|

市場調查報告書

商品編碼

2027586

機器人市場機會、成長要素、產業趨勢分析及2026-2035年預測Robot Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

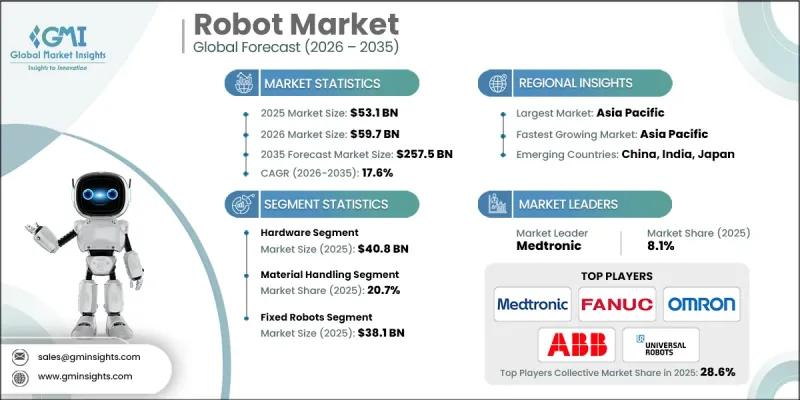

2025年全球機器人市場價值531億美元,預計2035年將達2,575億美元,年複合成長率為17.6%。

市場成長主要得益於機器人、人工智慧和機器學習技術的快速發展,這些技術正在改變各行各業的業務流程。這些技術透過實現更高的自動化程度和精度,重塑了供應鏈營運並增強了面向客戶的系統。現代機器人系統配備了先進的感測功能、智慧運動規劃和增強的適應性,使其能夠高精度地執行複雜任務。企業正擴大採用機器人解決方案,以滿足不斷成長的營運需求、提高效率並縮短處理時間。對更快、更準確的訂單處理的需求日益成長,進一步加速了機器人技術在物流和營運工作流程中的應用。此外,員工生產力和營運擴充性的壓力不斷增加,也促使企業採用能夠處理重複性、體力勞動強度大的任務的自動化解決方案。隨著各行各業持續致力於最佳化效率和績效,預計機器人系統的應用將在全球市場顯著擴展。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 531億美元 |

| 預計金額 | 2575億美元 |

| 複合年成長率 | 17.6% |

預計到2025年,硬體市場規模將達到408億美元。這一成長主要得益於協作機器人的日益普及以及核心機器人組件的持續改進。先進的控制器、執行器和末端執行器使機器人能夠在各種應用場景中實現更精準、更有效率的操作。感測器在提升機器人能力方面發揮著至關重要的作用,它使機器能夠感知周圍環境並自主運作。對能夠執行精細複雜任務的先進機器人系統的需求不斷成長,推動了先進感測技術的應用。這些進步提升了機器人硬體的整體性能和可靠性,進一步鞏固了其在市場中的重要性。

預計到2025年,固定式機器人市場規模將達到381億美元,彰顯其在產業中的強大地位。該市場受益於機器人設計和工程技術的不斷進步,從而提升了性能並拓展了應用領域。固定式機器人系統廣泛應用於需要高精度和高一致性的任務,已成為各種工業流程中不可或缺的一部分。它們能夠精準地執行重複性和危險性任務,在提高生產效率的同時,也增強了職場的安全性。隨著各行業持續投資自動化以提高營運效率,對固定式機器人系統的需求預計將保持強勁。

預計到2025年,北美機器人市佔率將達到110.6%,凸顯其先進且以創新主導的生態系統。該地區自動化技術普及率高,並受益於成熟的機器人開發商、整合商和終端用戶網路。對先進製造和智慧生產環境的大力投資正在推動市場擴張。美國在推動區域成長方面發揮著至關重要的作用,因為它優先考慮提高生產力並應對勞動力挑戰。持續的技術創新和戰略投資有望保持該地區在機器人市場的領先地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 電子商務和物流需求激增

