|

市場調查報告書

商品編碼

2027563

2026 年至 2035 年生鮮食品包裝的市場機會、成長要素、產業趨勢與預測。Fresh Food Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

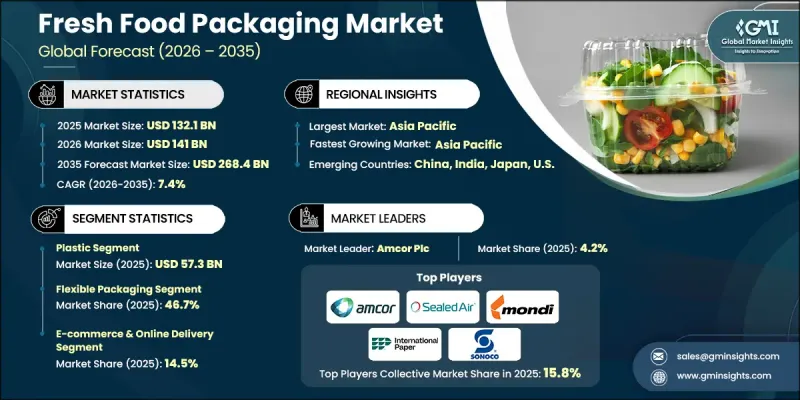

預計到 2025 年,全球生鮮食品包裝市場價值將達到 1,321 億美元,年複合成長率為 7.4%,到 2035 年將達到 2,684 億美元。

市場成長深受消費者生活方式變化的影響,尤其是在時間效率和便利性至關重要的都市區。這種轉變推動了對即食、易攜帶的生鮮食品的需求成長,這些食品能夠融入人們忙碌的日常生活節奏,包括工作、旅行和社交活動。因此,包裝不再只是為了保護產品;它在提升便利性、便攜性和易用性方面發揮著越來越重要的作用。食品製造商正在透過採用先進的包裝解決方案來應對這一變化,這些解決方案有助於延長保存期限、簡化操作並改善產品外觀。包裝設計的持續創新正在進一步重塑行業標準,企業正致力於開發兼具功能性和永續性的包裝形式。同時,消費者對新鮮度、衛生和食品安全的日益重視也加速了先進包裝技術的應用。對永續材料和高效供應鏈系統的加大投入也為全球市場的擴張提供了支持。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 1321億美元 |

| 預測金額 | 2684億美元 |

| 複合年成長率 | 7.4% |

預計到2025年,軟包裝市佔率將達到46.7%。該細分市場憑藉其輕盈的結構、成本效益以及在包裝應用中減少材料用量等優勢,持續保持主導地位。軟包裝廣泛應用於生鮮食品已調理食品的包裝,能夠提供有效的保護、延長保存期限並降低運輸成本。人們對永續性的日益關注,進一步推動了可回收單一材料結構和先進複合材料的應用,從而強化了軟包裝在整個食品供應鏈中的作用。

預計到2025年,電子商務和線上配送領域將佔據14.5%的市場。數位生鮮購物和食品配送服務的快速發展正顯著影響著包裝需求。為了在長途且複雜的通路中維持產品質量,市場對防護性強、耐用且防潮的包裝解決方案的需求日益成長。隨著線上食品零售的持續發展,能夠確保產品在運輸過程中保持新鮮、安全和便利的包裝解決方案的重要性也日益凸顯。

到2025年,北美生鮮食品包裝市佔率將達到31.1%。該地區擁有強大的創新能力、先進的供應鏈體系和完善的低溫運輸基礎設施。新鮮農產品、肉品和已調理食品的高消費量支撐了對先進包裝解決方案的穩定需求。此外,消費者對新鮮、加工較少的食品日益成長的偏好,推動了能夠延長保存期限並同時保持品質和安全標準的包裝系統的應用。持續的技術創新和永續發展措施進一步促進了該地區的市場成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 消費者對食品安全和品質的需求日益成長。

