|

市場調查報告書

商品編碼

2027552

機械錶市場商機、成長要素、產業趨勢分析及2026-2035年預測。Mechanical Watch Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

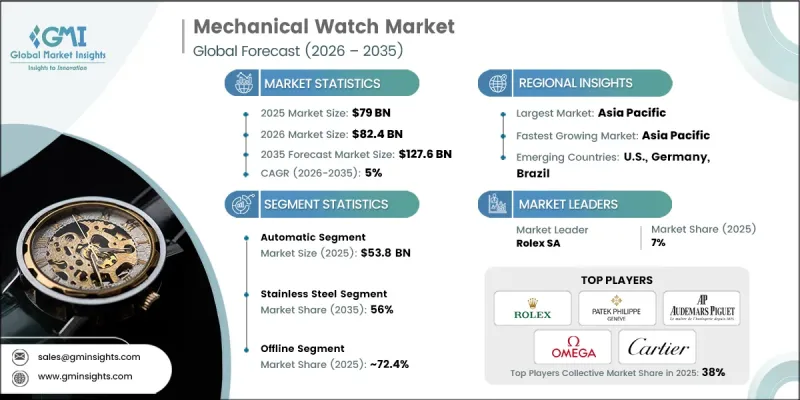

預計到 2025 年,全球機械手錶市場價值將達到 790 億美元,並有望以 5% 的複合年成長率成長,到 2035 年達到 1,276 億美元。

由於人們對傳統製錶工藝的欣賞日益增強,以及全球富裕人群對奢華腕錶的需求不斷成長,市場正在蓬勃發展。領先品牌間的策略性併購與合作,不斷拓展其經典系列,提升產能,並鞏固其在全球市場的地位。產業重組推動了機芯技術的進步,使得融合傳統技藝與創新功能的高精準度機械腕錶得以問世。這些發展在奢侈品零售和時尚市場尤其受到青睞,因為稀缺性、卓越的設計和精湛的工藝是影響消費者偏好的關鍵因素。總而言之,市場成長的驅動力在於消費者對兼具尊貴氣質、技術先進、彰顯個性風格並具有長期投資價值的腕錶的需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 790億美元 |

| 預測金額 | 1276億美元 |

| 複合年成長率 | 5% |

傳統機械腕錶正日益融入萬年曆、陀飛輪和計時碼錶等先進複雜功能,進而提升精準度與性能。這些先進時計憑藉其精湛的工藝、稀有性和收藏價值,推動著市場擴張。高性能腕錶的目標客戶是那些重視技術卓越、美學設計和耐用性的消費者。創新複雜功能的融入是關鍵的差異化因素,不僅提升了品牌地位,也促進了全球奢侈品市場對高階機械腕錶的需求。

預計到2035年,自動上鍊腕錶市場規模將達到885億美元,而2025年的市場規模為538億美元。自動上鍊腕錶利用手腕的自然擺動自動上鍊,無需手動上鍊,方便快捷,深受追求低維護成本的奢華腕錶消費者的青睞。先進的轉子驅動上鍊系統能夠提供穩定的動力,確保精準的時間和日期顯示等複雜機械裝置的可靠運作。現代自動上鍊腕錶採用雙向轉子和精密滾珠軸承系統,提高了效率、穩定性和耐用性,使其成為日常佩戴和積極生活方式的理想選擇。這些創新凸顯了該細分市場在技術進步和消費者接受度方面的重要性。

預計到2025年,線下通路市佔率將達到72.4%,到2035年將維持在72.8%。個人化體驗,例如授權精品店和零售商提供的體驗,讓顧客親身觸摸和感受產品,在奢侈品購買中仍然至關重要。顧客重視能夠仔細檢查工藝、試戴腕錶,並獲得真偽鑑定、保固和售後服務。隨著消費者行為的改變,品牌正擴大採用全通路策略,將線上產品探索與線下購買體驗結合。預約諮詢、虛擬預覽和混合零售模式正變得越來越普遍,這些模式有助於品牌在滿足消費者不斷變化的奢侈腕錶購買期望的同時,保持客戶參與度。

預計到2025年,美國機械錶市場佔有率將達到78%,這主要得益於消費者較高的可支配收入、活躍的收藏家群體以及主要都市區遍布的授權經銷商網路。此外,古董錶收藏的日益普及、奢侈品電商平台的擴張以及對體驗式零售(例如品牌傳承中心和互動展示廳)的投資,也推動了市場成長。該地區的消費者越來越追求兼具奢華、性能和收藏價值的高品質自動上鍊和手動上鍊腕錶,這持續支撐著新系列和經典系列的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 財富成長與奢侈品消費