- 人事費用上升和勞動短缺

- 擴大機器人在醫療領域的應用

- 機器人即服務(RaaS)日益普及

- 快速的技術發展

- 產業潛在風險與挑戰

- 前期成本高

- 與機器人相關的技術複雜性

- 市場機遇

- 協作機器人(cobot)在中小企業的普及

- 將人工智慧和機器學習技術整合到機器人技術中

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要公司的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與發展(R&D)

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興/新創競爭對手的發展趨勢

第5章 市場估計與預測:依類型分類,2022-2035年

- 工業機器人

- 關節機器人

- SCARA機器人

- 笛卡兒機器人

- Delta機器人

- 協作機器人(cobots)

- 並聯機器人

- 其他

- 服務機器人

- 個人服務機器人

- 商用服務機器人

第6章 市場估計與預測:依組件分類,2022-2035年

- 硬體

- 機械零件

- 驅動器和驅動部件

- 接頭和軸承系統

- 彈簧和彈性部件

- 緊固和連接部件

- 末端執行器和工具

- 其他

- 電子元件

- 馬達和執行器

- 感應器

- 控制器和處理器

- 電源和電池

- 其他

- 機械零件

- 軟體

- 服務

- 工程和安裝

- 維護和支援

- 培訓和教育

第7章 市場估計與預測:依運輸方式分類,2022-2035年

- 固定機器人

- 移動機器人

- 人形機器人

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 組裝和生產

- 檢驗和品管

- 物料輸送

- 焊接和釬焊

- 包裝和托盤堆垛

- 醫療支援

- 安全監控

- 零售與客戶服務機器人

- 教育

- 其他

第9章 市場估計與預測:依最終用途產業分類,2022-2035年

- 製造業和工業

- 車

- 電子和半導體

- 食品/飲料

- 製藥

- 金屬和機械

- 其他

- 衛生保健

- 防禦

- 農業

- 家用

- 零售與電子商務

- 飯店業

- 後勤

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第11章:公司簡介

- 全球主要公司

- ABB Ltd.

- Fanuc Corporation

- KUKA AG

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Omron Corporation

- Intuitive Surgical

- Medtronic

- 按地區分類的主要公司

- Clearpath Robotics

- MiR(Mobile Industrial Robots)

- Staubli Group

- Universal Robots

- Aethon

- 特殊玩家/干擾者

- Boston Dynamics

- Blue Ocean Robotics

- Ecovacs Robotics

- iRobot Corporation

- Knightscope, Inc.

- Segway Robotics

- SoftBank Robotics

The Global Robot Market was valued at USD 53.1 billion in 2025 and is estimated to grow at a CAGR of 17.6% to reach USD 257.5 billion by 2035.

Market growth is driven by rapid advancements in robotics, artificial intelligence, and machine learning, which are transforming operational processes across industries. These technologies are reshaping supply chain operations and enhancing customer-facing systems by enabling greater automation and precision. Modern robotic systems are designed with advanced sensing capabilities, intelligent motion planning, and enhanced adaptability, allowing them to perform complex tasks with high accuracy. Businesses are increasingly adopting robotic solutions to manage rising operational demands, improve efficiency, and reduce processing time. The growing need for faster and more accurate order handling is further accelerating the integration of robotics into logistics and operational workflows. In addition, increasing pressure on workforce productivity and operational scalability is encouraging organizations to adopt automation solutions that can handle repetitive and physically demanding tasks. As industries continue to focus on efficiency and performance optimization, the adoption of robotic systems is expected to expand significantly across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $53.1 Billion |

| Forecast Value | $257.5 Billion |

| CAGR | 17.6% |

The hardware segment generated USD 40.8 billion in 2025. Growth in this segment is supported by rising adoption of collaborative robots and continuous improvements in core robotic components. Advanced controllers, actuators, and end-effectors are enabling more precise and efficient robotic operations across a wide range of applications. Sensors play a crucial role in enhancing robotic functionality by allowing machines to detect their environment and operate autonomously. Increasing demand for sophisticated robotic systems capable of performing detailed and complex tasks is driving the adoption of advanced sensing technologies. These developments are strengthening the overall performance and reliability of robotic hardware, reinforcing its importance in the market.

