|

市場調查報告書

商品編碼

2027581

防護包裝市場機會、成長要素、產業趨勢分析及2026-2035年預測Protective Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

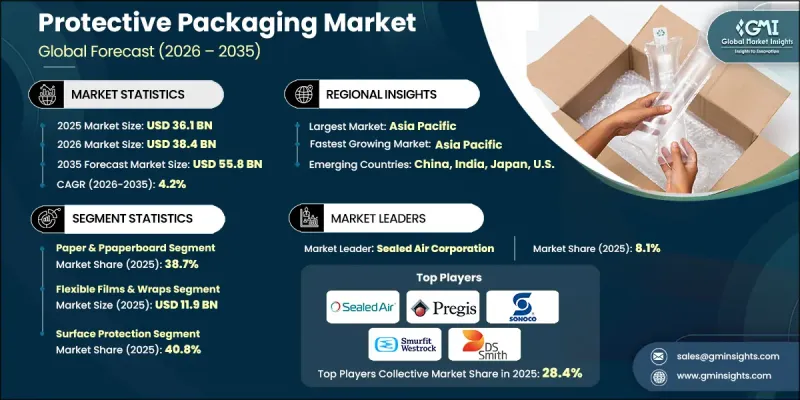

全球防護包裝市場預計到 2025 年價值 361 億美元,預計到 2035 年將以 4.2% 的複合年成長率成長至 558 億美元。

市場擴張主要得益於電子商務的快速發展和全球最後一公里配送業務的激增,這反過來又增加了對運輸途中產品可靠保護的需求。全球電子貿易的持續成長也強化了對能夠保護貴重易碎品的先進包裝解決方案的需求。此外,日益嚴格的物流績效標準(旨在減少破損)迫使企業採用更有效率的包裝系統。向可回收和環保材料的轉變正在進一步改變行業實踐。同時,自動化和智慧包裝技術正在物流和運輸網路中廣泛應用,以提高效率、追蹤能力和處理準確性。所有這些因素共同凸顯了保護性包裝作為現代全球供應鏈關鍵組成部分的重要性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 361億美元 |

| 預計金額 | 558億美元 |

| 複合年成長率 | 4.2% |

受電子商務平台快速成長和末端配送小包裹量激增的強勁推動,防護包裝市場正在擴張。線上零售的成長顯著提升了對安全包裝的需求,這種包裝能夠最大限度地減少運輸途中的損壞,降低退貨率,並提高客戶滿意度。跨境運輸的成長,尤其是在電子產品領域,進一步推動了對耐用防護解決方案的需求。此外,主要經濟體對永續和可回收替代包裝的日益重視,以及對自動化倉儲和履約系統投資的增加,也為市場成長提供了支撐。

預計2026年至2035年間,發泡聚合物市場將以5.3%的複合年成長率成長。由於其輕質、高抗衝擊性和高度可自訂性,發泡聚合物材料被廣泛應用於電子產品、藥品和精密消費品等易碎產品的包裝。其卓越的緩衝性能和對複雜產品形狀的適應性,使其成為製造商在包裝設計中兼顧可靠保護和營運效率的首選。

預計到2025年,表面保護產品將佔據40.8%的市場。該產品廣泛應用於電子產品、汽車零件和家具的物流領域,用於防止產品在儲存和運輸過程中出現刮痕、磨損和污染等表面損傷。需求的成長主要源自於在整個供應鏈(尤其是以零售為中心的配送網路)中維持產品外觀和功能的重要性。此外,對永續性重視也推動了可回收保護膜的應用,進一步促進了該領域在全球物流運營中的成長。

預計到2025年,美國防護包裝市場規模將達52億美元。美國市場的成長與政府主導的基礎設施現代化和經濟發展措施密切相關。美國環保署(EPA)和各州環保機構等監管機構正積極推廣循環經濟模式和包裝廢棄物減量計劃,從而促進永續材料的採用。加之電子商務的快速發展和物流的持續現代化,這些因素共同推動了對先進包裝和耐用防護包裝解決方案的強勁需求,使美國成為北美領先的區域市場。

全球防護包裝市場的主要參與者包括 Pregis LLC、Sealed Air Corporation、Smurfit WestRock、Berry Global Inc.、Mondi Group、Sonoco Products Company、Cascades Inc.、Huhtamaki Oyj、International Paper Company、Ranpak Holdings Corp.、ProAmpac Holdings Inc.、DS Smith Plc、International Paper Company、Ranpak Holdings Corp。防護包裝市場企業的主要策略著重於透過開發可回收和可生物分解材料來加強永續性發展,同時增加對先進緩衝技術的投資。市場參與企業正積極提升包裝營運的自動化能力,以提高效率並降低營運成本。策略性併購正在進行中,旨在擴大地域覆蓋範圍和產品系列。各公司還在研發方面投入巨資,以開發適用於電子商務和電子產品的輕質高性能防護材料。與物流和零售公司的合作也在不斷加強,以改善供應鏈整合並提供客製化的包裝解決方案。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 電子商務的成長增加了對最後一公里產品保護的需求。

