|

市場調查報告書

商品編碼

2027545

貓疫苗市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Cat Vaccines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

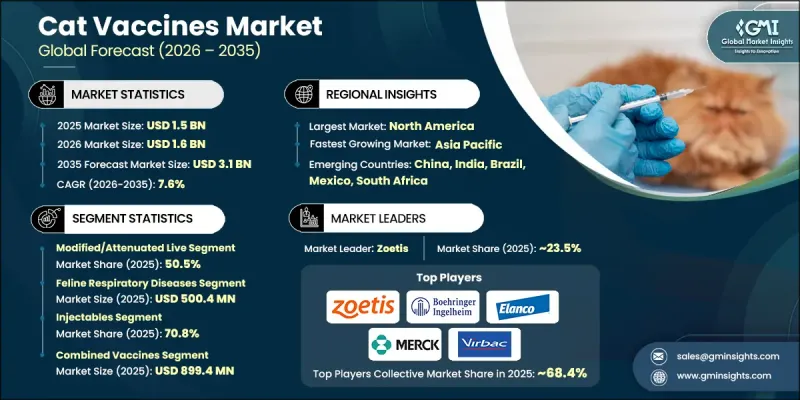

預計到 2025 年,全球貓疫苗市場價值將達到 15 億美元,並有望以 7.6% 的複合年成長率成長,到 2035 年達到 31 億美元。

市場成長的驅動力在於人們對動物健康的日益關注以及全球寵物主人數量的不斷成長。貓感染疾病率的上升推動了對醫療保健解決方案(尤其是疫苗接種)的需求。寵物飼主在保護寵物健康方面變得更加積極主動,加速了疫苗接種的普及。人們對人畜共通傳染病的日益關注進一步凸顯了免疫接種計劃的重要性。此外,寵物醫療保健服務和保險覆蓋範圍的擴大也提高了寵物獲得獸醫服務的便利性。這些因素共同推動了寵物健康支出的增加和疫苗接種率的提高。隨著預防醫學日益受到重視,市場正朝著長期疾病預防的方向發展,疫苗接種正成為現代寵物照護實踐中不可或缺的一部分。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 15億美元 |

| 預測金額 | 31億美元 |

| 複合年成長率 | 7.6% |

貓科動物疫苗是獸醫學的一個專門領域,旨在保護寵物免受各種感染疾病。這些疫苗的研發目的是增強免疫力,降低疾病感染的風險,進而維持動物的整體健康和福祉。

到2025年,改良活病毒疫苗和減毒活病毒疫苗將佔據50.5%的市場。該領域因其高效性、誘導強效免疫反應的能力以及成本效益而備受關注。這些疫苗因其能夠提供持久保護和快速激活免疫力而廣受歡迎,尤其適用於需要快速控制疾病的環境。其提供長期免疫力的能力也持續推動其廣泛應用。

預計到2025年,貓咪呼吸系統疾病市場規模將達到5.004億美元,主要得益於這些疾病的高發生率和高傳染性。這些疾病對貓的健康影響巨大,而且常常導致嚴重的併發症,因此,預防措施的重要性日益凸顯。對早期預防和疾病管理的重視正在推動該細分市場的需求成長,並鞏固其在整體市場的主導地位。

預計到2025年,北美貓疫苗市佔率將達到45.2%,並在預測期內以7.3%的複合年成長率成長。該地區的主導地位得益於較高的寵物擁有率、強大的寵物健康意識以及完善的獸醫基礎設施。寵物照護支出的增加和先進醫療服務的普及推動了市場的持續成長。主要行業相關人員的存在以及疫苗接種計劃的持續推廣進一步鞏固了該地區的市場地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 寵物數量增加以及寵物健康支出增加

- 人們對寵物預防保健的意識日益增強

- 疫苗技術的進步

- 人們對通用感染疾病的認知不斷提高

- 產業潛在風險與挑戰

- 疫苗研發成本高昂

- 嚴格的監管要求

- 市場機遇

- 獸醫保健基礎設施的成長和診所的擴張

- 與獸醫公共衛生相關的措施和項目增加

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 北美洲

- 科技與創新趨勢

- 目前技術

- 新興技術

- 產品平臺分析(基於初步調查)

- 專利分析(基於初步研究)

- 未來市場趨勢

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依疫苗類型分類,2022-2035年

- 減毒活病毒疫苗

- 失活

- 其他疫苗類型

第6章 市場估計與預測:依疾病類型分類,2022-2035年

- 貓的呼吸系統疾病

- 貓白血病

- 貓泛白血球減少症(貓瘟)

- 貓咪狂犬病

- 其他疾病類型

第7章 市場估計與預測:依給藥途徑分類,2022-2035年

- 注射藥物

- 鼻內

第8章 市場估算與預測:依組件分類,2022-2035年

- 聯合疫苗

- 單藥疫苗

第9章 市場估計與預測:依免疫接種期分類,2022-2035年

- 1年

- 3年

- 其他免疫期

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- Bioveta

- Boehringer Ingelheim

- Ceva Sante Animale

- Elanco Animal Health

- HIPRA

- Indian Immunologicals

- Merck

- Virbac

- Zoetis

The Global Cat Vaccines Market was valued at USD 1.5 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 3.1 billion by 2035.

