場規模、佔有率和成長分析(按類型、材質、安裝位置、車輛類型、銷售量和地區分類)-2026-2033年產業預測

汽車保險桿市場規模、佔有率和成長分析(按類型、材質、安裝位置、車輛類型、銷售量和地區分類)-2026-2033年產業預測 全球保險桿感測器市場

全球保險桿感測器市場