|

市場調查報告書

商品編碼

2027534

細胞培養基市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Cell Culture Media Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

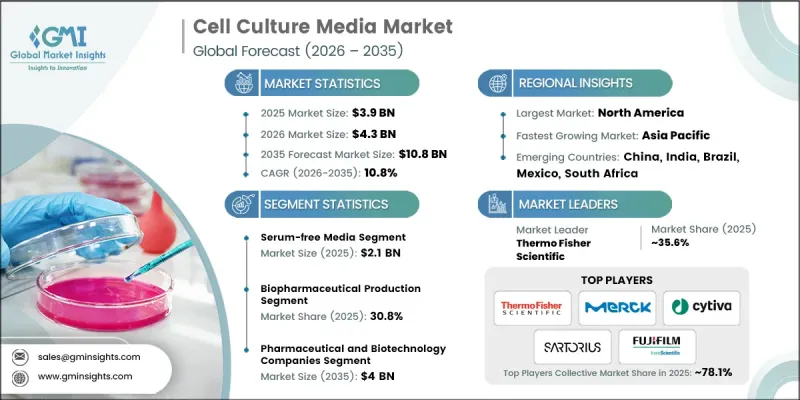

全球細胞培養基市場預計到 2025 年價值 39 億美元,預計到 2035 年將達到 108 億美元,年複合成長率為 10.8%。

市場擴張的驅動力在於癌症、糖尿病和自體免疫疾病等慢性病盛行率的上升,這導致對基於細胞的研究、開發和治療應用的需求不斷成長。細胞培養技術的進步,例如無血清和化學成分明確的培養基的開發,提高了實驗室的規模化生產能力、可重複性和效率。由於監管合規要求和降低污染風險,旨在提供細胞增殖、維持和分化所需營養的細胞培養基正在取代基於血清的配方。生物製藥生產商正在採用成分明確的培養基來確保批次品質的一致性,尤其是在生技藥品和疫苗的生產中。此外,向基於細胞的治療方法和單株抗體的轉變也進一步推動了市場需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 39億美元 |

| 預測金額 | 108億美元 |

| 複合年成長率 | 10.8% |

預計到2025年,無血清培養基市場規模將達21億美元。市場涵蓋CHO細胞培養基、HEK 293細胞培養基、BHK細胞培養基、VERO細胞培養基、昆蟲細胞培養基、免疫治療細胞培養基等無血清配方。與傳統的含血清培養基相比,無血清培養基具有更高的安全性、更好的法規遵循和更佳的重複性。無血清培養基消除了動物性成分帶來的變異性,確保細胞生長穩定,並提升產品品質。這對於生物製藥、疫苗和先進治療方法至關重要。細胞療法和單株抗體的日益普及也推動了無血清配方的廣泛應用。

預計到2025年,生物製藥製造領域將佔據30.8%的市場。該領域的成長主要得益於生物製藥行業的擴張以及包括疫苗、重組蛋白、基因療法和細胞療法在內的生物製藥產品的日益普及。慢性病發病率的上升以及對標靶治療需求的成長,正在推動這些治療方法的研發和商業化,從而支撐全球細胞培養基市場的發展。

到2025年,北美細胞培養基市佔率將達到39%。該地區的生物技術和製藥行業受益於先進的研究基礎設施、對生命科學的大量投資以及政府的大力支持。來自美國國立衛生研究院(NIH)等機構的資助以及對個人化醫療日益成長的需求,進一步加速了專用細胞培養基的普及應用。美國持續投資於創新生物製藥研發,從而推動區域成長,並滿足了對高品質、可重複細胞培養解決方案日益成長的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 影響產業的因素

- 成長促進因素

- 慢性病發生率增加

- 細胞培養和培養基技術的進步

- 對不含血清和動物性成分的培養基的需求日益成長。

- 對再生醫學的需求日益成長

- 產業潛在風險與挑戰

- 細胞生物學產品成本高昂

- 嚴峻的監理挑戰

- 市場機遇

- 對先進醫療產品(ATMP)的需求不斷成長

- 增加契約製造和CDMO夥伴關係

- 客製化培養基配方方面的技術進步

- 成長促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 北美洲

- 技術與創新趨勢(基於初步調查)

- 目前技術

- 新興技術

- 2025年細胞培養基生產分析

- 生產能力

- 設備運轉率

- 最終/實際產量

- 生產趨勢

- 2025年價格分析(基於初步調查)

- 專利趨勢(基於初步調查)