- 嚴格的監管標準

- 消費者越來越偏好便利的出行消費方式。

- 環保包裝解決方案的創新

- 重視高效率的供應鏈管理

- 產業潛在風險與挑戰

- 擴大永續包裝解決方案面臨的挑戰

- 引進新型包裝技術所帶來的成本影響

- 市場機遇

- 智慧包裝技術的發展

- 擴大植物來源材料和替代材料的使用

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要公司的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與發展(R&D)

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興競爭對手和新創競爭對手的發展趨勢

第5章 市場估算與預測:依材料類型分類,2022-2035年

- 塑膠

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚苯乙烯(PS)

- 聚氯乙烯(PVC)

- 其他

- 紙張和紙板

- 紙板

- 折疊式紙箱

- 紙袋

- 其他

- 金屬

- 鋁

- 鋼罐

- 其他

- 其他

第6章 市場估價與預測:依包裝類型分類,2022-2035年

- 硬包裝

- 托盤

- 翻蓋式容器

- 盒子/紙箱

- 瓶子罐

- 能

- 其他

- 軟包裝

- 薄膜包裝

- 袋子和小袋

- 袖子

- 其他

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 水果和蔬菜

- 肉類/雞肉

- 新鮮紅肉

- 新鮮家禽

- 加工肉品

- 其他

- 魚貝類

- 乳製品

- 生牛奶和奶油

- 優格和發酵乳

- 起司

- 其他

- 麵包和糖果甜點

- 麵包捲

- 蛋糕和酥皮點心

- 生餅乾和巧克力

- 其他

- 即食食品(RTE)

- 沙拉和水果拼盤

- 三明治捲

- 新鮮食材自煮包/調理食品

- 其他

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 零售

- 超級市場和大賣場

- 便利商店

- 特色食品店

- 食品服務業

- 全方位服務的餐廳

- 速食店(QSR)

- 其他

- 電子商務和線上配送

- 對機構而言

- 醫院和醫療保健

- 學校和大學

- 軍隊

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- 全球主要公司

- Amcor Plc

- Crown Holdings Inc.

- DS Smith Plc

- Huhtamaki Oyj

- International Paper Company

- Mondi PLC

- Sealed Air Corporation

- Sonoco Products Company

- Tetra Pak International

- WestRock Company

- 按地區分類的主要公司

- Anchor Packaging Inc.

- Coveris Holdings SA

- Flair Flexible Packaging Corporation

- Genpak, LLC

- Graphic Packaging International(Holding Co.)

- 特殊玩家/干擾者

- PPC Flexible Packaging LLC

- ProAmpac LLC

- Reynolds Group Holdings Ltd.

- Winpak Ltd.

The Global Fresh Food Packaging Market was valued at USD 132.1 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 268.4 billion by 2035.

Market growth is strongly influenced by shifting consumer lifestyles, particularly in urban regions where time efficiency and convenience have become key priorities. This shift is driving higher demand for ready-to-eat and easy-to-carry fresh food products that fit into fast-paced daily routines involving work, travel, and social activities. As a result, packaging is no longer limited to product protection but is increasingly playing a crucial role in enhancing convenience, portability, and usability. Food manufacturers are adapting by adopting advanced packaging solutions that support longer shelf life, easier handling, and improved product presentation. Continuous innovation in packaging design is further reshaping industry standards, with companies focusing on functional and sustainable formats. At the same time, rising consumer awareness around freshness, hygiene, and food safety is accelerating the adoption of advanced packaging technologies. Increasing investments in sustainable materials and efficient supply chain systems are also supporting market expansion across global regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $132.1 Billion |

| Forecast Value | $268.4 Billion |

| CAGR | 7.4% |

The flexible packaging segment accounted for 46.7% share in 2025. This segment continues to lead due to its lightweight structure, cost efficiency, and reduced material usage in packaging applications. Flexible formats are widely used for fresh and prepared food products as they offer strong protection, extended shelf life, and lower transportation costs. Growing emphasis on sustainability is further encouraging the adoption of recyclable mono-material structures and advanced laminates, which are strengthening the role of flexible packaging across the food supply chain.

