|

市場調查報告書

商品編碼

2027604

2026 年至 2035 年奢侈家具市場的商業機會、成長要素、產業趨勢和預測。Luxury Furniture Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

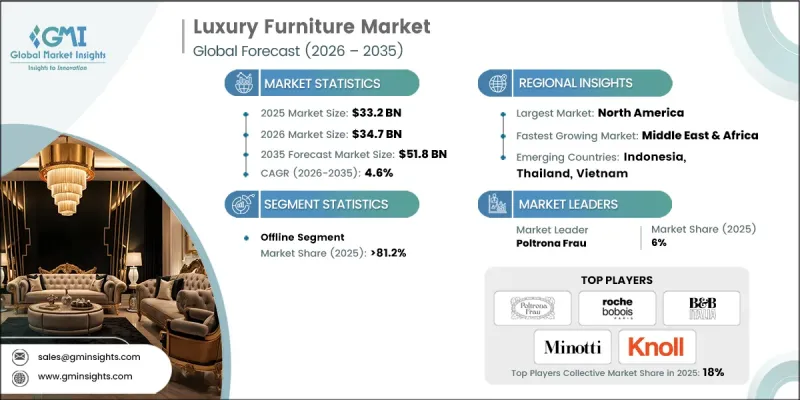

預計到 2025 年,全球奢侈家具市場價值將達到 332 億美元,並有望以 4.6% 的複合年成長率成長,到 2035 年達到 518 億美元。

市場動能深受超級富豪階級消費行為的影響,他們將家具購買視為提升生活品質和創造長期價值的融合。奢侈家具不再只專注於功能性;買家在選購時越來越重視設計傳統、工藝和稀缺性。此外,人們對多樣化所有權形式的需求,反映了不斷變化的生活方式偏好,也進一步塑造了市場格局。在發展中地區,富裕階層的崛起推動了對象徵個人成功和優雅品味的優質室內裝潢的需求。消費者越來越傾向於選擇耐用、高品質的產品,而非大量生產的替代品,這與「理性消費」理念的廣泛轉變不謀而合。對客製化和永續性的日益關注也在重新定義產品開發策略,因為買家正在尋求獨特且環保的設計。可支配收入的成長,以及全球設計標準的普及,正在推動奢侈家具的蓬勃發展,為成熟經濟體和新興經濟體市場的穩步擴張奠定了基礎。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 332億美元 |

| 預測金額 | 518億美元 |

| 複合年成長率 | 4.6% |

到2025年,以舒適性為核心的家具細分市場將佔據最大的市場佔有率。該細分市場將功能性與強烈的視覺吸引力相結合,在高階室內設計中扮演核心角色。它涵蓋了眾多旨在提升各種生活環境舒適度和美感的各類產品。市場需求主要源自於對精湛工藝、優質材料和精緻設計的追求。隨著對人體工學性能、美學細節和客製化需求的日益重視,該細分市場不斷發展,進一步鞏固了其在整體高階家具市場中的重要地位。

預計到2025年,線下銷售管道仍將維持其主導地位,佔據81.2%的市場。實體零售在高階家具銷售中繼續發揮至關重要的作用,因為消費者在購買高價值產品前更傾向於親自查看產品的品質、材質和設計。高階品牌經營的展示室作為體驗空間,展示全系列產品並提供個人化的客戶服務。這些展廳也發揮著品牌建立平台的作用,支持行銷活動並加強客戶參與。位於高檔商業區的策略位置進一步提升了品牌知名度和便利性,鞏固了線下管道的主導地位。

預計到2035年,亞太地區的豪華家具市場將以5.1%的複合年成長率成長。全部區域的成長主要得益於不斷擴大的富裕人口、快速的城市化以及對豪華住宅和酒店項目投資的增加。消費者越來越關注全球趨勢,這進一步推動了對高品質家具的需求。同時,本地製造能力的提升也使區域品牌能夠在豪華家具領域中展開有效競爭。這些因素共同鞏固了亞太地區作為全球豪華家具市場關鍵樞紐的地位,無論是在消費方面還是創新方面。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 提升國際奢侈品牌的品牌知名度與消費者渴望

- 電子商務滲透率和數位購物的便利性

- 全球豪華飯店、餐廳和商業設施的擴張

- 產業潛在風險與挑戰

- 供應鏈中斷和材料短缺

- 外匯波動影響國際銷售

- 機會

- 豪華家具租賃和訂閱模式

- 為成熟品牌打造優質化與故事化

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 奢侈品市場的需求價格彈性

- 外匯波動對進口價格的影響

- 法律規範

- 波特的分析

- PESTEL 分析

- 貿易資料分析(HS編碼:9401 - 座位)(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 主要出口國及進口國

- 區域貿易流量分析

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 個性化設計和客製化引擎

- 人工智慧驅動的室內設計諮詢

- 需求預測分析與庫存管理

- 虛擬展示室與身臨其境型購物體驗

- 消費者購買行為分析

- 購買模式

- 偏好分析

- 消費行為的區域差異

- 電子商務對購買決策的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 桌子

- 椅子

- 沙發休息室

- 廚房

- 照明

- 室內裝飾品

- 床

- 其他

第6章 市場估計與預測:依材料分類,2022-2035年

- 木頭

- 金屬

- 室內裝潢材料

- 玻璃水晶

- 複合材料及其他

第7章 市場估計與預測:依價格分類,2022-2035年

- 超豪華(每件超過 10,000 美元)