- 差距分析

- 未來市場趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 波特五力分析

- PESTEL 分析

- 細胞培養基產業鏈分析

- 上游工程分析

- 原物料採購

- 配方開發

- 生產製造和品管

- 供應鍊和物流

- 下游段

- 最終用戶

- 目的

- 分銷管道

- 上游工程分析

- 供應鏈分析

- 主要公司客戶概況分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 無血清培養基

- CHO培養基

- HEK 293 中等大小

- BHK 中等

- VERO細胞培養基

- 昆蟲細胞培養基

- 免疫細胞培養基

- 其他無血清培養基

- 特殊培養基

- 化學成分明確的培養基

- 幹細胞培養基

- 其他產品類型

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 生物製藥生產

- 單株抗體

- 疫苗生產

- 其他生物製藥生產

- 診斷

- 藥物篩檢和開發

- 組織工程與再生醫學

- 研究目的

- 其他用途

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 製藥和生物技術公司

- 醫院/診斷檢查室

- 研究機構和學術機構

- 其他最終用戶

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- ACROBiosystems

- Biowest

- Cellplus Bio

- Corning

- Cytiva

- Elabscience

- Eminence Scientific

- FUJIFILM Irvine Scientific

- JSBio

- Lonza

- Shanghai Mediumbank Biotechnology

- Merck

- Miltenyi Biotec

- OPM Biosciences

- ProBio

- PromoCell

- Quacell Biotechnology

- Sartorius

- Shanghai BioEngine

- Shanghai Basal Media

- Sino Biological

- Suzhou Womei

- Thermo Fisher Scientific

The Global Cell Culture Media Market was valued at USD 3.9 billion in 2025 and is estimated to grow at a CAGR of 10.8% to reach USD 10.8 billion by 2035.

Market expansion is driven by the rising prevalence of chronic diseases, including cancer, diabetes, and autoimmune disorders, which increase the demand for cell-based research and therapeutic applications. Technological advancements in cell culture, such as the development of serum-free and chemically defined media, have enhanced scalability, reproducibility, and efficiency in laboratories. Cell culture media, designed to provide essential nutrients for cellular growth, maintenance, and differentiation, are increasingly replacing serum-based formulations due to regulatory compliance requirements and reduced contamination risks. Biopharmaceutical manufacturers are adopting defined media to ensure consistent batch quality, particularly in biologics and vaccine production, while the shift toward cell-based therapies and monoclonal antibodies is further fueling demand.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.9 Billion |

| Forecast Value | $10.8 Billion |

| CAGR | 10.8% |

The serum-free media segment generated USD 2.1 billion in 2025. This segment includes CHO media, HEK 293 media, BHK media, VERO cell media, insect cell media, immune cell media, and other serum-free formulations. Its dominance is attributed to enhanced safety, regulatory compliance, and reproducibility compared to traditional serum-based media. Serum-free media eliminate variability from animal-derived components, ensuring consistent cell growth and improved product quality, which is crucial for biologics, vaccines, and advanced therapies. The increasing adoption of cell-based therapies and monoclonal antibodies has also contributed to the widespread use of serum-free formulations.

The biopharmaceutical production segment accounted for a 30.8% share in 2025. Growth in this segment is fueled by the expansion of the biopharmaceutical industry and the increasing adoption of biologics, including vaccines, recombinant proteins, gene therapies, and cell therapies. Rising chronic disease incidence and demand for targeted treatments have driven the development and commercialization of these therapies, supporting the global cell culture media market.

North America Cell Culture Media Market held a 39% share in 2025. The region's biotechnology and pharmaceutical sectors benefit from advanced research infrastructure, substantial life sciences investments, and strong government support. Funding from institutions such as the National Institutes of Health (NIH) and growing demand for personalized therapies have further accelerated the adoption of specialized cell culture media. The U.S. continues to drive regional growth through investments in innovative biopharmaceutical research and development, which underpins the rising need for high-quality, reproducible cell culture solutions.

Key players operating in the Cell Culture Media Market include Merck, FUJIFILM Irvine Scientific, Thermo Fisher Scientific, Lonza, Sartorius, Cytiva, ACROBiosystems, Miltenyi Biotec, PromoCell, Biowest, JSBio, Shanghai Mediumbank Biotechnology, ProBio, Quacell Biotechnology, Elabscience, Cellplus Bio, Shanghai BioEngine, Eminence Scientific, Corning, Shanghai Basal Media, Sino Biological, and OPM Biosciences. Key strategies employed by companies in the Cell Culture Media Market include expanding their portfolio of serum-free and chemically defined media to meet regulatory standards and minimize contamination risks. Manufacturers are focusing on R&D to develop specialized media for biopharmaceutical and cell therapy applications. Strategic partnerships with research institutions and biopharmaceutical companies enhance distribution channels and market reach. Companies are investing in scalable production facilities to meet growing global demand, while also leveraging technology to improve product quality and consistency. Targeted marketing campaigns, regulatory compliance certifications, and collaborations with healthcare and life sciences organizations further strengthen market presence and reinforce brand credibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of chronic diseases

- 3.2.1.2 Advancements in cell culture and media technology

- 3.2.1.3 Increasing demand for serum and animal component-free media

- 3.2.1.4 Growing demand for regenerative medicine

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of cell biology products

- 3.2.2.2 Stringent regulatory challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for advanced therapy medicinal products (ATMPs)