- 對防靜電緩衝解決方案的需求增加,電子設備出貨量也隨之成長。

- 全球物流營運中嚴格的損耗降低關鍵績效指標

- 倉庫自動化需要標準化的保護方法

- 跨境貿易的擴張增加了運輸風險。

- 產業潛在風險與挑戰

- 聚合物和紙漿原料價格波動

- 永續發展法規限制一次性塑膠包裝的使用。

- 市場機遇

- 採用可生物分解發泡材和模塑纖維解決方案

- 整合智慧包裝以實現衝擊和溫度監測

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要公司的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與發展(R&D)

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興/新創競爭對手的發展趨勢

第5章 市場估算與預測:依材料類型分類,2022-2035年

- 紙張和紙板

- 塑膠

- 發泡聚合物

- 其他材料

第6章 市場估算與預測:依產品類型分類,2022-2035年

- 軟性薄膜包裝

- 保護性郵件包裝袋和信封

- 緩衝材料/縫隙填充材

- 預先設計的保護方案

- 剛性容器和結構包裝

第7章 市場估計與預測:依功能分類,2022-2035年

- 緩衝和減震

- 間隙填充和穩定

- 表面保護

- 屏障和環境保護

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 電子商務、零售與消費品

- 電子電器設備

- 車

- 醫療和藥品

- 食品/飲料

- 工業和製造業

- 物流和第三方物流供應商

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 全球主要公司

- Sealed Air Corporation

- DS Smith Plc

- International Paper Company

- Mondi Group

- Berry Global Inc.

- 按地區分類的主要公司

- 北美洲

- Pregis LLC

- Sonoco Products Company

- Intertape Polymer Group Inc.

- ProAmpac Holdings Inc.

- 亞太地區

- Huhtamaki Oyj

- Ranpak Holdings Corp.

- 歐洲

- Smurfit WestRock

- Storopack Hans Reichenecker GmbH

- Nefab Group

- 北美洲

- 特殊玩家/干擾者

- Cascades Inc.

The Global Protective Packaging Market was valued at USD 36.1 billion in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 55.8 billion by 2035.

Market expansion is driven by the rapid rise of e-commerce activity and the surge in last-mile delivery operations worldwide, which are increasing the need for reliable product protection during transit. The continuous growth in global electronics trade is also strengthening demand for advanced protective packaging solutions that can safeguard high-value and fragile goods. In addition, stricter logistics performance benchmarks focused on damage reduction are pushing companies to adopt more efficient packaging systems. The increasing shift toward recyclable and eco-friendly materials is further reshaping industry practices, while automation and smart packaging technologies are gaining traction across logistics and shipping networks to improve efficiency, tracking, and handling precision. Collectively, these factors are reinforcing the importance of protective packaging as a critical component of modern global supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $36.1 Billion |

| Forecast Value | $55.8 Billion |

| CAGR | 4.2% |

The expansion of the protective packaging market is strongly supported by the rapid acceleration of e-commerce platforms and rising parcel volumes associated with last-mile deliveries. The growth of online retail has significantly increased the need for secure packaging formats that minimize transit damage, reduce return rates, and improve customer satisfaction. Rising cross-border shipments, particularly in electronics, are further intensifying the demand for durable protective solutions. Market growth is additionally supported by increased investments in automated warehousing and fulfillment systems, alongside rising awareness regarding sustainable and recyclable packaging alternatives across major economies.

The foam polymers segment is projected to register a CAGR of 5.3% during 2026-2035 Foam polymer materials are widely utilized for packaging sensitive goods such as electronics, pharmaceuticals, and precision consumer products due to their lightweight structure, high impact resistance, and customization flexibility. Their superior cushioning performance and adaptability to complex product geometries make them a preferred choice among manufacturers seeking reliable protection combined with operational efficiency in packaging design.

The surface protection segment held a share of 40.8% in 2025. This segment is extensively used across electronics, automotive components, and furniture logistics to prevent surface damage such as scratches, abrasion, and contamination during storage and transportation. Strong demand is driven by the need to preserve product appearance and functionality throughout the supply chain, particularly in retail-focused distribution networks. Additionally, increasing sustainability requirements are encouraging the adoption of recyclable protective films, further supporting segment growth across global logistics operations.

U.S. Protective Packaging Market captured USD 5.2 billion in 2025. Market growth in the United States is closely tied to government-led initiatives supporting infrastructure modernization and economic development. Regulatory bodies such as the EPA, along with state-level environmental agencies, are actively promoting circular economy models and packaging waste reduction programs, encouraging the adoption of sustainable materials. Combined with the rapid growth of e-commerce and ongoing logistics modernization, these factors are driving strong demand for advanced, durable, and environmentally compliant protective packaging solutions, positioning the U.S. as a key regional leader in North America.

