|

市場調查報告書

商品編碼

2027602

全像顯示市場機會、成長要素、產業趨勢分析及2026-2035年預測Holographic Display Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球全像顯示市場預計到 2025 年將達到 43 億美元,預計到 2035 年將達到 408 億美元,年複合成長率為 25.5%。

市場成長的驅動力來自娛樂、醫療保健、汽車、教育和其他互動應用領域對先進3D視覺化技術日益成長的需求。沉浸式數位體驗的興起正在加速全像顯示解決方案的普及。身臨其境型成像技術的持續進步,透過提升視覺清晰度、深度感知和即時互動能力,進一步推動了市場擴張。人們對互動式內容傳送的日益偏好,促使各行業將全像系統整合到商用和消費平台中。同時,對包括投影系統和互動視覺化平台在內的下一代顯示技術的投資不斷增加,也拓展了全像顯示技術在各個領域的應用範圍。人工智慧、全像渲染和即時內容自適應技術的融合,也增強了使用者參與度和個人化體驗。隨著各產業越來越重視體驗式技術,全像顯示器正成為變革數位互動和視覺化生態系統的關鍵要素。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 43億美元 |

| 預計金額 | 408億美元 |

| 複合年成長率 | 25.5% |

受市場對身臨其境型視覺化技術的強勁需求推動,預計2035年,3D市場規模將達到212億美元。零售、娛樂和醫療保健等產業正日益採用3D全像解決方案,以提供互動性強、引人入勝的使用者體驗。這些顯示技術使用戶能夠從多個觀點查看、操作數位內容並互動,從而顯著增強感知和沈浸感。人們對逼真沉浸式數位環境的日益偏好,進一步加速了3D全像技術在各種終端應用中的普及。

預計到2025年,家用電子電器領域將佔據22.2%的市場。該領域的成長主要得益於先進顯示技術與日常電子設備的日益整合。製造商正將全像顯示功能應用於各種產品,以增強視覺互動和用戶參與。隨著技術創新不斷推進,以及對更具沉浸感和直覺的使用者介面需求的推動,全像顯示技術在家用電子電器中的應用預計將進一步擴大。

預計到2025年,北美全像顯示器市佔率將達到36.3%,主要得益於醫療和汽車產業的強勁應用。該地區在醫療影像應用和車載顯示系統中對先進視覺化技術的需求日益成長。對更高診斷精度和更佳駕駛體驗的需求不斷增加,推動了全像解決方案的整合。持續的技術進步和對研發的大力投入,進一步鞏固了該地區在全球市場的主導地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 對3D全像顯示器的需求日益成長

- 擴增實境(AR)和虛擬實境(VR)技術的日益普及

- 醫學影像診斷領域的應用擴展

- 全像顯示技術在遊戲和娛樂領域日益普及。

- 全像顯示器在數位電子看板和零售領域的應用日益廣泛。

- 產業潛在風險與挑戰

- 高昂的製造成本和實施成本

- 內容和軟體相容性限制

- 市場機遇

- 在活動、娛樂和現場表演中的應用日益廣泛

- 在智慧城市和公共基礎設施的實施

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要公司的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與發展(R&D)

