|

市場調查報告書

商品編碼

2027589

2026 年至 2035 年休閒和戶外產品的市場機會、成長要素、產業趨勢和預測。Recreational and Outdoor Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

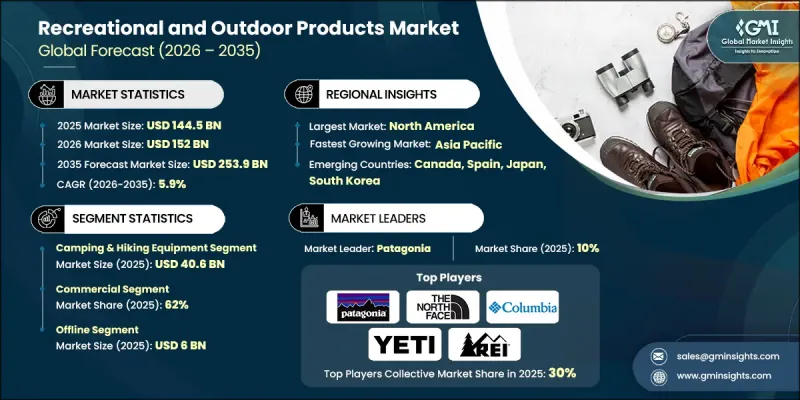

2025年全球休閒和戶外產品市場價值為1445億美元,預計到2035年將以5.9%的複合年成長率成長至2539億美元。

隨著消費者越來越重視身心健康,健行、跑步、騎乘和散步等戶外活動已成為他們日常生活的重要組成部分。人們普遍認為,戶外活動是緩解壓力、改善情緒、維持健康平衡生活方式的有效方法。與室內運動不同,戶外活動能帶來自由感和與大自然的連結,進而鼓勵人們持續參與。各個年齡層的人們都在參與各種各樣的戶外活動,從休閒散步到挑戰性徒步,總有一款適合他們的體能水平和舒適度。社交健身社群、穿戴式科技和以健康為導向的行銷活動正在推動這些習慣的養成,並提升了人們對耐用、舒適、高性能裝備的需求。如今,消費者追求多功能戶外裝備、透氣服裝、支撐鞋履以及能夠無縫融入日常健康生活方式的多功能工具,使戶外休閒成為不可或缺的生活方式選擇。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 1445億美元 |

| 預測金額 | 2539億美元 |

| 複合年成長率 | 5.9% |

到2025年,露營和健行裝備市場規模將達到406億美元。消費者對兼具耐用性和輕便性的裝備的需求日益成長,以應對各種地形和天氣條件。最新的帳篷、睡袋系統、可調式登山杖和透氣背包在設計時充分考慮了便攜性、多功能性和可靠性,旨在滿足從休閒週末探險者到長期戶外旅行專業人士等各類人群的需求。產品研發的重點在於提升舒適性和便利性,同時又不犧牲功能性,從而支持從休閒到專業戶外活動的各種需求。

到2025年,線下銷售管道的銷售額將達到60億美元。實體店銷售依然重要,因為消費者希望在購買前親身觸摸和檢查產品。戶外用品專賣店、運動用品連鎖店和品牌自營店都允許顧客試穿產品,體驗其合身度、耐用性和技術特性。這種親身體驗有助於買家做出明智的決定,尤其是在購買複雜的高性能裝備時。

到2025年,美國休閒和戶外用品市場規模將達444億美元,市佔率高達84.6%。人們對戶外休閒日益成長的興趣,以及由此帶來的健康益處、壓力緩解和生活方式提升,正在推動市場需求。消費者持續購買露營和健行裝備、功能性服裝以及適合週末探險和日常戶外活動的各種多功能配件。探險旅行、國家公園探索和以健康為導向的休閒也進一步支撐了這項旺盛的需求。美國零售生態系統能夠為不同技能水平的用戶提供適用於各種戶外活動的先進且可客製化的產品。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 健康、養生和積極生活方式的興起

- 探險旅遊的發展

- 材料和設計的創新

- 產業潛在風險與挑戰

- 需求的季節性和波動

- 供應鏈的複雜性

- 機會

- 產品個人化和客製化設備

- 智慧互聯戶外技術

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特的分析

- PESTEL 分析

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 各地區價格波動及其影響因素

- 貿易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 主要進口國和出口國

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 個性化產品建議

- 人工智慧驅動的設計和原型製作

- 戶外電子設備的預測性維護

- 用於客戶服務的聊天機器人和虛擬助手

- 風險、限制和監管考量

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 露營和健行裝備

- 帳篷

- 睡袋

- 背包

- 登山杖

- 露營爐

- 其他物品(燈籠等)