- 傳統價值與工匠技藝

- 投資價值與資產保值

- 產業潛在風險與挑戰

- 透過智慧型手錶和穿戴式技術展開競爭

- 技術純熟勞工短缺和生產受限

- 機會

- 認證二手和二次性市場的擴張

- 客製化和個人化服務

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按類型分類的趨勢

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 交易數據分析(基於初步調查)

- 進出口數量和價值趨勢(基於第一次調查)(2022-2025 年)

- 主要貿易走廊及關稅影響(基於初步調查)

- 波特的分析

- PESTEL 分析

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧變革傳統零售模式

- 生成式人工智慧的應用案例(虛擬試穿、個人化、身份驗證)

- 分銷基礎設施和通路滲透狀況(基於初步調查)

- 按地區和形式(單品牌與多品牌)分類的通路覆蓋率(基於初步調查)

- 電子商務基礎設施和全通路整合面臨的挑戰(基於初步研究)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依運輸方式分類,2022-2035年

- 自動的

- 手動的

第6章 市場估價與預測:依綁帶材料分類,2022-2035年

- 皮革

- 不銹鋼

- 尼龍

- 其他(橡膠等)

第7章 市場估計與預測:以箱量分類,2022-2035年

- 35毫米或更小

- 35 mm~40 mm

- 40 mm~45 mm

- 超過 45 毫米

第8章 市場估算與預測:依形狀分類,2022-2035年

- 長方形

- 圓

- 方塊

第9章 市場估計與預測:依消費群組分類,2022-2035年

- 男性

- 女士

- 男女通用的

第10章 市場估價與預測:依應用領域分類,2022-2035年

- 低的

- 中號

- 高階/優質

第11章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務網站

- 公司網站

- 離線

- 大型零售商店

- 專賣店

- 其他(例如,獨立經營的商店)

第12章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第13章:公司簡介

- A. Lange &Sohne GmbH

- Audemars Piguet Holding SA

- Blancpain SA

- Cartier International SNC

- Girard-Perregaux SA

- IWC International Watch Co. AG

- Jaeger-LeCoultre SA

- Montres Breguet SA

- Officine Panerai SA

- Omega SA

- Patek Philippe SA Geneve

- Rolex SA

- Seiko Group Corporation

- TAG Heuer SA

- Vacheron Constantin SA

The Global Mechanical Watch Market was valued at USD 79 billion in 2025 and is estimated to grow at a CAGR of 5% to reach USD 127.6 billion by 2035.

The rising appreciation for traditional watchmaking craftsmanship and the increasing demand for luxury timepieces among affluent consumers worldwide are driving market growth. Strategic mergers, acquisitions, and collaborations among leading brands are further expanding heritage collections, improving production capabilities, and strengthening global market presence. Consolidation in the sector has spurred technological advancements in movement engineering, enabling high-precision mechanical watches that combine traditional techniques with innovative features. These developments are particularly valued in luxury retail and fashion markets, where exclusivity, superior design, and craftsmanship determine consumer preference. Overall, the market's growth is fueled by the desire for prestigious, technically advanced timepieces that reflect personal style and long-term investment value.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $79 Billion |

| Forecast Value | $127.6 Billion |

| CAGR | 5% |

Traditional mechanical watches are increasingly being upgraded with sophisticated complications such as perpetual calendars, tourbillons, and chronographs, which enhance precision and performance. These advanced timepieces drive market expansion by offering exceptional craftsmanship, exclusivity, and collectible value. High-performance watches cater to consumers who prioritize technical excellence, aesthetics, and durability. The integration of innovative complications has become a key differentiator, elevating brand status while boosting demand for premium mechanical watches across global luxury markets.

The automatic segment accounted for USD 53.8 billion in 2025 and is projected to reach USD 88.5 billion by 2035. Automatic watches, which self-wind through natural wrist movement, offer convenience by eliminating the need for manual winding, making them highly desirable among consumers seeking low-maintenance luxury timepieces. Advanced rotor-driven winding systems maintain consistent power delivery, ensuring accurate timekeeping and reliable operation of complications such as date displays. Modern automatic watches incorporate bi-directional rotors and precision ball-bearing systems to improve efficiency, stability, and durability, making them ideal for daily wear and active lifestyles. These innovations underscore the segment's importance in technological advancement and consumer adoption within the market.

The offline channels segment held a 72.4% share in 2025 and is expected to hold 72.8% share by 2035. The tactile and personalized experience offered by authorized boutiques and retail stores remains critical for luxury purchases. Customers value the ability to examine craftsmanship, try on watches, and access authentication, warranty, and after-sales services. As consumer behavior evolves, brands are increasingly adopting omnichannel strategies, blending online discovery with offline purchase experiences. Appointment-based consultations, virtual previews, and hybrid retail initiatives are becoming common, helping brands maintain engagement while meeting evolving consumer expectations for luxury watch acquisition.