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興/新創競爭對手的發展趨勢

第5章 市場估計與預測:依技術分類,2022-2035年

- 電全像

- 觸控螢幕

- 雷射

- 氣體雷射

- 基於固體雷射

- 二極體雷射系統

- 活塞

第6章 市場估計與預測:依構面分類,2022-2035年

- 2D全像顯示器

- 3D全像顯示器

- 4D全像顯示器

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 汽車抬頭顯示器

- 搭乘用車

- 輕型商用車

- 大型商用車輛

- 醫學影像診斷

- 手術影像引導

- 神經外科

- 整形外科手術

- 微創手術

- 診斷影像

- 放射科/CT

- 病理學和顯微鏡檢查

- 醫學教育和培訓

- 解剖學可視化

- 外科手術訓練模擬器

- 其他

- 手術影像引導

- 家用電子電器

- 智慧電視

- 筆記型電腦和平板電腦

- 智慧型手機和行動裝置

- 數位相機和影像設備

- 其他

- 零售數位電子看板

- 店內廣告及產品展示

- 戶外數位電子看板

- 互動式零售體驗

- 其他

- 航太/國防

- 軍用抬頭顯示器和駕駛座顯示器

- 訓練和模擬系統

- 飛行模擬器

- 戰術訓練系統

- 指揮控制中心

- 情境察覺顯示

- 任務規劃與簡報

- 其他

- AR/VR

- AR頭戴式/眼鏡

- VR遊戲和娛樂

- 企業級AR應用

- 其他

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- 全球主要公司

- Qualcomm Inc.

- ViewSonic Corporation

- Provision Holding Inc.

- MDH Hologram Ltd.

- Realview Imaging Ltd.

- RealFiction(Realfiction Holding AB)

- EON Reality Inc.

- 按地區分類的主要公司

- Konica Minolta, Inc.

- AV Concepts Inc.

- Zebra Imaging

- Looking Glass Factory Inc.

- SeeReal Technologies SA

- Leia Inc.

- 特殊玩家/干擾者

- HOLOCO GmbH

- Holoconnects

- HoloTech Switzerland AG

- HYPERVSN

- zSpace, Inc.

- Ovizio Imaging Systems NV/SA

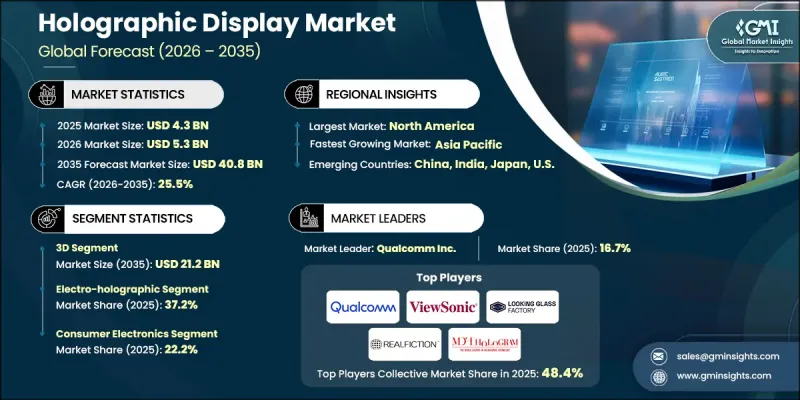

The Global Holographic Display Market was valued at USD 4.3 billion in 2025 and is estimated to grow at a CAGR of 25.5% to reach USD 40.8 billion by 2035.

Market growth is driven by the rising demand for advanced 3D visualization technologies across entertainment, healthcare, automotive, education, and other interactive application areas. The increasing shift toward highly immersive digital experiences is accelerating the adoption of holographic display solutions. Continuous advancements in immersive imaging technologies are further supporting market expansion by improving visual clarity, depth perception, and real-time interaction capabilities. The growing preference for engaging and interactive content delivery is encouraging industries to integrate holographic systems into their operational and consumer-facing platforms. At the same time, rising investments in next-generation display technologies, including projection systems and interactive visualization platforms, are broadening the scope of applications across multiple sectors. The convergence of artificial intelligence with holographic rendering and real-time content adaptation is also enhancing user engagement and personalization. As industries increasingly prioritize experiential technologies, holographic displays are emerging as a key component in transforming digital interaction and visualization ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.3 Billion |

| Forecast Value | $40.8 Billion |

| CAGR | 25.5% |

The 3D segment is projected to reach USD 21.2 billion by 2035, reflecting strong demand for immersive visualization technologies. Industries such as retail, entertainment, and healthcare are increasingly adopting 3D holographic solutions to deliver interactive and engaging user experiences. These displays enable users to view, manipulate, and interact with digital content from multiple angles, significantly enhancing perception and engagement. The rising preference for realistic and immersive digital environments is further accelerating the adoption of 3D holographic technologies across various end-use applications.