- 體育及戶外用品

- 自行車

- 滑板

- 槳板

- 滑雪和單板滑雪裝備

- 攀岩裝備

- 其他(例如皮划艇)

- 漁具

- 戶外服裝和鞋類

- 登山靴

- 戶外夾克

- 戶外褲

- 其他物品(手套、帽子等)

- 戶外電子設備

- GPS系統

- 頭燈

- 太陽能充電器

- 戶外智慧型手錶

- 其他(健身追蹤器等)

- 其他物品(馬術裝備等)

第6章 市場估計與預測:依價格分類,2022-2035年

- 低價位

- 中等的

- 高的

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 個人

- 專業的

第8章 市場估算與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 企業網站

- 離線

- 大賣場/超級市場

- 專賣店

- 其他(例如獨立經營零售商店)

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Clarus

- Columbia Sportswear

- Deckers Outdoor

- Foot Locker

- Garmin

- Johnson Outdoors

- Marmot

- Newell Brands

- Patagonia

- REI

- Sporting Goods Corporation

- The North Face

- Topgolf Callaway Brands

- Wolverine Worldwide

- Yeti

The Global Recreational and Outdoor Products Market was valued at USD 144.5 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 253.9 billion by 2035.

Consumers are increasingly prioritizing both physical and mental well-being, making outdoor activities such as hiking, running, cycling, and walking a central part of daily routines. Spending time outside is now perceived as a practical way to reduce stress, boost mood, and maintain a balanced lifestyle. Unlike indoor workouts, outdoor activities offer a sense of freedom and connection with nature, encouraging consistent participation. Across all age groups, people are engaging in activities suited to their fitness and comfort levels, from leisurely walks to challenging hikes. Social fitness communities, wearable technology, and wellness-driven marketing have reinforced these habits, increasing demand for durable, comfortable, and high-performance equipment. Consumers now expect versatile outdoor gear, breathable clothing, supportive footwear, and multipurpose tools that integrate seamlessly into everyday wellness routines, transforming outdoor recreation into an essential lifestyle choice.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $144.5 Billion |

| Forecast Value | $253.9 Billion |

| CAGR | 5.9% |

In 2025, the camping and hiking equipment segment reached USD 40.6 billion. Consumers increasingly seek gear that combines lightweight design with durability to withstand diverse terrains and weather conditions. Modern tents, sleeping systems, adjustable trekking poles, and ventilated backpacks are engineered for mobility, versatility, and reliability, catering to casual weekend adventurers as well as professionals undertaking extended outdoor trips. The focus is on creating products that enhance comfort and convenience without compromising functionality, supporting both leisure and intensive outdoor activities.

The offline channels segment captured USD 6 billion in 2025. Physical retail remains important as consumers prefer to interact with products before purchase. Specialty outdoor stores, sporting goods chains, and brand-owned outlets allow customers to test fit, durability, and technical features. These hands-on experiences help buyers make confident purchase decisions, especially for complex or high-performance equipment.

U.S. Recreational and Outdoor Products Market accounted for 84.6% share in 2025, generating USD 44.4 billion. Growing interest in outdoor recreation for wellness, stress relief, and lifestyle enrichment drives demand. Consumers continue to purchase camping and hiking gear, performance apparel, and multipurpose accessories suitable for both weekend adventures and everyday outdoor routines. Adventure travel, national park exploration, and wellness-focused recreation further sustain high demand. The U.S. retail ecosystem supports the availability of advanced, customizable products for users of all skill levels across multiple outdoor activities.

Key players in the Global Recreational and Outdoor Products Market include Yeti, Johnson Outdoors, REI, Columbia Sportswear, Wolverine Worldwide, Foot Locker, Topgolf, Callaway Brands, Clarus, Newell Brands, The North Face, Deckers Outdoor, Patagonia, Sporting Goods Corporation, Marmot, and Garmin. Companies in the Recreational and Outdoor Products Market are strengthening their presence through several strategic approaches. They invest heavily in R&D to develop innovative, high-performance, and multi-functional products that enhance user experience. Expansion of both online and offline retail channels allows brands to reach a broader audience while offering personalized purchasing experiences. Marketing strategies leverage wellness-focused messaging, social fitness communities, and influencer partnerships to promote brand visibility. Companies are emphasizing sustainable and eco-friendly product lines to appeal to environmentally conscious consumers. Strategic collaborations, sponsorships, and event activations in outdoor and sports communities further enhance brand recognition and loyalty. Product customization, technology integration, and post-purchase services create lasting consumer engagement and reinforce market foothold.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Price

- 2.2.4 End use

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in health, wellness & active lifestyles