Market growth is driven by rising awareness of animal health and the increasing global population of pet owners. The growing incidence of infectious conditions among cats is strengthening demand for preventive healthcare solutions, particularly vaccination. Pet owners are becoming more proactive in safeguarding animal health, which is accelerating vaccine adoption. Increased attention toward diseases that can be transmitted between animals and humans is further reinforcing the importance of immunization programs. In addition, the expanding availability of pet healthcare services and insurance coverage is improving access to veterinary care. These factors are collectively encouraging higher spending on companion animal health and boosting vaccine uptake. As preventive care becomes a priority, the market is evolving with a strong focus on long-term disease protection, making vaccination an essential component of modern pet care practices.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.5 Billion |

| Forecast Value | $3.1 Billion |

| CAGR | 7.6% |

Cat vaccines represent a specialized category within veterinary medicine aimed at protecting companion animals from a range of infectious conditions. These vaccines are developed to strengthen immunity and reduce the risk of disease transmission, supporting overall animal health and well-being.

The modified and attenuated live vaccines segment held a 50.5% share in 2025. This segment is gaining traction due to its strong effectiveness, ability to generate a robust immune response, and cost efficiency. These vaccines are widely preferred because they provide durable protection and faster immune activation, making them suitable for environments where rapid disease control is essential. Their ability to deliver long-lasting immunity continues to support widespread adoption.

The feline respiratory diseases segment generated USD 500.4 million in 2025, leading the market due to the high occurrence and transmissibility of such conditions. These diseases significantly impact feline health and often lead to severe complications, increasing the need for preventive measures. The strong emphasis on early protection and disease management is driving demand within this segment, reinforcing its leading position in the overall market.

North America Cat Vaccines Market accounted for 45.2% share in 2025 and is expected to grow at a CAGR of 7.3% over the forecast period. The region's leadership is supported by high pet ownership rates, strong awareness of preventive healthcare, and well-established veterinary infrastructure. Increased spending on pet care and the availability of advanced healthcare services are contributing to sustained market growth. The presence of key industry participants and continued adoption of vaccination programs further strengthen the region's market position.

Key companies operating in the Global Cat Vaccines Market include Zoetis, Merck, Elanco Animal Health, Boehringer Ingelheim, Virbac, Ceva Sante Animale, HIPRA, Bioveta, and Indian Immunologicals. Companies in the Cat Vaccines Market are focusing on innovation and product development to enhance efficacy and safety profiles. Investment in research and development is enabling the introduction of advanced vaccine formulations with improved immune response and longer protection duration. Strategic collaborations and partnerships help expand geographic reach and strengthen distribution networks. Firms are also emphasizing awareness campaigns and veterinary engagement to increase vaccine adoption. Additionally, expanding product portfolios and improving accessibility through veterinary clinics and digital platforms are supporting market penetration, while ongoing advancements in biotechnology continue to shape competitive positioning.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Vaccine type trends

- 2.2.3 Disease type trends

- 2.2.4 Route of administration trends

- 2.2.5 Component trends

- 2.2.6 Duration of immunity trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing pet ownership and spending on pet health

- 3.2.1.2 Growing awareness of preventive pet healthcare

- 3.2.1.3 Advancements in vaccine technology

- 3.2.1.4 Rising awareness of zoonotic diseases

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High development cost of vaccines

- 3.2.2.2 Stringent regulatory requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of veterinary healthcare infrastructure and expansion of clinics

- 3.2.3.2 Increasing veterinary public health initiatives and programs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology and innovation landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Product pipeline analysis (Driven by Primary Research)

- 3.7 Patent analysis (Driven by Primary Research)

- 3.8 Future market trends

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Vaccine Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Modified/attenuated live

- 5.3 Inactivated

- 5.4 Other vaccine types

Chapter 6 Market Estimates and Forecast, By Disease Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Feline respiratory diseases

- 6.3 Feline leukemia

- 6.4 Feline panleukopenia (feline distemper)

- 6.5 Feline rabies

- 6.6 Other disease types

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Injectables

- 7.3 Intranasal

Chapter 8 Market Estimates and Forecast, By Component, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Combined vaccine

- 8.3 Mono vaccine

Chapter 9 Market Estimates and Forecast, By Duration of Immunity, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 1-year

- 9.3 3-years

- 9.4 Other durations of immunity

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Bioveta

- 11.2 Boehringer Ingelheim

- 11.3 Ceva Sante Animale

- 11.4 Elanco Animal Health

- 11.5 HIPRA

- 11.6 Indian Immunologicals

- 11.7 Merck

- 11.8 Virbac

- 11.9 Zoetis