- 頂級奢侈品(每件5000美元至10000美元)

- 價格適中的奢侈品(每件2000美元至5000美元)

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 住宅

- 商業的

- 飯店和度假村

- 餐廳和咖啡館

- 公司總部

- 其他

第9章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 企業網站

- 離線

- 大型零售商店及家居建材商店

- 專賣店

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第11章:公司簡介

- Arhaus

- B&B Italia

- Baker Furniture

- Cassina

- Ethan Allen

- Fendi Casa

- Flexform

- Herman Miller

- King Living

- Knoll

- KUKA

- Ligne Roset

- Man Wah Holdings Limited

- Markor International Home Furnishings

- Minotti

- Natuzzi

- Poltrona Frau

- Restoration Hardware(RH)

- Roche Bobois

- Rolf Benz

The Global Luxury Furniture Market was valued at USD 33.2 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 51.8 billion by 2035.

Market momentum is strongly influenced by the spending behavior of ultra-high-net-worth individuals, who view furniture purchases as a blend of lifestyle enhancement and long-term value creation. High-end furnishings are no longer limited to functionality, as buyers increasingly consider design heritage, craftsmanship, and exclusivity when making purchasing decisions. The market is further shaped by demand across multiple ownership environments, reflecting evolving lifestyle preferences. In developing regions, a growing affluent population is fueling demand for premium interiors that symbolize personal success and refined taste. Consumers are increasingly prioritizing durable, high-quality products over mass-produced alternatives, aligning with a broader shift toward mindful consumption. The growing emphasis on customization and sustainability is also redefining product development strategies, as buyers seek unique, environmentally responsible designs. Rising discretionary income levels, combined with increasing exposure to global design standards, are strengthening the adoption of luxury furniture, positioning the market for steady expansion across both established and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $33.2 Billion |

| Forecast Value | $51.8 Billion |

| CAGR | 4.6% |

The seating furniture segment held the largest share in 2025. This segment plays a central role in luxury interiors by combining functionality with strong visual appeal. It includes a wide spectrum of products designed to enhance both comfort and aesthetics across different living environments. Demand is driven by the need for refined craftsmanship, premium materials, and design sophistication. The category continues to evolve with a focus on ergonomic performance, aesthetic detailing, and customization, reinforcing its importance within the broader luxury furniture landscape.

The offline distribution channel accounted for 81.2% share in 2025, maintaining its dominant position. Physical retail continues to play a critical role in luxury furniture sales, as customers prefer to evaluate product quality, materials, and design in person before making high-value purchases. Showrooms operated by premium brands serve as experiential spaces that showcase complete collections and deliver personalized customer service. These locations also function as brand-building platforms, supporting marketing initiatives and strengthening customer engagement. Strategic placement in high-end retail districts enhances visibility and accessibility, further supporting offline channel dominance.

Asia Pacific Luxury Furniture Market is projected to grow at a CAGR of 5.1% through 2035. Growth across the region is driven by expanding affluent populations, rapid urban development, and increasing investment in premium residential and hospitality projects. Consumers are becoming more exposed to global design trends, which is elevating demand for high-quality furnishings. At the same time, improvements in local manufacturing capabilities are enabling regional brands to compete effectively in the luxury segment. These combined factors are positioning Asia Pacific as a key hub for both consumption and innovation in the global luxury furniture market.

Key companies operating in the Global Luxury Furniture Market include Arhaus, B&B Italia, Baker Furniture, Cassina, Ethan Allen, Fendi Casa, Flexform, Herman Miller, King Living, Knoll, KUKA, Ligne Roset, Man Wah Holdings Limited, Markor International Home Furnishings, Minotti, Natuzzi, Poltrona Frau, Restoration Hardware (RH), Roche Bobois, and Rolf Benz. Companies in the Luxury Furniture Market are strengthening their competitive position by investing in design innovation, premium materials, and customization capabilities. Many players focus on enhancing brand identity through exclusive collections, collaborations, and limited-edition offerings that appeal to affluent consumers. Expansion of flagship showrooms in prime locations supports immersive brand experiences and customer engagement. Businesses are also prioritizing sustainable sourcing and environmentally responsible manufacturing processes to align with evolving consumer expectations. Digital transformation, including online visualization tools and personalized design services, is improving customer interaction. Additionally, strategic global expansion, partnerships, and supply chain optimization are enabling companies to scale operations while maintaining product quality and brand exclusivity.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Material

- 2.2.4 Price range

- 2.2.5 Application

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing brand awareness & aspiration for international luxury brands

- 3.2.1.2 E-commerce penetration & digital shopping convenience

- 3.2.1.3 Expansion of luxury hotels, restaurants & commercial spaces globally

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Supply chain disruptions & material shortages