United States Mechanical Watch Market held a 78% share in 2025, driven by high disposable income, a robust collector community, and widespread authorized retail networks in major urban centers. Growth is further supported by the rising popularity of vintage watch collecting, the expansion of luxury e-commerce platforms, and investments in experiential retail, including brand heritage centers and interactive showcases. Consumers in the region increasingly seek high-quality automatic and manual-wind watches that combine luxury, performance, and collectibility, sustaining demand across both new and heritage timepiece collections.

Key players in the Global Mechanical Watch Market include Blancpain SA, TAG Heuer SA, IWC International Watch Co. AG, Rolex SA, Omega SA, Montres Breguet SA, Cartier International SNC, Audemars Piguet Holding SA, Patek Philippe SA Geneve, A. Lange & Sohne GmbH, Jaeger-LeCoultre SA, Vacheron Constantin SA, Seiko Group Corporation, Officine Panerai SA, and Girard-Perregaux SA. Companies in the Mechanical Watch Market strengthen their presence by investing in high-precision movement technology, including innovative complications and long-term durability improvements. Brands pursue strategic partnerships and acquisitions to expand their heritage collections and enhance manufacturing capabilities. Geographic expansion into emerging luxury markets and the development of omnichannel retail strategies increase market visibility and accessibility. Firms emphasize brand storytelling, heritage marketing, and experiential retail initiatives to foster consumer loyalty. Additionally, limited editions, bespoke designs, and collectible releases reinforce exclusivity and value perception.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research (Driven by Primary Research)

- 1.5.1 Industry Expert Interviews

- 1.5.2 Manufacturer & Brand Surveys

- 1.5.3 Retailer & Distributor Insights

- 1.6 Secondary Research

- 1.6.1 Paid Sources

- 1.6.2 Public Sources

- 1.7 Forecast model

- 1.8 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Movement Type

- 2.2.3 Strap Material

- 2.2.4 Case Size

- 2.2.5 Shape

- 2.2.6 Consumer Group

- 2.2.7 Price

- 2.2.8 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising affluence & luxury consumption

- 3.2.1.2 Heritage appreciation & artisan craftsmanship

- 3.2.1.3 Investment value & wealth preservation

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Competition from smartwatches & wearable technology

- 3.2.2.2 Skilled labor shortage & production constraints

- 3.2.3 Opportunities

- 3.2.3.1 Certified pre-owned & secondary market expansion

- 3.2.3.2 Customization & personalization services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Movement type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade Data Analysis (Driven by Primary Research)

- 3.8.1 Import/Export Volume & Value Trends (Driven by Primary Research) (2022-2025)

- 3.8.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Traditional Retail Models

- 3.11.2 GenAI Use Cases (Virtual Try-on, Personalization, Authentication)

- 3.12 Distribution Infrastructure & Channel Penetration Landscape (Driven by Primary Research)

- 3.12.1 Channel Coverage by Region & Format (Mono-brand vs. Multi-brand) (Driven by Primary Research)

- 3.12.2 E-commerce Infrastructure Gaps & Omnichannel Integration (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Movement Type, 2022 - 2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Automatic

- 5.3 Manual

Chapter 6 Market Estimates & Forecast, By Strap Material, 2022 - 2035(USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Leather

- 6.3 Stainless Steel

- 6.4 Nylon

- 6.5 Others (Rubber etc.)

Chapter 7 Market Estimates & Forecast, By Case Size, 2022 - 2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Up to 35 mm

- 7.3 35 mm - 40 mm

- 7.4 40 mm - 45 mm

- 7.5 Above 45 mm

Chapter 8 Market Estimates & Forecast, By Shape, 2022 - 2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Rectangular

- 8.3 Round

- 8.4 Square

Chapter 9 Market Estimates & Forecast, By Consumer Group, 2022 - 2035 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Men

- 9.3 Women

- 9.4 Unisex

Chapter 10 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Low

- 10.3 Medium

- 10.4 High/Premium

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 Online

- 11.2.1 E-commerce Websites

- 11.2.2 Company-owned Websites

- 11.3 Offline

- 11.3.1 Mega Retail Stores

- 11.3.2 Specialty Stores

- 11.3.3 Others (Independent Stores, etc.)

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Million Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 Japan

- 12.4.3 India

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 A. Lange & Sohne GmbH

- 13.2 Audemars Piguet Holding SA

- 13.3 Blancpain SA

- 13.4 Cartier International SNC

- 13.5 Girard-Perregaux SA

- 13.6 IWC International Watch Co. AG

- 13.7 Jaeger-LeCoultre SA

- 13.8 Montres Breguet SA

- 13.9 Officine Panerai SA

- 13.10 Omega SA

- 13.11 Patek Philippe SA Geneve

- 13.12 Rolex SA

- 13.13 Seiko Group Corporation

- 13.14 TAG Heuer SA

- 13.15 Vacheron Constantin SA