The e-commerce and online delivery segment held a 14.5% share in 2025. The rapid expansion of digital grocery shopping and food delivery services is significantly influencing packaging requirements. Increasing demand for protective, durable, and moisture-resistant packaging solutions is being driven by the need to maintain product integrity across extended and complex distribution channels. As online food retail continues to expand, packaging solutions that ensure freshness, safety, and convenience during transit are becoming increasingly important.

North America Fresh Food Packaging Market accounted for 31.1% share in 2025. The region is characterized by strong innovation capabilities, advanced supply chain systems, and a well-developed cold chain infrastructure. High consumption of fresh produce, meat products, and ready-to-eat meals is supporting steady demand for advanced packaging solutions. Increasing consumer preference for fresh and minimally processed foods is also encouraging the use of packaging systems that extend shelf life while maintaining quality and safety standards. Continuous technological advancements and sustainability initiatives are further strengthening market growth in the region.

Key companies operating in the Global Fresh Food Packaging Market include Amcor Plc, Anchor Packaging Inc., Coveris Holdings S.A., Crown Holdings Inc., DS Smith Plc, Flair Flexible Packaging Corporation, Genpak, LLC, Graphic Packaging International (Holding Co.), Huhtamaki Oyj, International Paper Company, Mondi PLC, PPC Flexible Packaging LLC, ProAmpac LLC, Reynolds Group Holdings Ltd., Sealed Air Corporation, Sonoco Products Company, Tetra Pak International, WestRock Company, and Winpak Ltd. Companies in the Fresh Food Packaging Market are strengthening their market position through innovation in sustainable materials, product design advancements, and expansion of production capabilities. They are increasingly focusing on developing eco-friendly and recyclable packaging solutions to meet regulatory requirements and rising environmental concerns. Investments in smart packaging technologies that enhance shelf life monitoring and product traceability are also gaining traction. Many players are expanding partnerships with food manufacturers and retailers to develop customized packaging formats tailored to specific product needs. Optimization of supply chains and adoption of lightweight, cost-efficient materials are further supporting operational efficiency.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Packaging format trends

- 2.2.3 Application trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for food safety and quality

- 3.2.1.2 Stringent regulatory standards

- 3.2.1.3 Rising consumer preference for convenience and on-the-go consumption

- 3.2.1.4 Innovations in eco-friendly packaging solutions

- 3.2.1.5 Emphasis on efficient supply chain management

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Challenges in scaling sustainable packaging solutions

- 3.2.2.2 Cost implications of implementing new packaging technologies

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of smart and intelligent packaging technologies

- 3.2.3.2 Increasing adoption of plant-based and alternative materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Plastic

- 5.2.1 Polyethylene (PE)

- 5.2.2 Polypropylene (PP)

- 5.2.3 Polyethylene terephthalate (PET)

- 5.2.4 Polystyrene (PS)

- 5.2.5 Polyvinyl chloride (PVC)

- 5.2.6 Others

- 5.3 Paper & paperboard

- 5.3.1 Corrugated board

- 5.3.2 Folding carton

- 5.3.3 Paper bags

- 5.3.4 Others

- 5.4 Metal

- 5.4.1 Aluminum

- 5.4.2 Steel cans

- 5.4.3 Others

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Packaging Format, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Rigid packaging