The major companies operating in the Global Protective Packaging Market include Pregis LLC, Sealed Air Corporation, Smurfit WestRock, Berry Global Inc., Mondi Group, Sonoco Products Company, Cascades Inc., Huhtamaki Oyj, International Paper Company, Ranpak Holdings Corp., ProAmpac Holdings Inc., DS Smith Plc, Intertape Polymer Group Inc., Nefab Group, and Storopack Hans Reichenecker GmbH. Key strategies adopted by companies in the Protective Packaging Market focus on strengthening sustainability initiatives through recyclable and biodegradable material development while expanding investments in advanced cushioning technologies. Market players are actively enhancing automation capabilities in packaging operations to improve efficiency and reduce operational costs. Strategic mergers and acquisitions are being pursued to expand geographic presence and product portfolios. Companies are also investing heavily in research and development to create lightweight, high-performance protective materials tailored for e-commerce and electronics applications. Partnerships with logistics and retail firms are increasing to improve supply chain integration and customized packaging solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Product format trends

- 2.2.3 Function trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 E-commerce growth increasing last-mile product protection demand

- 3.2.1.2 Rising electronics shipments requiring anti-static cushioning solutions

- 3.2.1.3 Strict damage-reduction KPIs in global logistics operations

- 3.2.1.4 Automation in warehouses demanding standardized protective formats

- 3.2.1.5 Growth in cross-border trade increasing transit risk exposure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in polymer and pulp raw material prices

- 3.2.2.2 Sustainability regulations restricting single-use plastic packaging formats

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of biodegradable foam and molded fiber solutions

- 3.2.3.2 Integration of smart packaging for shock and temperature monitoring

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Paper & paperboard

- 5.3 Plastic-based

- 5.4 Foam polymers

- 5.5 Other materials

Chapter 6 Market Estimates and Forecast, By Product Format, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Flexible films & wraps

- 6.3 Protective mailers & envelopes

- 6.4 Loose fill & void fill

- 6.5 Engineered protective solutions

- 6.6 Rigid containers & structural packaging

Chapter 7 Market Estimates and Forecast, By Function, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Cushioning & shock absorption

- 7.3 Void fill & stabilization

- 7.4 Surface protection

- 7.5 Barrier & environmental protection

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 E-commerce, retail & consumer goods

- 8.3 Electronics & electrical

- 8.4 Automotive

- 8.5 Healthcare & pharmaceuticals

- 8.6 Food & beverage

- 8.7 Industrial & manufacturing

- 8.8 Logistics & 3pl providers

- 8.9 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Sealed Air Corporation

- 10.1.2 DS Smith Plc

- 10.1.3 International Paper Company

- 10.1.4 Mondi Group

- 10.1.5 Berry Global Inc.

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Pregis LLC

- 10.2.1.2 Sonoco Products Company

- 10.2.1.3 Intertape Polymer Group Inc.

- 10.2.1.4 ProAmpac Holdings Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 Huhtamaki Oyj

- 10.2.2.2 Ranpak Holdings Corp.

- 10.2.3 Europe

- 10.2.3.1 Smurfit WestRock

- 10.2.3.2 Storopack Hans Reichenecker GmbH

- 10.2.3.3 Nefab Group

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Cascades Inc.

2034年防護包裝市場預測-按產品類型、材料類型、功能、分銷管道、最終用戶和地區分類的全球分析

2034年防護包裝市場預測-按產品類型、材料類型、功能、分銷管道、最終用戶和地區分類的全球分析 防護包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

防護包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 防護包裝市場:2026-2032年全球市場預測(按產品類型、應用、分銷管道和最終用戶分類)

防護包裝市場:2026-2032年全球市場預測(按產品類型、應用、分銷管道和最終用戶分類) 長笛玻璃市場規模、佔有率和趨勢分析報告:按應用、最終用途、地區和細分市場分類(2026-2033 年)

長笛玻璃市場規模、佔有率和趨勢分析報告:按應用、最終用途、地區和細分市場分類(2026-2033 年) 生物分解緩衝材料(花生)市場分析及預測(至2035年):按類型、產品類型、材質、應用、技術、最終用戶、功能、製程、安裝類型及解決方案分類

生物分解緩衝材料(花生)市場分析及預測(至2035年):按類型、產品類型、材質、應用、技術、最終用戶、功能、製程、安裝類型及解決方案分類 全球防護包裝市場:市場規模、佔有率、成長和行業分析:按類型、最終用途行業和區域預測(2024-2034 年)

全球防護包裝市場:市場規模、佔有率、成長和行業分析:按類型、最終用途行業和區域預測(2024-2034 年) 2026年全球防護包裝市場報告

2026年全球防護包裝市場報告 2026-2030年全球防護包裝市場高性能防護發泡包裝市場(按材料類型、產品類型、通路、應用和最終用戶產業分類)-2026-2032年全球預測

2026-2030年全球防護包裝市場高性能防護發泡包裝市場(按材料類型、產品類型、通路、應用和最終用戶產業分類)-2026-2032年全球預測 防護包裝市場規模、佔有率和成長分析(按類型、材料、功能、最終用途和地區分類)—產業預測(2026-2033 年)

防護包裝市場規模、佔有率和成長分析(按類型、材料、功能、最終用途和地區分類)—產業預測(2026-2033 年)