|

市場調查報告書

商品編碼

2027590

2026 年至 2035 年建築平板玻璃的市場機會、成長要素、產業趨勢與預測。Architectural Flat Glass Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

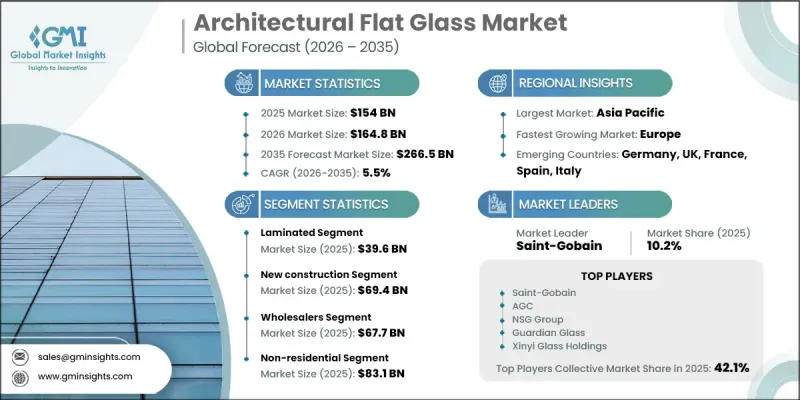

預計到 2025 年,全球建築平板玻璃市場價值將達到 1,540 億美元,並預計以 5.5% 的複合年成長率成長,到 2035 年達到 2,665 億美元。

在現代建築領域,隨著兼顧性能、設計和能源效率的先進材料日益普及,市場持續成長。建築平板玻璃以均質板材的形式生產,憑藉其透明性、結構適應性和提升視覺美感的能力,在現代建築中扮演著至關重要的角色。其廣泛應用源自於人們對最佳化自然採光、提升隔熱性能和打造美觀建築外觀的日益成長的需求。塗層技術和製造流程的進步顯著提升了建築平板玻璃的隔熱性能、太陽輻射控制和隔音效果,使其成為不斷發展的建築設計中的首選解決方案。此材料廣泛應用於住宅和商業基礎設施,協助節能環保永續建築的建設。此外,隨著都市化的加速和基礎設施投資的增加,市場需求持續成長,而玻璃系統的不斷創新和設計的柔軟性也在不斷塑造建築平板玻璃市場的競爭格局和長期成長軌跡。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 1540億美元 |

| 預測金額 | 2665億美元 |

| 複合年成長率 | 5.5% |

預計到2025年,受全球基礎建設不斷成長的推動,新建建築市場規模將達到694億美元。建築公司優先考慮高性能材料,以確保新建築的耐久性、效率和長期營運價值。建築用平板玻璃在實現這些目標中發揮核心作用,有助於提升建築性能和改善居住者體驗。除了新建項目外,維修和整修項目也推動了對平板玻璃的需求,因為業主希望提高能源效率並實現現有建築的現代化。平板玻璃的多功能性使其可應用於各種結構構件,進而提升建築專案的功能性和視覺效果。

預計到2025年,批發市場規模將達到677億美元。批發商透過確保為複雜的建設活動提供各種規格的玻璃,從而促進大規模分銷。他們管理庫存、物流和按時交貨的能力,幫助承包商和加工商按時完成專案並達到品質標準。這個分銷網路加強了市場准入,促進了製造商和終端用戶之間的高效合作,從而支持了整個行業的成長。

2025年北美建築平板玻璃市場規模為184億美元,預計2035年將達314億美元。該地區對能夠提升能源效率和建築性能的先進玻璃系統需求日益成長。創新的幕牆設計和高性能鍍膜玻璃的廣泛應用正在塑造全部區域的建築趨勢。美國持續引領區域需求,這主要得益於住宅翻新和商業開發項目的持續推進,這些項目優先考慮提高隔熱性能、最佳化照明以及融入現代設計。人們對永續建築實踐和監管標準的日益關注,進一步加速了先進平板玻璃解決方案的普及應用。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 利用自然光進行設計的需求日益成長。

- 在現代建築立面上的應用日益增多

- 利用新型玻璃產品擴大維修活動

- 陷阱與挑戰

- 如果不採取適當的隔熱措施,能源損失將非常嚴重。

- 運輸和安裝過程中存在損壞風險

- 機會

- 人們對智慧嵌裝玻璃解決方案的興趣日益濃厚

- 採用節能建築材料

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 夾層玻璃

- 強化玻璃

- 普通浮法玻璃

- 雙層玻璃窗

- 裝飾性的

- 反射玻璃

- 棱鏡玻璃和低輻射玻璃

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 新建工程

- 維修

- 室內施工

第7章 市場估價與預測:依銷售管道分類,2022-2035年

- 批發商

- 線上

- 零售商

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 住宅

- 非住宅

- 辦公室

- 零售空間

- 飯店業

- 公共設施

- 醫療設施

- 教育機構

- 交通設施

- 娛樂設施

- 其他

- 工業的

- 製造工廠

- 倉庫

- 彈性空間大樓

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- AGC

- Asahi India Glass

- Cardinal Glass Industries

- Central Glass

- China Glass Holdings

- CSG Holding

- Saint-Gobain

- Guardian Glass

- NSG Group

- Xinyi Glass Holdings

The Global Architectural Flat Glass Market was valued at USD 154 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 266.5 billion by 2035.

