|

市場調查報告書

商品編碼

2027592

果味水市場機會、成長要素、產業趨勢分析及2026-2035年預測。Fruit Infused Water Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

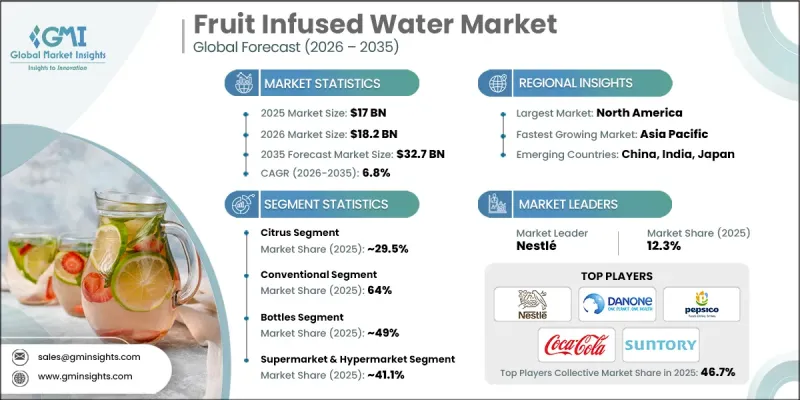

預計到 2025 年,全球水果浸泡水市場價值將達到 170 億美元,並預計以 6.8% 的複合年成長率成長,到 2035 年達到 327 億美元。

隨著消費者越來越傾向於選擇更健康、天然風味的飲品,果味水產業正穩步擴張。人們對健康和正確飲水習慣的日益重視,正推動消費者從含糖飲料轉向更健康的飲品。果味水兼具清爽口感和健康益處,已成為機能飲料市場的重要組成部分。果味水低卡路里,符合現代消費者對天然成分和透明度的食品偏好。其成分符合「潔淨標示」的要求,無需添加人工添加劑。除了補水之外,這些飲品還富含源自天然成分的營養物質,有助於整體健康,並支持積極的生活方式。消費者對便利即飲型果味水的需求不斷成長,進一步推動了其在多個終端應用領域的市場需求。隨著消費者對健康消費的重視程度不斷提高,全球果味水市場預計將保持強勁的成長動能。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 170億美元 |

| 預計金額 | 327億美元 |

| 複合年成長率 | 6.8% |

預計到2025年,柑橘口味飲料的市佔率將達到29.5%,並在2035年之前以6.5%的複合年成長率成長。該口味憑藉其清爽的口感和強大的消費者支持,持續引領市場。市場口味趨勢反映出消費者越來越偏好兼具美味和健康益處的天然功能性產品。隨著消費者在追求更健康飲品的同時,也更加重視產品的多樣性和更豐富的感官體驗,對水果口味飲料的需求持續成長。

預計到2025年,瓶裝產品將佔據49%的市場佔有率,並在2035年之前以6.5%的複合年成長率成長。隨著消費者越來越重視便利性、便攜性和永續性,包裝創新仍是市場擴張的關鍵驅動力。瓶裝產品因其易用性和在零售通路的廣泛覆蓋而繼續佔據市場主導地位。隨著環保意識的增強,輕質和可回收材料越來越受歡迎。替代包裝形式也在不斷發展,以滿足消費者多樣化的需求,從而促進了整體市場的發展。

預計到2025年,超級市場和大賣場市佔率將達到41.1%,並在2035年之前以7.1%的複合年成長率成長。這些零售通路憑藉其覆蓋範圍廣、產品種類豐富的優勢,仍是主要的銷售平台。它們在提升品牌知名度、為消費者提供一站式購物體驗方面發揮著至關重要的作用。零售網路的擴張和消費者購買行為的改變正在進一步推動這一領域的成長。

預計到2025年,北美果味水市佔率將達到33.5%,這主要得益於消費者對天然低卡路里飲料的需求不斷成長,以及意識提升。消費者積極尋找符合偏好的產品,例如潔淨標示、無糖等。口味研發和包裝設計的創新正在提升品牌吸引力。零售和線上通路的拓展,也帶動了消費者隨時隨地飲用果味水的趨勢,持續推動本地市場的需求成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依口味分類,2022-2035年

- 柑橘

- 檸檬

- 萊姆

- 橘子

- 柚子

- 莓果

- 草莓

- 藍莓

- 覆盆子

- 黑莓

- 熱帶水果

- 芒果

- 鳳梨

- 百香果

- 番石榴

- 蘋果和梨

- 其他

第6章 市場估計與預測:依類別分類,2022-2035年

- 有機的

- 傳統的

第7章 市場估價與預測:依包裝類型分類,2022-2035年

- 瓶子

- 能

- 水壺

- 小袋

第8章 市場估算與預測:依通路分類,2022-2035年

- 超級市場和大賣場

- 便利商店

- 線上零售

- 其他(例如,直接銷售、自動販賣機)

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- Bai Brands

- Danone

- Flow Water

- Hint Inc.

- JUST Water

- LaCroix Beverages, Inc.

- Mountain Valley Spring Water

- Nestle

- Ozarka Water(BlueTriton Brands)

- PATH Water

- PepsiCo

- Primo Brands

- Sanzo

- SUNTORY BEVERAGE & FOOD LIMITED.

- The Coca-Cola Company

The Global Fruit Infused Water Market was valued at USD 17 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 32.7 billion by 2035.