- 6.2.1 Trays & plates

- 6.2.2 Clamshells & containers

- 6.2.3 Boxes & cartons

- 6.2.4 Bottles & jars

- 6.2.5 Cans

- 6.2.6 Others

- 6.3 Flexible packaging

- 6.3.1 Films & wraps

- 6.3.2 Bags & pouches

- 6.3.3 Sleeves

- 6.3.4 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Fruits & vegetables

- 7.3 Meat & poultry

- 7.3.1 Fresh red meat

- 7.3.2 Fresh poultry

- 7.3.3 Processed meat

- 7.3.4 Others

- 7.4 Seafood

- 7.5 Dairy products

- 7.5.1 Fluid milk & cream

- 7.5.2 Yogurt & fermented milk

- 7.5.3 Cheese

- 7.5.4 Others

- 7.6 Bakery & confectionery

- 7.6.1 Breads & rolls

- 7.6.2 Cakes & pastries

- 7.6.3 Fresh cookies/chocolates

- 7.6.4 Others

- 7.7 Ready-to-eat (RTE) foods

- 7.7.1 Salads & fruit bowls

- 7.7.2 Sandwiches & wraps

- 7.7.3 Fresh meal kits/ready meals

- 7.7.4 Others

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Retail

- 8.2.1 Supermarkets & hypermarkets

- 8.2.2 Convenience stores

- 8.2.3 Specialty food stores

- 8.3 Food service

- 8.3.1 Full-service restaurants

- 8.3.2 Quick service restaurants (QSR)

- 8.3.3 Others

- 8.4 E-commerce & online delivery

- 8.5 Institutional

- 8.5.1 Hospitals & healthcare

- 8.5.2 Schools & universities

- 8.5.3 Military

- 8.5.4 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Amcor Plc

- 10.1.2 Crown Holdings Inc.

- 10.1.3 DS Smith Plc

- 10.1.4 Huhtamaki Oyj

- 10.1.5 International Paper Company

- 10.1.6 Mondi PLC

- 10.1.7 Sealed Air Corporation

- 10.1.8 Sonoco Products Company

- 10.1.9 Tetra Pak International

- 10.1.10 WestRock Company

- 10.2 Regional key players

- 10.2.1 Anchor Packaging Inc.

- 10.2.2 Coveris Holdings S.A.

- 10.2.3 Flair Flexible Packaging Corporation

- 10.2.4 Genpak, LLC

- 10.2.5 Graphic Packaging International (Holding Co.)

- 10.3 Niche Players/Disruptors

- 10.3.1 PPC Flexible Packaging LLC

- 10.3.2 ProAmpac LLC

- 10.3.3 Reynolds Group Holdings Ltd.

- 10.3.4 Winpak Ltd.

2034年生鮮食品包裝市場預測-全球包裝類型、材料、產品類型、包裝技術、通路與區域分析

2034年生鮮食品包裝市場預測-全球包裝類型、材料、產品類型、包裝技術、通路與區域分析 生鮮食品包裝市場:依材料、包裝形式、應用及地區分類蘑菇包裝市場預測至2034年—按類型、材料成分、分銷管道、應用、最終用戶和地區分類的全球分析

生鮮食品包裝市場:依材料、包裝形式、應用及地區分類蘑菇包裝市場預測至2034年—按類型、材料成分、分銷管道、應用、最終用戶和地區分類的全球分析 菌絲包裝材料市場規模、佔有率和成長分析:按材料、包裝類型、分銷管道、最終用途行業、地區和行業預測,2026-2033年

菌絲包裝材料市場規模、佔有率和成長分析:按材料、包裝類型、分銷管道、最終用途行業、地區和行業預測,2026-2033年 全球生鮮食品包裝市場:市場規模、佔有率、成長和行業分析:按材料類型、產品類型、包裝類型、應用和區域預測(至2034年)

全球生鮮食品包裝市場:市場規模、佔有率、成長和行業分析:按材料類型、產品類型、包裝類型、應用和區域預測(至2034年) Panette包裝全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球生鮮食品包裝市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球蘑菇包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球保鮮包裝市場預測至2032年:按材料、包裝類型、分銷管道、技術、應用和地區分類的分析

Panette包裝全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球生鮮食品包裝市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球蘑菇包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球保鮮包裝市場預測至2032年:按材料、包裝類型、分銷管道、技術、應用和地區分類的分析 食品包裝盒市場規模、佔有率和成長分析(按產品類型、產能、材質、應用和地區分類)-2026-2033年產業預測

食品包裝盒市場規模、佔有率和成長分析(按產品類型、產能、材質、應用和地區分類)-2026-2033年產業預測