The market continues to gain momentum as modern construction increasingly integrates advanced materials that balance performance, design, and energy efficiency. Architectural flat glass, manufactured in uniform sheet form, plays a critical role in contemporary buildings due to its ability to deliver transparency, structural adaptability, and enhanced visual appeal. Its widespread adoption is driven by the growing need for natural light optimization, improved insulation, and aesthetically refined building envelopes. Advancements in coating technologies and fabrication processes have significantly improved thermal performance, solar control, and acoustic insulation, making flat glass a preferred solution in evolving architectural designs. The material is extensively utilized across both residential and commercial infrastructure, supporting the development of energy-efficient and sustainable buildings. In addition, rising urbanization and infrastructure investments are further reinforcing demand, while continuous innovation in glazing systems and design flexibility continues to shape the competitive landscape and long-term growth trajectory of the architectural flat glass market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $154 Billion |

| Forecast Value | $266.5 Billion |

| CAGR | 5.5% |

The new construction segment accounted for USD 69.4 billion in 2025 owing to the increasing volume of global infrastructure development. Builders prioritize high-performance materials that ensure durability, efficiency, and long-term operational value in newly developed structures. Architectural flat glass plays a central role in achieving these objectives by contributing to improved building performance and enhanced occupant experience. Alongside new developments, renovation and upgrade projects are also contributing to demand as property owners seek to enhance energy efficiency and modernize existing structures. The versatility of flat glass enables its application across various structural elements, supporting both functional and visual enhancements in construction projects.

The wholesaler segment generated USD 67.7 billion in 2025. Wholesalers facilitate large-scale distribution by ensuring consistent availability of diverse glass specifications required for complex construction activities. Their ability to manage inventory, logistics, and timely delivery supports contractors and fabricators in meeting project deadlines and quality standards. This distribution network strengthens market accessibility and enables efficient coordination between manufacturers and end users, thereby supporting overall industry growth.

North America Architectural Flat Glass Market was valued at USD 18.4 billion in 2025 and is anticipated to reach USD 31.4 billion by 2035. The region is witnessing rising demand for advanced glazing systems that enhance energy efficiency and building performance. Increasing adoption of innovative facade designs and high-performance coated glass is shaping construction trends across the region. The United States continues to drive regional demand, supported by ongoing residential upgrades and commercial development projects that emphasize improved insulation, daylight optimization, and modern design integration. Growing awareness of sustainable construction practices and regulatory standards is further accelerating the adoption of technologically advanced flat glass solutions.

Key companies operating in the Global Architectural Flat Glass Industry include Saint-Gobain, AGC, Guardian Glass, NSG Group, Xinyi Glass Holdings, Asahi India Glass, Central Glass, China Glass Holdings, CSG Holding, and Cardinal Glass Industries. Companies in the Architectural Flat Glass Market are strengthening their competitive position through continuous investment in advanced manufacturing technologies and product innovation. Many players are focusing on developing energy-efficient and high-performance glass solutions that align with evolving building standards and sustainability requirements. Strategic collaborations with construction firms and real estate developers are enabling companies to expand their project pipelines and enhance market reach. In addition, businesses are optimizing supply chain operations and expanding production capacities to meet rising global demand. Geographic expansion into emerging markets and diversification of product portfolios are also key approaches. Furthermore, companies are prioritizing research in coatings, smart glass technologies, and recyclable materials to maintain long-term competitiveness and reinforce their market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product

- 2.2.2 Application

- 2.2.3 Sales Channel

- 2.2.4 End Use

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for daylight-focused designs

- 3.2.1.2 Rising use in modern building facades

- 3.2.1.3 Expanding renovation activities using new glazing

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 High energy-loss without proper insulation

- 3.2.2.2 Breakage risk during transport and installation

- 3.2.3 Opportunities

- 3.2.3.1 Growing interest in smart glazing solutions

- 3.2.3.2 Adoption of energy-efficient building materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Laminated

- 5.3 Tempered

- 5.4 Basic Float

- 5.5 Insulating

- 5.6 Decorative

- 5.7 Reflective

- 5.8 Prism & low-emissivity glass

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 New construction

- 6.3 Refurbishment

- 6.4 Interior construction

Chapter 7 Market Estimates and Forecast, By Sales Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Wholesalers

- 7.3 Online

- 7.4 Retailer

Chapter 8 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Non-Residential

- 8.3.1 Offices

- 8.3.2 Retail Spaces

- 8.3.3 Hospitality

- 8.3.3.1 Institutional

- 8.3.3.2 Healthcare facilities

- 8.3.3.3 Educational institutes

- 8.3.3.4 Transport facilities

- 8.3.3.5 Entertainment facilities

- 8.3.3.6 Others

- 8.4 Industrial

- 8.4.1 Manufacturing Facilities

- 8.4.2 Warehouses

- 8.4.3 Flex Space Buildings

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 AGC

- 10.2 Asahi India Glass

- 10.3 Cardinal Glass Industries

- 10.4 Central Glass

- 10.5 China Glass Holdings

- 10.6 CSG Holding

- 10.7 Saint-Gobain

- 10.8 Guardian Glass

- 10.9 NSG Group

- 10.10 Xinyi Glass Holdings