The fixed robots segment accounted for USD 38.1 billion in 2025, reflecting its strong presence in the industry. This segment is benefiting from ongoing technological advancements in robotic design and engineering, which are improving performance and expanding application areas. Fixed robotic systems are widely utilized for tasks requiring high precision and consistency, making them essential in various industrial processes. Their ability to perform repetitive and hazardous operations with accuracy enhances workplace safety while improving productivity. As industries continue to invest in automation to achieve operational efficiency, demand for fixed robotic systems is expected to remain strong.

North America Robot Market held a 110.6% share in 2025, highlighting its advanced and innovation-driven ecosystem. The region demonstrates high adoption of automation technologies and benefits from a well-established network of robotics developers, integrators, and end users. Strong investment in advanced manufacturing and smart production environments is supporting market expansion. The United States plays a key role in driving regional growth, supported by an increasing focus on productivity enhancement and the need to address labor-related challenges. Continuous technological advancements and strategic investments are expected to sustain the region's leadership in the robot market.

Key companies operating in the Global Robot Market include ABB Ltd., Aethon, Blue Ocean Robotics, Boston Dynamics, Clearpath Robotics, Ecovacs Robotics, Fanuc Corporation, Intuitive Surgical, iRobot Corporation, Knightscope, Inc., and Medtronic. Companies in the Global Robot Market are strengthening their competitive position through continuous innovation and strategic expansion initiatives. Industry players are investing in advanced technologies such as AI integration, autonomous systems, and enhanced sensing capabilities to improve product performance and expand application areas. Organizations are forming partnerships and collaborations to accelerate research and development efforts and broaden their technological expertise. Market participants are also focusing on expanding their geographic presence and enhancing distribution networks to reach a wider customer base. In addition, companies are prioritizing customization and flexible solutions to meet specific industry requirements.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Component trends

- 2.2.3 Mobility trends

- 2.2.4 Application trends

- 2.2.5 End-use industry trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in e-commerce and logistics demands

- 3.2.1.2 Increasing labor costs and labor shortages

- 3.2.1.3 Rising application of robot in healthcare

- 3.2.1.4 Growing popularity of Robotics-as-a-Service (RaaS)

- 3.2.1.5 Rapid technological developments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost

- 3.2.2.2 Technical complexity associated with robots

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of collaborative robots (cobots) across SMEs

- 3.2.3.2 Integration of AI and machine learning in robotics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Industrial robots

- 5.2.1 Articulated robots

- 5.2.2 Scara robots

- 5.2.3 Cartesian robots

- 5.2.4 Delta robots

- 5.2.5 Collaborative robots (cobots)

- 5.2.6 Parallel robots

- 5.2.7 Others

- 5.3 Service robots

- 5.3.1 Personal service robots

- 5.3.2 Professional service robots

Chapter 6 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Hardware

- 6.2.1 Mechanical component

- 6.2.1.1 Actuation & drive components

- 6.2.1.2 Joint & bearing systems

- 6.2.1.3 Springs & elastic components

- 6.2.1.4 Fastening & connection components

- 6.2.1.5 End effectors & tooling

- 6.2.1.6 Others

- 6.2.2 Electronic components

- 6.2.2.1 Motors and actuators

- 6.2.2.2 Sensors

- 6.2.2.3 Controllers and processors

- 6.2.2.4 Power supplies and batteries

- 6.2.2.5 Others

- 6.2.1 Mechanical component

- 6.3 Software

- 6.4 Services

- 6.4.1 Engineering and installation

- 6.4.2 Maintenance and Support

- 6.4.3 Training and education

Chapter 7 Market Estimates and Forecast, By Mobility, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Fixed robotics