The consumer electronics segment accounted for 22.2% share in 2025. Growth in this segment is being driven by the increasing integration of advanced display technologies into everyday electronic devices. Manufacturers are incorporating holographic capabilities into a range of products to enhance visual interaction and user engagement. As technological innovation continues to advance, the adoption of holographic displays in consumer electronics is expected to expand further, driven by demand for more immersive and intuitive user interfaces.

North America Holographic Display Market held a 36.3% share in 2025, supported by strong adoption across healthcare and automotive sectors. The region is witnessing increased utilization of advanced visualization technologies in medical imaging applications and in-vehicle display systems. Growing demand for enhanced diagnostic accuracy and improved driving experiences is contributing to the integration of holographic solutions. Continuous technological advancements and strong investment in research and development are further reinforcing the region's leadership in the global market.

Key companies operating in the Global Holographic Display Market include Qualcomm Inc., ViewSonic Corporation, Provision Holding Inc., MDH Hologram Ltd., Realview Imaging Ltd., RealFiction (Realfiction Holding AB), EON Reality Inc., and Holoxica Ltd. Companies in the Holographic Display Market are strengthening their market position through continuous innovation, strategic collaborations, and expansion into emerging application areas. They are investing heavily in research and development to improve display resolution, depth accuracy, and real-time rendering capabilities. Partnerships with technology providers and end-use industries are helping accelerate commercialization and broaden application scope. Many players are focusing on integrating artificial intelligence and augmented reality features to enhance interactivity and user experience. Additionally, companies are expanding their production capabilities and global distribution networks to meet rising demand. Emphasis on cost optimization, product differentiation, and customized solutions is further enabling firms to strengthen competitiveness and capture new growth opportunities across diverse industry verticals.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Technology trends

- 2.2.2 Dimension trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for 3D holographic displays

- 3.2.1.2 Increasing adoption in augmented reality (AR) and virtual reality (VR)

- 3.2.1.3 Growing adoption in healthcare for medical imaging

- 3.2.1.4 Growing popularity of holographic displays in gaming and entertainment

- 3.2.1.5 Rising adoption of holographic displays in digital signage and retail

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and implementation costs

- 3.2.2.2 Limited content and software compatibility

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing use in events, entertainment, and live performances

- 3.2.3.2 Deployment in smart cities and public infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Electro-holographic

- 5.3 Touchable

- 5.4 Laser

- 5.4.1 Gas laser-based

- 5.4.2 Solid-state laser-based

- 5.4.3 Diode laser-based

- 5.5 Piston

Chapter 6 Market Estimates and Forecast, By Dimension, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 2D holographic displays

