|

市場調查報告書

商品編碼

2027596

農業微量營養素市場機會、成長要素、產業趨勢分析及2026-2035年預測Agricultural Micronutrients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

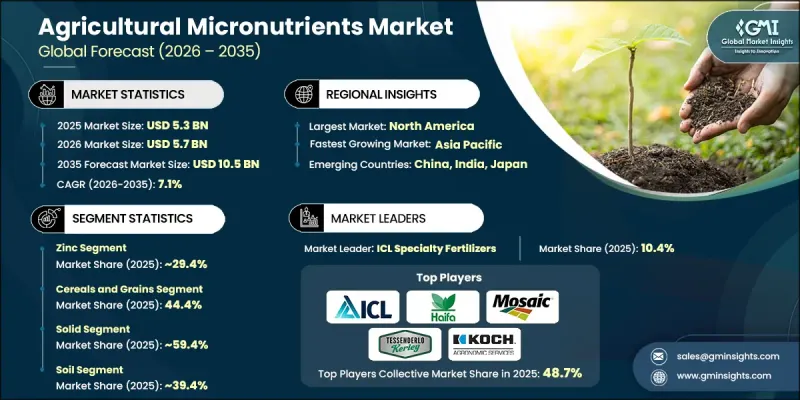

2025年全球農業微量營養素市場規模預計為53億美元,預計到2035年將以7.1%的複合年成長率成長至105億美元。

在全球農業領域,隨著人們越來越重視提高作物產量和土壤健康,市場正在不斷擴大。鋅、鐵、錳、硼、銅、鉬和鎳等農業微量元素即使在微量的情況下,也能在支持植物生長方面發揮關鍵作用,並對作物發育、抗逆性和產量產生顯著影響。農民對土壤養分缺乏問題的認知不斷提高,推動了富含微量元素肥料的使用。在新興經濟體,尤其是在面臨土壤劣化普遍問題的地區,這些肥料的使用正在加速成長。向永續和有機農業的轉型進一步刺激了需求,因為生產者致力於採用環保方法來提高土壤肥力。營養配方技術的不斷進步,包括具有更高生物利用度的螯合產品,正在提高肥料的效率和作物反應。這些微量元素支持酵素活化、光合作用和養分吸收等重要的生理功能,增強作物對乾旱和鹽鹼化等環境壓力的耐受性,並有助於全面提高農業產量和品質。

| 市場規模 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 53億美元 |

| 預測金額 | 105億美元 |

| 複合年成長率 | 7.1% |

預計到2025年,穀物市佔率將達到44.4%,並在2035年之前以6.7%的複合年成長率成長。其主導地位源自於穀物作為主糧作物的地位,而微量元素的施用對於提高產量穩定性和作物抗逆性至關重要。穀物種植中微量元素施用量的增加正在提高生產力,並有助於實現全球糧食安全目標。

預計到2025年,固態形態的微量元素肥料將佔據59.4%的市場佔有率,並在2026年至2035年間以6.8%的複合年成長率成長。儘管市場正逐漸轉向液體配方,但由於固體微量元素肥料具有保存期限長、易於儲存和適合土壤施用等優點,因此仍被廣泛使用。然而,液體配方肥料因其吸收速度更快以及與現代營養輸送系統(如灌溉施肥和葉面噴布)的兼容性而日益受到歡迎。

預計到2025年,北美農業微量元素市場將佔全球市場佔有率的34.9%。這一成長主要得益於先進農業實踐和精密農業技術的積極應用。人們對永續營養管理和環境效率的日益關注也進一步推動了市場需求。美國和加拿大在螯合態和液態微量元素溶液的應用方面處於領先地位,尤其是在高價值和特種作物領域。同時,人們對有機農業的日益關注也推動了向環境友善農業材料的轉變。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 鋅

- 硼

- 錳

- 鐵

- 鉬

- 銅

- 其他

第6章 市場估算與預測:依作物類型分類,2022-2035年

- 糧食

- 油籽和豆類

- 水果和蔬菜

- 其他

第7章 市場估計與預測:依類型分類,2022-2035年

- 固體的

- 液體

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 土壤

- 葉面噴布

- 施肥和灌溉

第9章 市場估價與預測:依最終用戶分類,2022-2035年

- 商業農場/大規模農業

- 中小農場

- 溫室和可控制環境農業

- 草坪和觀賞植物

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第11章:公司簡介

- Agricen

- AgroLiquid

- Atlantica Agricola

- Brandt Consolidated

- Haifa Group

- Helena Agri-Enterprises

- ICL Specialty Fertilizers

- Koch Agronomic Services

- Micromix Plant Health

- Miller Chemical

- NACHURS Alpine Solutions

- SAN Agrow

- Tessenderlo Kerley

- The Mosaic Company

- WUXAL

The Global Agricultural Micronutrients Market was valued at USD 5.3 billion in 2025 and is estimated to grow at a CAGR of 7.1% to reach USD 10.5 billion by 2035.