- 7.3 Mobile robotics

- 7.4 Humanoid robotics

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Assembly & production

- 8.3 Inspection & quality control

- 8.4 Material handling

- 8.5 Welding & soldering

- 8.6 Packaging & palletizing

- 8.7 Medical assistance

- 8.8 Security & surveillance

- 8.9 Retail & customer interaction robots

- 8.10 Education

- 8.11 Others

Chapter 9 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Manufacturing & industrial

- 9.2.1 Automotive

- 9.2.2 Electronics & semiconductor

- 9.2.3 Food & beverage

- 9.2.4 Pharmaceuticals

- 9.2.5 Metal & machinery

- 9.2.6 Others

- 9.3 Healthcare

- 9.4 Defense

- 9.5 Agriculture

- 9.6 Household

- 9.7 Retail & e-commerce

- 9.8 Hospitality

- 9.9 Logistics

- 9.10 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.3.7 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Rest of MEA

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 ABB Ltd.

- 11.1.2 Fanuc Corporation

- 11.1.3 KUKA AG

- 11.1.4 Yaskawa Electric Corporation

- 11.1.5 Mitsubishi Electric Corporation

- 11.1.6 Omron Corporation

- 11.1.7 Intuitive Surgical

- 11.1.8 Medtronic

- 11.2 Regional key players

- 11.2.1 Clearpath Robotics

- 11.2.2 MiR (Mobile Industrial Robots)

- 11.2.3 Staubli Group

- 11.2.4 Universal Robots

- 11.2.5 Aethon

- 11.3 Niche Players/Disruptors

- 11.3.1 Boston Dynamics

- 11.3.2 Blue Ocean Robotics

- 11.3.3 Ecovacs Robotics

- 11.3.4 iRobot Corporation

- 11.3.5 Knightscope, Inc.

- 11.3.6 Segway Robotics

- 11.3.7 SoftBank Robotics

人機協作市場預測至2034年:按組件、機器人類型、應用、最終用戶和地區分類的全球分析

人機協作市場預測至2034年:按組件、機器人類型、應用、最終用戶和地區分類的全球分析 機器人驅動裝置市場:按驅動系統、機器人類型、軸配置和應用分類-2026-2032年全球市場預測

機器人驅動裝置市場:按驅動系統、機器人類型、軸配置和應用分類-2026-2032年全球市場預測 室內機器人市場報告:按類型、最終用戶和地區分類(2026-2034 年)互動式機器人市場:按組件、自主性、移動功能和應用分類-2026-2032年全球市場預測翻新機器人市場:按機器人類別、機器人類型、翻新等級、成色等級、移動類型、應用、最終用戶產業和通路分類-2026-2032年全球預測

室內機器人市場報告:按類型、最終用戶和地區分類(2026-2034 年)互動式機器人市場:按組件、自主性、移動功能和應用分類-2026-2032年全球市場預測翻新機器人市場:按機器人類別、機器人類型、翻新等級、成色等級、移動類型、應用、最終用戶產業和通路分類-2026-2032年全球預測 室內機器人市場規模、佔有率和成長分析(按產品類型、機器人類型、硬體組件、應用、最終用戶、運作環境和地區分類)—2026-2033年產業預測

室內機器人市場規模、佔有率和成長分析(按產品類型、機器人類型、硬體組件、應用、最終用戶、運作環境和地區分類)—2026-2033年產業預測 機器人市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、形式、最終用戶及功能分類視覺引導機器人市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、功能、安裝類型及部署形式分類

機器人市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、形式、最終用戶及功能分類視覺引導機器人市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、功能、安裝類型及部署形式分類 全球鑄造鍛造機器人市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球鑄造鍛造機器人市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年主要機器人全球市場報告

2026年主要機器人全球市場報告