- 6.3 3D holographic displays

- 6.4 4D holographic displays

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Automotive head-up displays

- 7.2.1 Passenger vehicles

- 7.2.2 Light commercial vehicles

- 7.2.3 Heavy commercial vehicles

- 7.3 Medical imaging

- 7.3.1 Surgical imaging & guidance

- 7.3.1.1 Neurosurgery

- 7.3.1.2 Orthopedic surgery

- 7.3.1.3 Minimally invasive surgery

- 7.3.2 Diagnostic imaging

- 7.3.2.1 Radiology & CT

- 7.3.2.2 Pathology & microscopy

- 7.3.3 Medical education & training

- 7.3.3.1 Anatomy visualization

- 7.3.3.2 Surgical training simulators

- 7.3.3.3 Others

- 7.3.1 Surgical imaging & guidance

- 7.4 Consumer electronics

- 7.4.1 Smart TVs

- 7.4.2 Laptops & tablets

- 7.4.3 Smartphones & mobile devices

- 7.4.4 Digital cameras & imaging devices

- 7.4.5 Others

- 7.5 Retail & digital signage

- 7.5.1 In-store advertising & product display

- 7.5.2 Outdoor digital signage

- 7.5.3 Interactive retail experiences

- 7.5.4 Others

- 7.6 Aerospace and defense

- 7.6.1 Military HUDs & cockpit displays

- 7.6.2 Training & simulation systems

- 7.6.2.1 Flight simulators

- 7.6.2.2 Tactical training systems

- 7.6.3 Command & control centers

- 7.6.3.1 Situational awareness displays

- 7.6.3.2 Mission planning & briefing

- 7.6.4 Others

- 7.7 AR/VR

- 7.7.1 AR headsets & glasses

- 7.7.2 VR gaming & entertainment

- 7.7.3 Enterprise AR applications

- 7.7.4 Others

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of MEA

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Qualcomm Inc.

- 9.1.2 ViewSonic Corporation

- 9.1.3 Provision Holding Inc.

- 9.1.4 MDH Hologram Ltd.

- 9.1.5 Realview Imaging Ltd.

- 9.1.6 RealFiction (Realfiction Holding AB)

- 9.1.7 EON Reality Inc.

- 9.2 Regional key players

- 9.2.1 Konica Minolta, Inc.

- 9.2.2 AV Concepts Inc.

- 9.2.3 Zebra Imaging

- 9.2.4 Looking Glass Factory Inc.

- 9.2.5 SeeReal Technologies S.A.

- 9.2.6 Leia Inc.

- 9.3 Niche Players/Disruptors

- 9.3.1 HOLOCO GmbH

- 9.3.2 Holoconnects

- 9.3.3 HoloTech Switzerland AG

- 9.3.4 HYPERVSN

- 9.3.5 zSpace, Inc.

- 9.3.6 Ovizio Imaging Systems NV/SA

全像顯示器市場:按顯示類型、影像尺寸、技術和應用分類的全球市場預測 – 2026-2032 年

全像顯示器市場:按顯示類型、影像尺寸、技術和應用分類的全球市場預測 – 2026-2032 年 2026年全球觸控全像顯示器市場報告2026年全球3D全像市場報告汽車全像顯示器市場:按組件、尺寸、解析度類型、技術類型、顯示器尺寸、應用、車輛類型、銷售管道類型分類,全球預測,2026-2032年

2026年全球觸控全像顯示器市場報告2026年全球3D全像市場報告汽車全像顯示器市場:按組件、尺寸、解析度類型、技術類型、顯示器尺寸、應用、車輛類型、銷售管道類型分類,全球預測,2026-2032年 全像顯示市場分析及至2035年預測:按類型、產品、技術、組件、應用、材料類型、設備、製程、最終用戶及安裝類型分類

全像顯示市場分析及至2035年預測:按類型、產品、技術、組件、應用、材料類型、設備、製程、最終用戶及安裝類型分類 全球全像顯示器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全像顯示器市場報告

全球全像顯示器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全像顯示器市場報告 全像顯示器市場規模、佔有率和成長分析(按組件、產品、技術、尺寸、應用和地區分類)—2026-2033年產業預測

全像顯示器市場規模、佔有率和成長分析(按組件、產品、技術、尺寸、應用和地區分類)—2026-2033年產業預測 全像顯示器市場-全球產業規模、佔有率、趨勢、機會和預測,按產品類型、技術、最終用戶、地區和競爭格局分類,2020-2030年預測

全像顯示器市場-全球產業規模、佔有率、趨勢、機會和預測,按產品類型、技術、最終用戶、地區和競爭格局分類,2020-2030年預測 全像顯示市場報告(按組件、技術、尺寸、應用、最終用戶和地區)2025-2033

全像顯示市場報告(按組件、技術、尺寸、應用、最終用戶和地區)2025-2033