- 3.2.3.2 Rising contract manufacturing and CDMO partnerships

- 3.2.3.3 Technological advancements in custom media formulation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology and innovation landscape (Driven by Primary Research)

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Cell culture media production analysis, 2025

- 3.6.1 Production capacity

- 3.6.2 Capacity utilization rate

- 3.6.3 Final/actual manufactured volume

- 3.6.4 Production trends

- 3.7 Pricing analysis, 2025 (Driven by Primary Research)

- 3.8 Patent landscape (Driven by Primary Research)

- 3.9 Gap analysis

- 3.10 Future market trends

- 3.11 Impact of AI and Gen AI on the market

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Cell culture media industry chain analysis

- 3.14.1 Upstream process analysis

- 3.14.1.1 Raw material sourcing

- 3.14.1.2 Formulation development

- 3.14.1.3 Manufacturing and quality control

- 3.14.1.4 Supply chain and logistics

- 3.14.2 Downstream segments

- 3.14.2.1 End user

- 3.14.2.2 Application

- 3.14.2.3 Distribution channels

- 3.14.1 Upstream process analysis

- 3.15 Supply chain analysis

- 3.16 Customer profile analysis for major companies

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Serum-free media

- 5.2.1 CHO media

- 5.2.2 HEK 293 media

- 5.2.3 BHK media

- 5.2.4 VERO cell media

- 5.2.5 Insect cell media

- 5.2.6 Immune cell media

- 5.2.7 Other serum-free media

- 5.3 Specialty media

- 5.4 Chemically defined media

- 5.5 Stem cell culture media

- 5.6 Other product types

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Biopharmaceutical production

- 6.2.1 Monoclonal antibodies

- 6.2.2 Vaccine production

- 6.2.3 Other biopharmaceutical productions

- 6.3 Diagnostics

- 6.4 Drug screening and development

- 6.5 Tissue engineering and regenerative medicine

- 6.6 Research purpose

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Pharmaceutical and biotechnology companies

- 7.3 Hospital and diagnostic laboratories

- 7.4 Research and academic institutes

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ACROBiosystems

- 9.2 Biowest

- 9.3 Cellplus Bio

- 9.4 Corning

- 9.5 Cytiva

- 9.6 Elabscience

- 9.7 Eminence Scientific

- 9.8 FUJIFILM Irvine Scientific

- 9.9 JSBio

- 9.10 Lonza

- 9.11 Shanghai Mediumbank Biotechnology

- 9.12 Merck

- 9.13 Miltenyi Biotec

- 9.14 OPM Biosciences

- 9.15 ProBio

- 9.16 PromoCell

- 9.17 Quacell Biotechnology

- 9.18 Sartorius

- 9.19 Shanghai BioEngine

- 9.20 Shanghai Basal Media

- 9.21 Sino Biological

- 9.22 Suzhou Womei

- 9.23 Thermo Fisher Scientific

培養基市場規模、佔有率和成長分析:按產品類型、培養基類型、應用、最終用戶和地區分類-2026-2033年產業預測

培養基市場規模、佔有率和成長分析:按產品類型、培養基類型、應用、最終用戶和地區分類-2026-2033年產業預測 全球細胞培養基市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球細胞培養基市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 胚胎培養基市場:按產品類型、胚胎發育階段、產品形狀、最終用戶和應用分類-全球市場預測(2026-2032 年)細胞培養基市場:依產品類型、細胞類型、形態、應用和最終用戶分類-2026-2032年全球市場預測

胚胎培養基市場:按產品類型、胚胎發育階段、產品形狀、最終用戶和應用分類-全球市場預測(2026-2032 年)細胞培養基市場:依產品類型、細胞類型、形態、應用和最終用戶分類-2026-2032年全球市場預測 倉鼠卵巢來源單株抗體市場規模、佔有率和成長分析:按產品類型、應用、最終用戶和地區分類-2026-2033年產業預測

倉鼠卵巢來源單株抗體市場規模、佔有率和成長分析:按產品類型、應用、最終用戶和地區分類-2026-2033年產業預測 倉鼠卵巢FC融合蛋白市場規模、佔有率和成長分析:按治療適應症、融合伴侶類型、生產策略、分子結構和地區分類-產業預測,2026-2033年

倉鼠卵巢FC融合蛋白市場規模、佔有率和成長分析:按治療適應症、融合伴侶類型、生產策略、分子結構和地區分類-產業預測,2026-2033年 體外診斷試劑和細胞培養基市場規模、佔有率和成長分析:按產品類型、應用和地區分類-2026-2033年產業預測

體外診斷試劑和細胞培養基市場規模、佔有率和成長分析:按產品類型、應用和地區分類-2026-2033年產業預測 2026年全球再生醫學細胞培養基市場報告2026年全球細胞培養基市場報告Dulbecco改良Eagle培養基(DMEM)設備全球市場報告(2026年)

2026年全球再生醫學細胞培養基市場報告2026年全球細胞培養基市場報告Dulbecco改良Eagle培養基(DMEM)設備全球市場報告(2026年)