The fruit infused water industry has been expanding steadily as consumers increasingly gravitate toward healthier, naturally flavored hydration choices. Rising awareness of wellness and proper hydration habits is encouraging a shift away from sugar-loaded beverages toward cleaner alternatives. This category has become a key part of the functional beverage space, offering both refreshment and perceived health support. Fruit-infused water delivers a low-calorie option that aligns with modern dietary preferences focused on natural ingredients and transparency. Its composition supports clean-label expectations while eliminating the need for artificial additives. In addition to hydration, these beverages are associated with added nutritional value derived from infused ingredients, contributing to overall well-being and supporting active lifestyles. The growing appeal of convenient, ready-to-drink formats is further accelerating demand across multiple end-use sectors. As consumer priorities continue to evolve toward health-conscious consumption, the global fruit infused water market is expected to maintain strong growth momentum.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17 Billion |

| Forecast Value | $32.7 Billion |

| CAGR | 6.8% |

In 2025, the citrus flavors segment accounted for 29.5% share and is projected to grow at a CAGR of 6.5% through 2035. This segment continues to lead due to its refreshing taste profile and strong consumer acceptance. Flavor trends within the market reflect a growing preference for natural and functional options that combine taste with perceived wellness benefits. Demand for fruit-based flavor profiles continues to rise as consumers seek variety and enhanced sensory experiences while maintaining a focus on healthier beverage choices.

The bottles segment held a share of 49% in 2025 and is expected to grow at a CAGR of 6.5% through 2035. Packaging innovation remains a key factor driving market expansion, as consumers prioritize convenience, portability, and sustainability. Bottles continue to dominate due to ease of use and widespread availability across retail channels. Lightweight and recyclable materials are gaining preference as environmental awareness increases. Alternative packaging formats are also evolving to meet diverse consumer needs, contributing to overall market development.

The supermarkets and hypermarkets segment accounted for 41.1% share in 2025 and is projected to grow at a CAGR of 7.1% through 2035. These retail channels remain the primary distribution platforms due to their broad reach and ability to offer extensive product selections. They play a critical role in enhancing brand visibility and enabling consumers to access a wide range of options in one location. Expanding retail networks and changing purchasing behaviors are further supporting growth in this segment.

North America Fruit Infused Water Market held a 33.5% share in 2025, driven by increasing demand for natural, low-calorie beverages and rising awareness of health and wellness. Consumers are actively seeking products that align with clean-label and sugar-free preferences. Innovation in flavor development and packaging design is helping brands strengthen their appeal. The growing trend of on-the-go consumption, supported by expanding retail and online distribution channels, continues to drive regional demand.

Key players operating in the Global Fruit Infused Water Market include PepsiCo, The Coca-Cola Company, Nestle, Danone, SUNTORY BEVERAGE & FOOD LIMITED, LaCroix Beverages, Inc., Hint Inc., Bai Brands, JUST Water, PATH Water, Flow Water, Primo Brands, Ozarka Water (BlueTriton Brands), Mountain Valley Spring Water, and Sanzo. Companies in the Fruit Infused Water Market are reinforcing their market position through innovation, branding, and strategic expansion. They are introducing new flavor profiles and clean-label formulations to meet evolving consumer preferences. Investments in sustainable packaging and environmentally responsible practices are helping companies align with growing eco-conscious demand. Strategic partnerships and distribution expansions are enabling broader market reach and improved product accessibility. Additionally, companies are strengthening their digital presence and leveraging e-commerce platforms to capture changing purchasing behaviors while focusing on product differentiation and premium positioning to enhance brand loyalty and competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Flavor type

- 2.2.3 Category

- 2.2.4 Packaging type

- 2.2.5 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Flavor Type, 2022-2035 (USD Billion) (Thousand Liters)

- 5.1 Key trends

- 5.2 Citrus

- 5.2.1 Lemon

- 5.2.2 Lime

- 5.2.3 Orange

- 5.2.4 Grapefruit

- 5.3 Berries

- 5.3.1 Strawberry

- 5.3.2 Blueberry

- 5.3.3 Raspberry

- 5.3.4 Blackberry

- 5.4 Tropical Fruits

- 5.4.1 Mango

- 5.4.2 Pineapple

- 5.4.3 Passion Fruit

- 5.4.4 Guava

- 5.5 Apples and Pears

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Category, 2022-2035 (USD Billion) (Thousand Liters)

- 6.1 Key trends

- 6.2 Organic

- 6.3 Conventional

Chapter 7 Market Estimates and Forecast, By Packaging Type, 2022-2035 (USD Billion) (Thousand Liters)

- 7.1 Key trends

- 7.2 Bottles

- 7.3 Cans

- 7.4 Jugs

- 7.5 Pouches

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Liters)

- 8.1 Key trends

- 8.2 Supermarkets and hypermarkets

- 8.3 Convenience stores

- 8.4 Online retail

- 8.5 Others (e.g., direct sales, vending machines)

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Thousand Liters)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Bai Brands

- 10.2 Danone

- 10.3 Flow Water

- 10.4 Hint Inc.

- 10.5 JUST Water

- 10.6 LaCroix Beverages, Inc.

- 10.7 Mountain Valley Spring Water

- 10.8 Nestle

- 10.9 Ozarka Water (BlueTriton Brands)

- 10.10 PATH Water

- 10.11 PepsiCo

- 10.12 Primo Brands

- 10.13 Sanzo

- 10.14 SUNTORY BEVERAGE & FOOD LIMITED.

- 10.15 The Coca-Cola Company