- 3.2.1.2 Growth of adventure tourism

- 3.2.1.3 Innovation in materials & design

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Seasonality & demand volatility

- 3.2.2.2 Supply chain complexity

- 3.2.3 Opportunities

- 3.2.3.1 Product personalization & custom equipment

- 3.2.3.2 Smart & connected outdoor technology

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9.3 Regional price variation & factors

- 3.10 Trade data analysis (driven by paid data base)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.10.3 Top importing & exporting countries

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.2.1 Personalized product recommendations

- 3.11.2.2 Ai-powered design & prototyping

- 3.11.2.3 Predictive maintenance for outdoor electronics

- 3.11.2.4 Chatbot & virtual assistant for customer service

- 3.11.3 Risks, limitations & regulatory considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Camping & hiking equipment

- 5.2.1 Tents

- 5.2.2 Sleeping bags

- 5.2.3 Backpacks

- 5.2.4 Hiking poles

- 5.2.5 Camping stoves

- 5.2.6 Others (lanterns etc.)

- 5.3 Sports & outdoor gear

- 5.3.1 Bicycles

- 5.3.2 Skateboards

- 5.3.3 Paddle boards

- 5.3.4 Skiing & snowboarding equipment

- 5.3.5 Climbing equipment

- 5.3.6 Others (kayaks etc.)

- 5.4 Fishing gear

- 5.4.1 Outdoor apparel & footwear

- 5.4.2 Hiking boots

- 5.4.3 Outdoor jackets

- 5.4.4 Outdoor pants

- 5.4.5 Others (gloves, hats etc.)

- 5.5 Outdoor electronics

- 5.5.1 GPS systems

- 5.5.2 Headlamps

- 5.5.3 Solar-powered chargers

- 5.5.4 Outdoor smartwatches

- 5.5.5 Others (fitness trackers etc.)

- 5.6 Others (equestrian products etc.)

Chapter 6 Market Estimates and Forecast, By Price, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low

- 6.3 Mid

- 6.4 High

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Individual

- 7.3 Professional

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-commerce

- 8.2.2 Company websites

- 8.3 Offline

- 8.3.1 Hypermarket/Supermarkets

- 8.3.2 Specialty stores

- 8.3.3 Others (independent retailer, etc.)

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Clarus

- 10.2 Columbia Sportswear

- 10.3 Deckers Outdoor

- 10.4 Foot Locker

- 10.5 Garmin

- 10.6 Johnson Outdoors

- 10.7 Marmot

- 10.8 Newell Brands

- 10.9 Patagonia

- 10.10 REI

- 10.11 Sporting Goods Corporation

- 10.12 The North Face

- 10.13 Topgolf Callaway Brands

- 10.14 Wolverine Worldwide

- 10.15 Yeti

全球戶外生活設施市場:市場規模、佔有率、趨勢和成長分析(2026-2034 年)

全球戶外生活設施市場:市場規模、佔有率、趨勢和成長分析(2026-2034 年) 全球戶外生活設施市場

全球戶外生活設施市場 戶外生活結構市場預測至 2032 年:按類型、材料類型、價格分佈範圍、分銷管道、技術、應用、最終用戶和地區進行的全球分析

戶外生活結構市場預測至 2032 年:按類型、材料類型、價格分佈範圍、分銷管道、技術、應用、最終用戶和地區進行的全球分析 戶外生活結構市場:按產品、按材料、按分銷管道、按地區

戶外生活結構市場:按產品、按材料、按分銷管道、按地區 2024 - 2032 年戶外餐飲產品市場機會、成長動力、產業趨勢分析與預測戶外活動結構市場、機會、成長動力、產業趨勢分析與預測,2024-2032

2024 - 2032 年戶外餐飲產品市場機會、成長動力、產業趨勢分析與預測戶外活動結構市場、機會、成長動力、產業趨勢分析與預測,2024-2032 全球戶外生活結構市場規模研究,按類型、材料類型、最終用途、配銷通路和區域預測 2022-2032

全球戶外生活結構市場規模研究,按類型、材料類型、最終用途、配銷通路和區域預測 2022-2032 戶外生活結構市場(類型:涼棚、涼亭、涼亭或華美達、溫室、涼亭等;材料類型:木材、鋼、鋁、乙烯基等)-全球產業分析、規模、佔有率、成長、趨勢、 2024-2034年預測

戶外生活結構市場(類型:涼棚、涼亭、涼亭或華美達、溫室、涼亭等;材料類型:木材、鋼、鋁、乙烯基等)-全球產業分析、規模、佔有率、成長、趨勢、 2024-2034年預測