- 3.2.2.2 Currency volatility impacting international sales

- 3.2.3 Opportunities

- 3.2.3.1 Luxury furniture rental & subscription models

- 3.2.3.2 Heritage brand premiumization & storytelling

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Historical price trend analysis

- 3.6.2 Price elasticity of demand in luxury segment

- 3.6.3 Currency fluctuation impact on import pricing

- 3.7 Regulatory framework

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Trade data analysis (HS Code: 9401-seats) (driven by paid data base)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.10.3 Major exporting & importing countries

- 3.10.4 Trade flow analysis by region

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.3 Personalized design & customization engines

- 3.11.4 AI-powered interior design consultation

- 3.11.5 Predictive demand analytics & inventory management

- 3.11.6 Virtual showrooms & immersive shopping experiences

- 3.12 Consumer buying behavior analysis

- 3.12.1 Purchasing patterns

- 3.12.2 Preference analysis

- 3.12.3 Regional variations in consumer behavior

- 3.12.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Tables

- 5.3 Chairs

- 5.4 Sofas & lounges

- 5.5 Kitchen

- 5.6 Lighting

- 5.7 Interior accessories

- 5.8 Beds

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Wood

- 6.3 Metal

- 6.4 Upholstery

- 6.5 Glass & crystal

- 6.6 Composite & others

Chapter 7 Market Estimates and Forecast, By Price, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Ultra-luxury (>$10,000 per piece)

- 7.3 Premium luxury ($5,000-$10,000 per piece)

- 7.4 Accessible luxury ($2,000-$5,000 per piece)

Chapter 8 Market Estimates and Forecast, By End-Use, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Hotels & resorts

- 8.3.2 Restaurants & cafes

- 8.3.3 Corporate offices

- 8.3.4 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce

- 9.2.2 Company websites

- 9.3 Offline

- 9.3.1 Mega retail stores & home improvement centers

- 9.3.2 Specialty stores

- 9.3.3 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Arhaus

- 11.2 B&B Italia

- 11.3 Baker Furniture

- 11.4 Cassina

- 11.5 Ethan Allen

- 11.6 Fendi Casa

- 11.7 Flexform

- 11.8 Herman Miller

- 11.9 King Living

- 11.10 Knoll

- 11.11 KUKA

- 11.12 Ligne Roset

- 11.13 Man Wah Holdings Limited

- 11.14 Markor International Home Furnishings

- 11.15 Minotti

- 11.16 Natuzzi

- 11.17 Poltrona Frau

- 11.18 Restoration Hardware (RH)

- 11.19 Roche Bobois

- 11.20 Rolf Benz

豪華家具市場:2026-2032年全球市場預測(依產品類型、材料類型、設計風格、最終用戶、通路和使用環境分類)

豪華家具市場:2026-2032年全球市場預測(依產品類型、材料類型、設計風格、最終用戶、通路和使用環境分類) 豪華家具市場:依產品類型、材料、最終用途產業、通路及地區分類飯店家具市場:依產品類型、材料、應用、最終用戶、銷售管道和地區分類。

豪華家具市場:依產品類型、材料、最終用途產業、通路及地區分類飯店家具市場:依產品類型、材料、應用、最終用戶、銷售管道和地區分類。 2026-2034年全球豪華家具市場規模、佔有率、趨勢及成長分析報告商業豪華概念家具市場:依產品類型、材料、應用和分銷管道分類-2026-2032年全球預測全球豪華家具市場規模、佔有率、成長率、按類型和應用分類的全球產業分析、區域趨勢以及 2026-2034 年預測。

2026-2034年全球豪華家具市場規模、佔有率、趨勢及成長分析報告商業豪華概念家具市場:依產品類型、材料、應用和分銷管道分類-2026-2032年全球預測全球豪華家具市場規模、佔有率、成長率、按類型和應用分類的全球產業分析、區域趨勢以及 2026-2034 年預測。 2026-2034年豪華家具市場規模、佔有率、趨勢及預測(依材料、應用、通路、設計及地區分類)

2026-2034年豪華家具市場規模、佔有率、趨勢及預測(依材料、應用、通路、設計及地區分類) 全球豪華室內家具市場-產業規模、佔有率、趨勢、機會與預測:按類型、應用、通路、地區和競爭格局分類,2021-2031年商業豪華家具市場-全球產業規模、佔有率、趨勢、機會和預測:按材料、最終用戶、銷售管道、地區和競爭格局分類,2021-2031年水療豪華家具市場-全球產業規模、佔有率、趨勢、機會與預測:按產品類型、通路、地區和競爭格局分類,2021-2031年

全球豪華室內家具市場-產業規模、佔有率、趨勢、機會與預測:按類型、應用、通路、地區和競爭格局分類,2021-2031年商業豪華家具市場-全球產業規模、佔有率、趨勢、機會和預測:按材料、最終用戶、銷售管道、地區和競爭格局分類,2021-2031年水療豪華家具市場-全球產業規模、佔有率、趨勢、機會與預測:按產品類型、通路、地區和競爭格局分類,2021-2031年