The market is witnessing expansion as global agriculture intensifies its focus on improving crop productivity and soil health. Agricultural micronutrients such as zinc, iron, manganese, boron, copper, molybdenum, and nickel play a crucial role in supporting plant growth in extremely small quantities, yet they significantly influence crop development, resistance to stress, and yield performance. Rising awareness among farmers regarding soil nutrient deficiencies is encouraging wider adoption of micronutrient-based fertilizers. Emerging economies, particularly in regions facing widespread soil depletion, are showing strong uptake of these inputs. The shift toward sustainable and organic farming practices is further boosting demand as growers aim to improve soil fertility using environmentally responsible methods. Continuous advancements in nutrient formulation technologies, including chelated products with enhanced bioavailability, are improving efficiency and crop response. These micronutrients also support essential physiological functions such as enzyme activation, photosynthesis, and nutrient absorption, helping improve crop resilience against environmental stressors like drought and salinity while enhancing overall agricultural output and quality.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.3 Billion |

| Forecast Value | $10.5 Billion |

| CAGR | 7.1% |

The cereals and grains segment accounted for 44.4% share in 2025 and is expected to grow at a CAGR of 6.7% through 2035. Their dominance is attributed to their status as staple food crops, where micronutrient application is essential to improve yield stability and crop resilience. Increasing adoption in grain cultivation is enhancing productivity and supporting food security objectives globally.

The solid form segment held a 59.4% share in 2025 and is projected to grow at a CAGR of 6.8% during 2026-2035. Despite the growing shift toward liquid formulations, solid micronutrients continue to be widely used due to their longer shelf life, ease of storage, and suitability for soil-based applications. However, liquid formulations are gaining traction due to faster absorption rates and compatibility with modern nutrient delivery systems such as fertigation and foliar application.

North America Agricultural Micronutrients Market accounted for 34.9% of the global share in 2025. Growth in the region is supported by advanced farming practices and strong adoption of precision agriculture technologies. Increasing focus on sustainable nutrient management and environmental efficiency is further driving demand. The United States and Canada are leading adopters of chelated and liquid micronutrient solutions, particularly for high-value and specialty crops, while growing interest in organic farming practices is reinforcing the shift toward eco-friendly agricultural inputs.

Key companies operating in the Global Agricultural Micronutrients Market include Haifa Group, The Mosaic Company, Koch Agronomic Services, ICL Specialty Fertilizers, Helena Agri-Enterprises, Tessenderlo Kerley, Brandt Consolidated, Miller Chemical, AgroLiquid, NACHURS Alpine Solutions, SAN Agrow, Agricen, Atlantica Agricola, Micromix Plant Health, and WUXAL. Companies in the Global Agricultural Micronutrients Market are strengthening their competitive position through innovation in formulation technologies and expansion of product portfolios. Significant investments are being directed toward developing chelated and highly bioavailable micronutrient solutions that improve crop efficiency and soil absorption. Strategic collaborations with distributors and agricultural service providers are enhancing market penetration. Firms are also focusing on expanding production capacities to meet rising global demand. Increasing emphasis on sustainable agriculture is driving companies to develop eco-friendly and organic-compatible products. Additionally, businesses are leveraging digital agriculture platforms and agronomic advisory services to improve farmer engagement and promote precision nutrient application practices, thereby enhancing long-term customer loyalty and market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Crop type

- 2.2.4 Form

- 2.2.5 Application

- 2.2.6 End user

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Zinc

- 5.3 Boron

- 5.4 Manganese

- 5.5 Iron

- 5.6 Molybdenum

- 5.7 Copper

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Crop Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cereals and grains

- 6.3 Oilseeds and pulses

- 6.4 Fruits and vegetables

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Solid

- 7.3 Liquid

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Soil

- 8.3 Foliar

- 8.4 Fertigation

Chapter 9 Market Estimates and Forecast, By End User, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Commercial farms/large-scale agriculture

- 9.3 Small & medium farms

- 9.4 Greenhouse & controlled environment agriculture

- 9.5 Turf & ornamentals

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Agricen

- 11.2 AgroLiquid

- 11.3 Atlantica Agricola

- 11.4 Brandt Consolidated

- 11.5 Haifa Group

- 11.6 Helena Agri-Enterprises

- 11.7 ICL Specialty Fertilizers

- 11.8 Koch Agronomic Services

- 11.9 Micromix Plant Health

- 11.10 Miller Chemical

- 11.11 NACHURS Alpine Solutions

- 11.12 SAN Agrow

- 11.13 Tessenderlo Kerley

- 11.14 The Mosaic Company

- 11.15 WUXAL

作物微量元素:全球市場

作物微量元素:全球市場 農業次要營養元素市場分析及預測(至2035年):類型、產品、應用、形式、技術、最終用戶、成分、製程、服務和設備

農業次要營養元素市場分析及預測(至2035年):類型、產品、應用、形式、技術、最終用戶、成分、製程、服務和設備 全球微量營養素市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球農業微量元素市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球微量營養素市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球農業微量元素市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 農業螯合鐵微量元素市場報告:按應用和地區分類

農業螯合鐵微量元素市場報告:按應用和地區分類 全球作物營養解決方案市場預測(至2032年):按產品類型、配方、作物類型、分銷管道、應用方法、最終用戶和地區分類

全球作物營養解決方案市場預測(至2032年):按產品類型、配方、作物類型、分銷管道、應用方法、最終用戶和地區分類 螯合鐵農業微量營養素市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、地區和競爭格局分類,2021-2031年農業微量元素市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、作物類型、形態、應用方式、地區和競爭格局分類,2020-2030年預測全球農業微量元素市場-2025年至2030年預測

螯合鐵農業微量營養素市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、地區和競爭格局分類,2021-2031年農業微量元素市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、作物類型、形態、應用方式、地區和競爭格局分類,2020-2030年預測全球農業微量元素市場-2025年至2030年預測 全球含硫微量營養素市場

全球含硫微量營養素市場